Backtest trading strategies in Python

Project description

Backtesting.py

Backtest trading strategies with Python.

Project website + Documentation | YouTube

Installation

$ pip install backtesting

Usage

from backtesting import Backtest, Strategy

from backtesting.lib import crossover

from backtesting.test import SMA, GOOG

class SmaCross(Strategy):

def init(self):

price = self.data.Close

self.ma1 = self.I(SMA, price, 10)

self.ma2 = self.I(SMA, price, 20)

def next(self):

if crossover(self.ma1, self.ma2):

self.buy()

elif crossover(self.ma2, self.ma1):

self.sell()

bt = Backtest(GOOG, SmaCross, commission=.002,

exclusive_orders=True)

stats = bt.run()

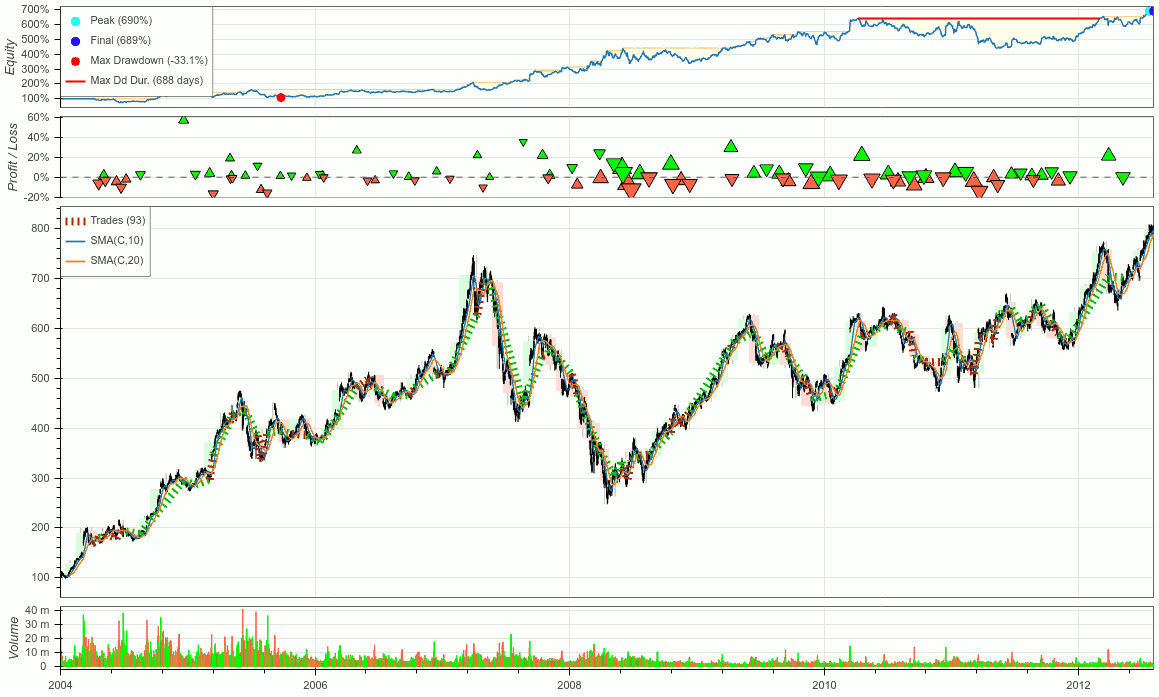

bt.plot()

Results in:

Start 2004-08-19 00:00:00

End 2013-03-01 00:00:00

Duration 3116 days 00:00:00

Exposure Time [%] 94.27

Equity Final [$] 68935.12

Equity Peak [$] 68991.22

Return [%] 589.35

Buy & Hold Return [%] 703.46

Return (Ann.) [%] 25.42

Volatility (Ann.) [%] 38.43

CAGR [%] 16.80

Sharpe Ratio 0.66

Sortino Ratio 1.30

Calmar Ratio 0.77

Alpha [%] 450.62

Beta 0.02

Max. Drawdown [%] -33.08

Avg. Drawdown [%] -5.58

Max. Drawdown Duration 688 days 00:00:00

Avg. Drawdown Duration 41 days 00:00:00

# Trades 93

Win Rate [%] 53.76

Best Trade [%] 57.12

Worst Trade [%] -16.63

Avg. Trade [%] 1.96

Max. Trade Duration 121 days 00:00:00

Avg. Trade Duration 32 days 00:00:00

Profit Factor 2.13

Expectancy [%] 6.91

SQN 1.78

Kelly Criterion 0.6134

_strategy SmaCross(n1=10, n2=20)

_equity_curve Equ...

_trades Size EntryB...

dtype: object

Find more usage examples in the documentation.

Features

- Simple, well-documented API

- Blazing fast execution

- Built-in optimizer

- Library of composable base strategies and utilities

- Indicator-library-agnostic

- Supports any financial instrument with candlestick data

- Detailed results

- Interactive visualizations

Bugs

Before reporting bugs or posting to the

discussion board,

please read contributing guidelines, particularly the section

about crafting useful bug reports and ```-fencing your code. We thank you!

Alternatives

See alternatives.md for a list of alternative Python backtesting frameworks and related packages.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file backtesting-0.6.5.tar.gz.

File metadata

- Download URL: backtesting-0.6.5.tar.gz

- Upload date:

- Size: 194.0 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.0.1 CPython/3.11.2

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

738a1dee28fc53df2eda35ea2f2d1a1c37ddba01df14223fc9e87d80a1efbc2e

|

|

| MD5 |

d4a48b6cd5962b4eae8404906e2772ff

|

|

| BLAKE2b-256 |

dbcca3bf58f45e1a58c28681fe1f173cdf748bd91e7cde60e3dcc29c8e9aa194

|

File details

Details for the file backtesting-0.6.5-py3-none-any.whl.

File metadata

- Download URL: backtesting-0.6.5-py3-none-any.whl

- Upload date:

- Size: 192.1 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.0.1 CPython/3.11.2

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

8ac2fa500c8fd83dc783b72957b600653a72687986fe3ca86d6ef6c8b8d74363

|

|

| MD5 |

d18e5a413c5e0bd965052109924b2ea4

|

|

| BLAKE2b-256 |

b3b6cf57538b968c5caa60ee626ec8be1c31e420067d2a4cf710d81605356f8c

|