SodesPy (Stochastic Ordinary Differential Equations Suite in Python) is a high-performance library for numerically solving stochastic differential equations (SDEs).

Project description

SodesPy

SodesPy (Stochastic Ordinary Differential Equations Suite in Python) is a high-performance library for numerically solving stochastic differential equations (SDEs).

SodesPy provides many Ito and Stratonovich discretization schemes, an intuitive interface to define SDE systems and the option to solve them using CPU, GPUs or even TPUs.

With SodesPy you can solve, for example, the following (and many more) well known SDEs:

- Heston Model. A model for determining the evolution of the volatility of an underlying asset.

- Geometric Brownian Motion. The basic model for stock prices under Black–Scholes framework.

- Ornstein Uhlenbeck Process. A model with applications in mathematical finance and physics.

- Affine short rate. A general class for short rate models.

- Stochastic SIR Epidemic Model. A compartmental epidemiologic model.

- Stochastic Lorenz Attractor. A stochastic form of the classic Lorenz Attractor system.

Furthermore, SodesPy offers the following discretization schemes:

-

Classic:

- Euler. Classical scheme with 0.5 strong convergence and general noise.

-

Stochastic Runge Kutta (SRK):

Examples

If you want to define an Euler process you need to define the drift and diffusion functions, the discretization step and the initial condition. Taking this into account, an Euler process input file looks like:

from sodespy import *

scheme = "Euler"

noise_type = "Diagonal"

x0 = [.1, .1]

dt = 1 / 252

paths = 1000

tspan = (0.0, 1.0)

μs = [0.05, 0.044]

σs = [0.05, 0.044]

mu = [lambda x, t: μs[i] * x[i] for i in range(2)]

sigma = [lambda x, t: σs[i] * x[i] for i in range(2)]

sdes = SDESystem(mu, sigma, noise_type, scheme, x0, tspan, dt, paths)

sdes.simulate()

Another nice example that shows the flexibility of SodesPy is the Lorenz attractor, which can be written as:

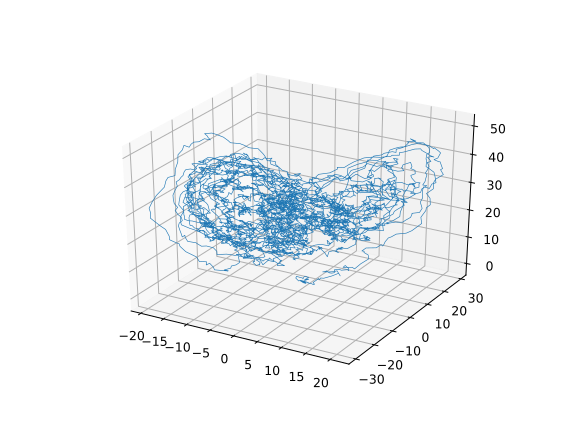

from sodespy import *

scheme = "Euler"

noise_type = "Diagonal"

paths = 1

tspan = (0.0, 20.0)

dt = 1 / 252

x0 = [1.0, 0.0, 0.0]

α = 10.0

β = 28.0

γ = 8 / 3

mu = [lambda x, t: α * (x[1] - x[0]),

lambda x, t: x[0] * (β - x[2]) - x[1],

lambda x, t: x[0] * x[1] - γ * x[2]]

sigma = [lambda x, t: 10.0,

lambda x, t: 10.0,

lambda x, t: 10.0]

sdes = SDESystem(mu, sigma, noise_type, scheme, x0, tspan, dt, paths)

sdes.simulate()

plt.plot(sdes.solution)

plt.show()

This will plot the beautiful Lorenz attractor:

Installation

SodesPy can be installed via pip install sodespy

Author

SodesPy is authored by mpkuperman

License

SodesPy is distributed under the GPL-3.0 License.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file sodespy-0.0.1.tar.gz.

File metadata

- Download URL: sodespy-0.0.1.tar.gz

- Upload date:

- Size: 20.6 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/3.4.2 importlib_metadata/4.8.1 pkginfo/1.7.1 requests/2.22.0 requests-toolbelt/0.9.1 tqdm/4.61.1 CPython/3.8.10

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

8cee1c60dc29ce2f41fafdd53b0b677d43af948e114047067a9e2b0df42f01c4

|

|

| MD5 |

e2bb39861ed07a3b9665d9109ad1121e

|

|

| BLAKE2b-256 |

5eee9b6d24a3604e57a32d6b86e3871e6492f41e880f3d8f458e2e38d3a60e23

|

File details

Details for the file sodespy-0.0.1-py3-none-any.whl.

File metadata

- Download URL: sodespy-0.0.1-py3-none-any.whl

- Upload date:

- Size: 20.2 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/3.4.2 importlib_metadata/4.8.1 pkginfo/1.7.1 requests/2.22.0 requests-toolbelt/0.9.1 tqdm/4.61.1 CPython/3.8.10

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

0a14fd373da31cf86065f4fb641cfc902c7a0c87cb24a2e356dcf4b240b5d793

|

|

| MD5 |

68f5d053f6b0efac632985b2b46f491b

|

|

| BLAKE2b-256 |

bd3857ffaa12d71094fa0fdc44ce7ba09408ce4db53537d9bbc65137cd4c320a

|