Tools for analyzing financial timeseries.

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Project description

openseries

Tools for analyzing financial timeseries of a single asset or a group of assets. Designed for daily or less frequent data.

Documentation

Complete documentation is available at: https://captorab.github.io/openseries/

The documentation includes:

- Quick start guide

- API reference

- Tutorials and examples

- Installation instructions

Installation

pip install openseries

or:

conda install -c conda-forge openseries

Quick Start

from openseries import OpenTimeSeries

import yfinance as yf

move=yf.Ticker(ticker="^MOVE")

history=move.history(period="max")

series=OpenTimeSeries.from_df(dframe=history.loc[:, "Close"])

_=series.set_new_label(lvl_zero="ICE BofAML MOVE Index")

_,_=series.plot_series()

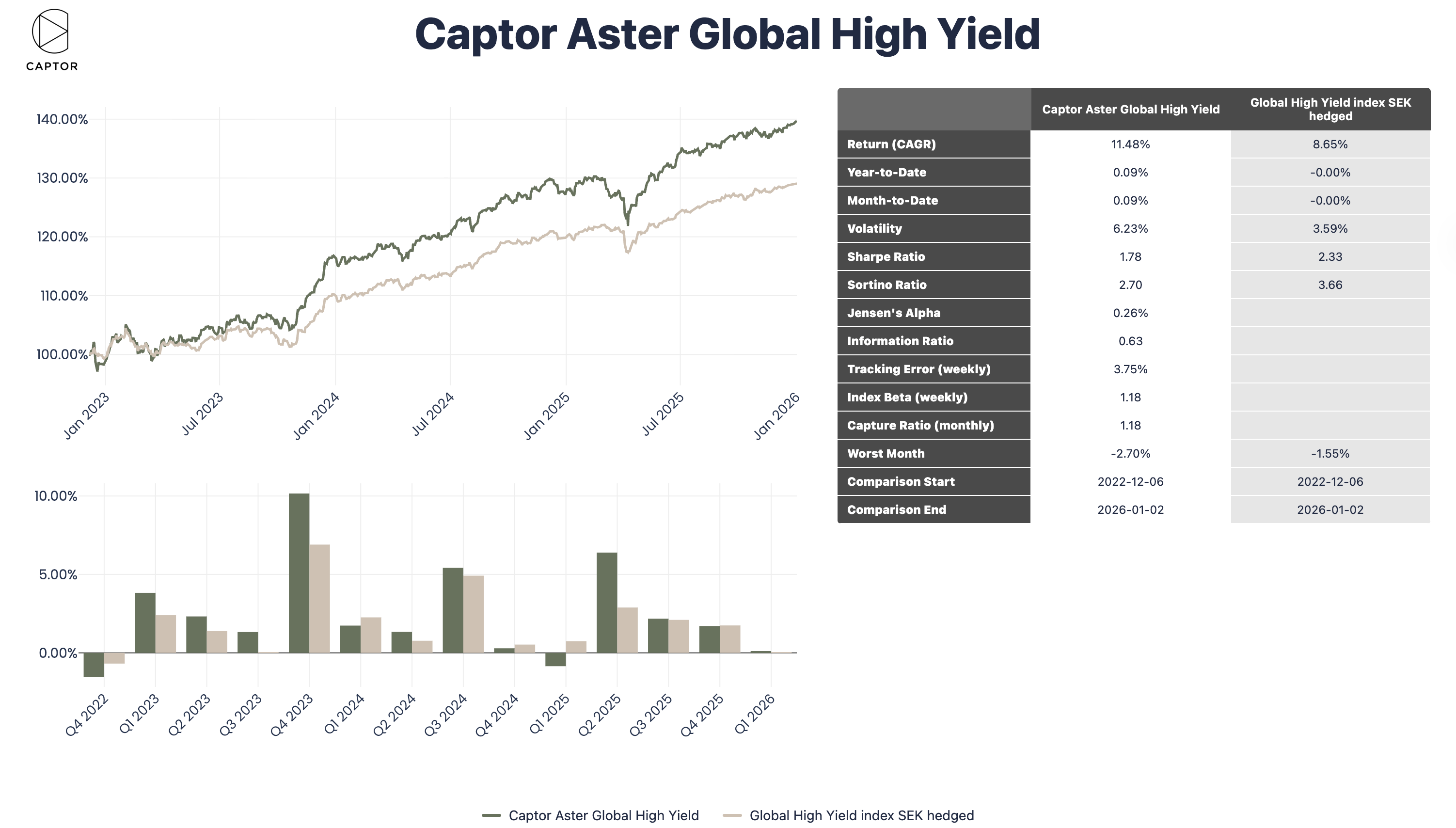

Sample output using the report_html() function

Project details

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file openseries-2.1.9.tar.gz.

File metadata

- Download URL: openseries-2.1.9.tar.gz

- Upload date:

- Size: 121.6 kB

- Tags: Source

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.13

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

e7433a5c36525d0deaad7fe99b4fb0b05eb72bd06c3ddb8fbd6e8dc840fd7e7e

|

|

| MD5 |

21c1a88dcb2135973b6771a6bb39e569

|

|

| BLAKE2b-256 |

10c30c1e3c8f668fa7ecf031a6d933fe2ebe2d090a691d798e172f562e82bd91

|

Provenance

The following attestation bundles were made for openseries-2.1.9.tar.gz:

Publisher:

deploy.yml on CaptorAB/openseries

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

openseries-2.1.9.tar.gz -

Subject digest:

e7433a5c36525d0deaad7fe99b4fb0b05eb72bd06c3ddb8fbd6e8dc840fd7e7e - Sigstore transparency entry: 1646836445

- Sigstore integration time:

-

Permalink:

CaptorAB/openseries@e3b2b4b6a403081ef4e0460d7f2a92e29b8a42ec -

Branch / Tag:

refs/heads/master - Owner: https://github.com/CaptorAB

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

deploy.yml@e3b2b4b6a403081ef4e0460d7f2a92e29b8a42ec -

Trigger Event:

workflow_dispatch

-

Statement type:

File details

Details for the file openseries-2.1.9-py3-none-any.whl.

File metadata

- Download URL: openseries-2.1.9-py3-none-any.whl

- Upload date:

- Size: 70.8 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.13

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

6039106ab3f5039b698adf0cd6b5db855720426d64a7525111995113cf0ececd

|

|

| MD5 |

1ae937e936514d380cc4e2e66308c99c

|

|

| BLAKE2b-256 |

cfbf66767a3b17630c3da48c0d5c5a98b6dff8ff4bc9cd3d953b538f053faf80

|

Provenance

The following attestation bundles were made for openseries-2.1.9-py3-none-any.whl:

Publisher:

deploy.yml on CaptorAB/openseries

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

openseries-2.1.9-py3-none-any.whl -

Subject digest:

6039106ab3f5039b698adf0cd6b5db855720426d64a7525111995113cf0ececd - Sigstore transparency entry: 1646836475

- Sigstore integration time:

-

Permalink:

CaptorAB/openseries@e3b2b4b6a403081ef4e0460d7f2a92e29b8a42ec -

Branch / Tag:

refs/heads/master - Owner: https://github.com/CaptorAB

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

deploy.yml@e3b2b4b6a403081ef4e0460d7f2a92e29b8a42ec -

Trigger Event:

workflow_dispatch

-

Statement type: