Log Periodic Power Law Singularity (LPPLS) Model

lppls is a Python module for fitting the LPPLS model to data.

Overview

The LPPLS model provides a flexible framework to detect bubbles and predict regime changes of a financial asset. A bubble is defined as a faster-than-exponential increase in asset price, that reflects positive feedback loop of higher return anticipations competing with negative feedback spirals of crash expectations. It models a bubble price as a power law with a finite-time singularity decorated by oscillations with a frequency increasing with time.

Try the demo:

Here is the model:

E[ln\ p(t)] = A + B(t_c-t)^{m}+C(t_c-t)^{m}\cos(\omega\ ln(t_c-t) - \phi)

where:

- $E[ln\ p(t)]$: expected log price at the date of the termination of the bubble

- $t_c$: critical time (date of termination of the bubble and transition in a new regime)

- $A$: expected log price at the peak when the end of the bubble is reached at $t_c$

- $B$: amplitude of the power law acceleration

- $C$: amplitude of the log-periodic oscillations

- $m$: degree of the super exponential growth

- $\omega$: scaling ratio of the temporal hierarchy of oscillations

- $\phi$: time scale of the oscillations

The model has three components representing a bubble. The first, $A+B(t_c-t)^{m}$, handles the hyperbolic power law. For $m$ < 1 when the price growth becomes unsustainable, and at $t_c$ the growth rate becomes infinite. The second term, $C(t_c-t)^{m}$, controls the amplitude of the oscillations. It drops to zero at the critical time $t_c$. The third term, $\cos(\omega\ ln(t_c-t) - \phi)$, models the frequency of the oscillations. They become infinite at $t_c$.

Important links

- Official source code repo: https://github.com/Boulder-Investment-Technologies/lppls

- Download releases: https://pypi.org/project/lppls/

- Issue tracker: https://github.com/Boulder-Investment-Technologies/lppls/issues

Installation

Dependencies

lppls requires:

- Python (>= 3.10)

- CMA-ES (>= 3.3.0)

- Matplotlib (>= 3.5.0)

- Numba (>= 0.56.0)

- NumPy (>= 1.23.0)

- Pandas (>= 1.5.0)

- SciPy (>= 1.9.0)

- Scikit-learn (>= 1.2.0)

- tqdm (>= 4.64.0)

- Xarray (>= 2024.1.0)

User installation

pip install -U lppls

Example Use

from lppls import lppls, data_loader

import numpy as np

import pandas as pd

from datetime import datetime as dt

%matplotlib inline

# read example dataset into df

data = data_loader.nasdaq_dotcom()

# convert time to ordinal

time = [pd.Timestamp.toordinal(dt.strptime(t1, '%Y-%m-%d')) for t1 in data['Date']]

# create list of observation data

price = np.log(data['Adj Close'].values)

# create observations array (expected format for LPPLS observations)

observations = np.array([time, price])

# set the max number for searches to perform before giving-up

# the literature suggests 25

MAX_SEARCHES = 25

# instantiate a new LPPLS model with the Nasdaq Dot-com bubble dataset

lppls_model = lppls.LPPLS(observations=observations)

# fit the model to the data and get back the params

tc, m, w, a, b, c, c1, c2, O, D = lppls_model.fit(MAX_SEARCHES)

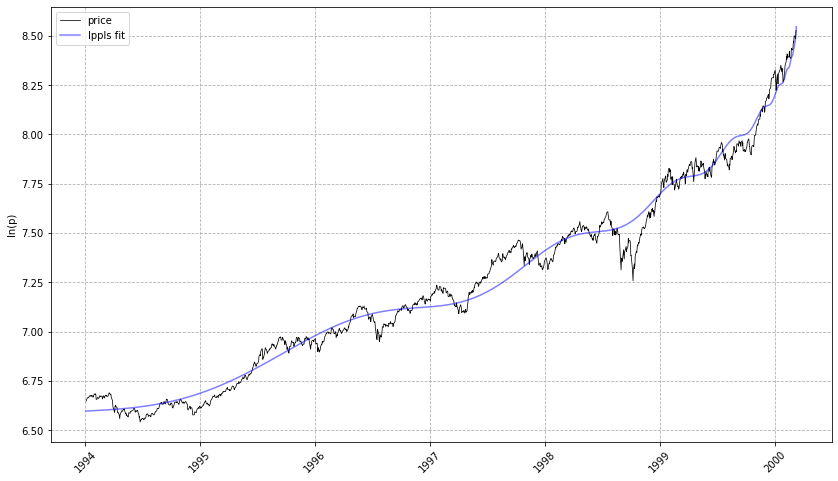

# visualize the fit

lppls_model.plot_fit()

# should give a plot like the following...

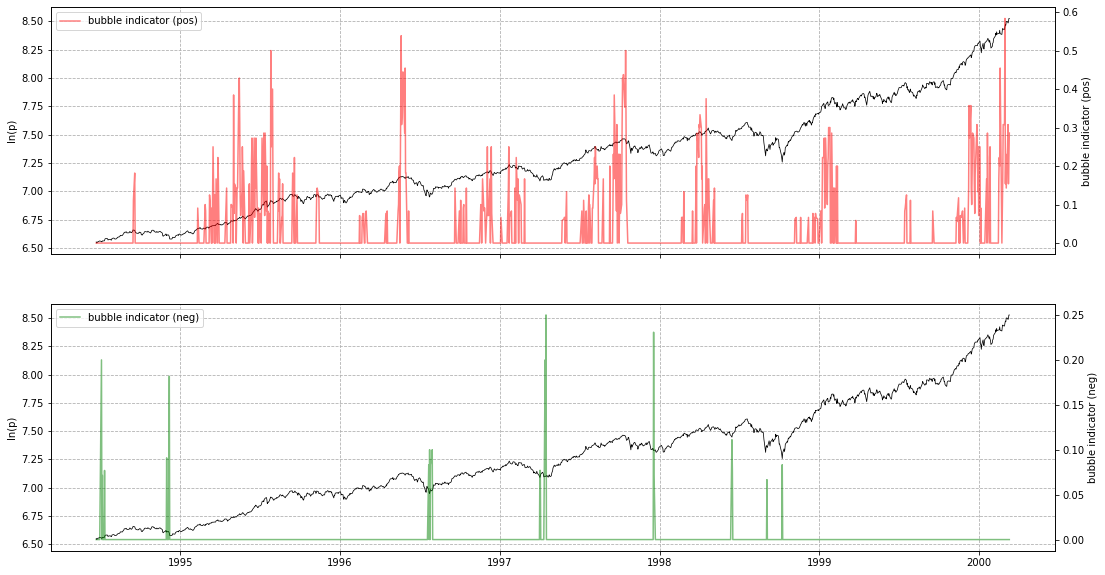

# compute the confidence indicator

res = lppls_model.mp_compute_nested_fits(

workers=8,

window_size=120,

smallest_window_size=30,

outer_increment=1,

inner_increment=5,

max_searches=25,

filter_conditions_config={

"m_min": 0.0,

"m_max": 1.0,

"w_min": 2.0,

"w_max": 15.0,

"O_min": 2.5,

"D_min": 0.5,

},

)

lppls_model.plot_confidence_indicators(res)

# should give a plot like the following...

If you wish to store res as a pd.DataFrame, use compute_indicators.

Example

res_df = lppls_model.compute_indicators(res)

res_df

# gives the following...

Quantile Regression

Based on the work in Zhang, Zhang & Sornette 2016, quantile regression for LPPLS uses the L1 norm (sum of absolute differences) instead of the L2 norm and applies the q-dependent loss function during calibration. Please refer to the example usage here.

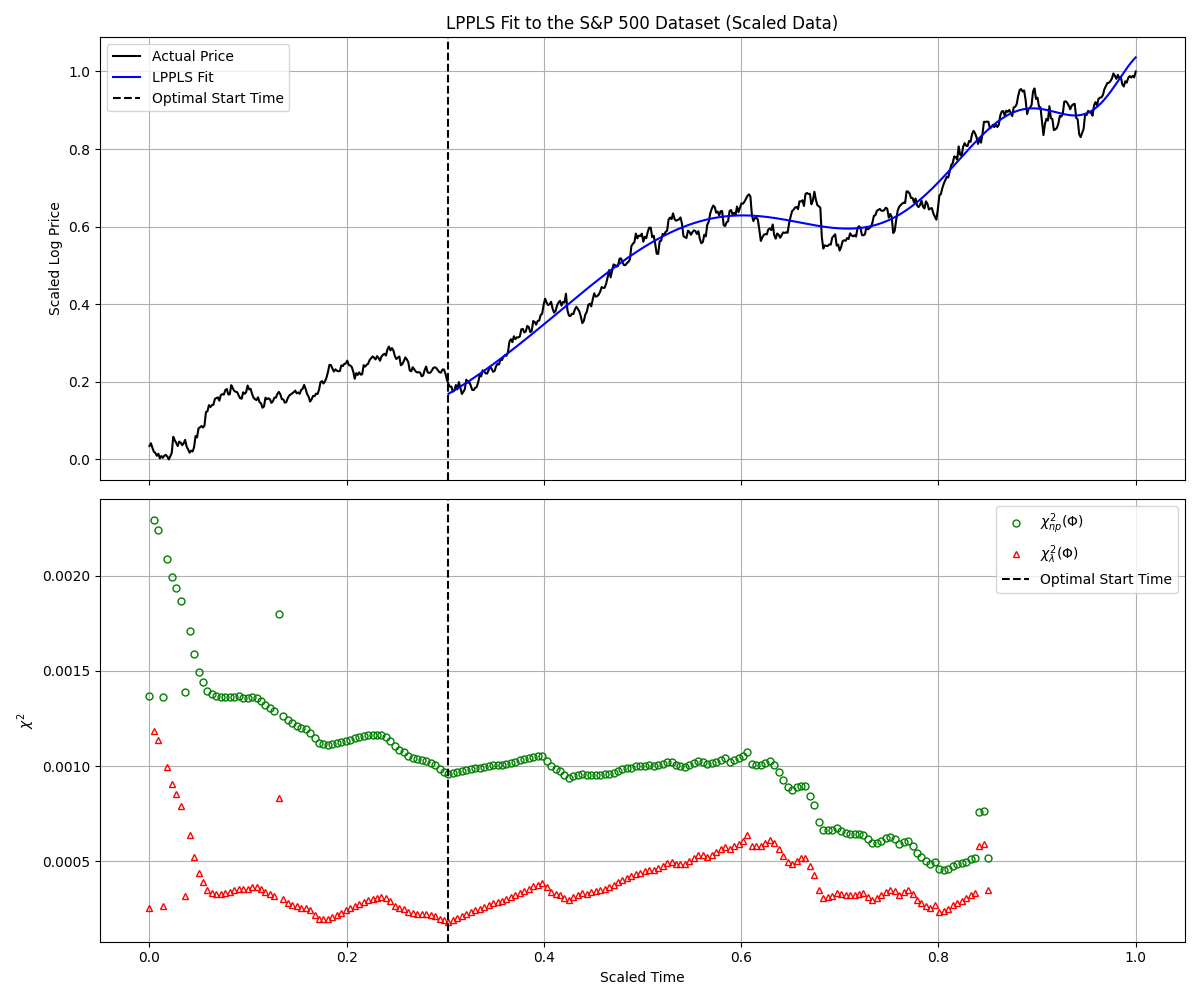

Lagrange Regularization for Bubble Start Time Detection

The lppls library includes a method for determining the start time of a financial bubble using Lagrange regularization. This technique, inspired by the work of Demos & Sornette (2017), addresses the challenge of model overfitting when the bubble's inception is unknown.

By introducing a regularization term to the normalized sum of squared residuals, the method objectively identifies the optimal fitting window size. This allows for a more robust and data-driven estimation of the bubble's start time without requiring exogenous information, which is a significant improvement over previous approaches.

This functionality is available through the detect_bubble_start_time_via_lagrange method. For detailed usage, please refer to the tutorial here.

Other Search Algorithms

Shu and Zhu (2019) proposed CMA-ES for identifying the best estimation of the three non-linear parameters ($t_c$, $m$, $\omega$).

The CMA-ES rates among the most successful evolutionary algorithms for real-valued single-objective optimization and is typically applied to difficult nonlinear non-convex black-box optimization problems in continuous domain and search space dimensions between three and a hundred. Parallel computing is adopted to expedite the fitting process drastically.

This approach has been implemented in a subclass and can be used as follows... Thanks to @paulogonc for the code.

from lppls import lppls_cmaes

lppls_model = lppls_cmaes.LPPLSCMAES(observations=observations)

tc, m, w, a, b, c, c1, c2, O, D = lppls_model.fit(max_iteration=2500, pop_size=4)

Performance Note: this works well for single fits but can take a long time for computing the confidence indicators. More work needs to be done to speed it up.

References

- Filimonov, V. and Sornette, D. A Stable and Robust Calibration Scheme of the Log-Periodic Power Law Model. Physica A: Statistical Mechanics and its Applications. 2013

- Shu, M. and Zhu, W. Real-time Prediction of Bitcoin Bubble Crashes. 2019.

- Sornette, D. Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press. 2002.

- Sornette, D. and Demos, G. and Zhang, Q. and Cauwels, P. and Filimonov, V. and Zhang, Q., Real-Time Prediction and Post-Mortem Analysis of the Shanghai 2015 Stock Market Bubble and Crash (August 6, 2015). Swiss Finance Institute Research Paper No. 15-31.

- Demos, G. and Sornette, D. Lagrange regularisation approach to compare nested data sets and determine objectively financial bubbles' inceptions. 2017. arXiv:1707.07162

- Zhang, Q., Zhang, Q., and Sornette, D. Early Warning Signals of Financial Crises with Multi-Scale Quantile Regressions of Log-Periodic Power Law Singularities. PLOS ONE. 2016. DOI:10.1371/journal.pone.0165819

1 maintainer

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file lppls-0.6.24.tar.gz.

File metadata

- Download URL: lppls-0.6.24.tar.gz

- Upload date:

- Size: 61.3 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.14.5

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

7fdf19011309067c95222e90627e9c09ac1d3841777b9b4555b5761128f3065f

|

|

| MD5 |

225e113e96384f93ac932133cc5b38ce

|

|

| BLAKE2b-256 |

3cf172d14ee7b4a14eff3e88be78987a701dfc5d53194ac69cdc3485ad5560bd

|

File details

Details for the file lppls-0.6.24-py3-none-any.whl.

File metadata

- Download URL: lppls-0.6.24-py3-none-any.whl

- Upload date:

- Size: 52.6 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.14.5

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

6c414b29c6e07ba5b79cbe9c6ea60b6f0e3a15e30371ddfa0ae73ace61564636

|

|

| MD5 |

927d4ad149caaebb10e8404fccc99bae

|

|

| BLAKE2b-256 |

ade734b14c7c936919961a5008cae4d6898f009a365d7d8d3568daa7f97de13d

|