Time series-based machine learning framework for stock market forecasting

Project description

Overview

AuToMaR is a customizable time series-based machine learning framework for forecasting the stock market. Built in Python, it provides both a powerful web-based GUI and a command-line interface for financial data analysis and model training.

The framework supports sector-aware modeling: optionally extract data for all companies in a chosen economic sector, apply PCA dimensionality reduction to capture sector-wide patterns, and train models on this enriched feature space. This allows models to learn from industry-level dynamics and correlations, or work with individual stocks in isolation.

Key capabilities:

| Component | Description |

|---|---|

| Web Interface | Full-featured SvelteKit GUI with real-time job tracking and visualization |

| Data Pipeline | Yahoo Finance extraction with automated technical indicator generation |

| ML Models | GRU, Transformer, and Logistic Regression with Ray Tune hyperparameter optimization |

| Dimensionality Reduction | PCA transformation with feature name visualization |

| Validation | Growing windows cross-validation for robust time series evaluation |

| Forecasting | Multi-day ahead predictions using autoregressive feature synthesis |

| Visualization | Interactive Plotly charts with comprehensive statistical analysis |

Table of Contents

- Features

- Installation

- Quick Start

- How It Works

- Visual Tutorial

- Configuration

- Building Distribution Packages

- Requirements

- Developed With

- References

- Authors

Features

Core Operations

- Data Extraction: Fetch historical stock data from Yahoo Finance for S&P 500 companies with industry-wide feature generation

- Principal Component Analysis: Dimensionality reduction with explained variance visualization and feature importance analysis

- Hyperparameter Tuning: Distributed Ray Tune optimization with customizable search spaces

- Model Training: Train GRU, Transformer, and Logistic Regression models with full GPU support

- Cross-Validation: K-fold validation using the growing windows method for time series

- Prediction & Forecasting: Two-mode inference system:

- Evaluation Mode: Test model performance on holdout data with comprehensive metrics

- Forecast Mode: Multi-day ahead forecasting (1-30 business days) with autoregressive synthesis

System Features

- Interactive Web GUI: Full-featured interface accessible via single command (

automar gui) - Job Management: Persistent SQLite-based job tracking with filtering, progress monitoring, and result visualization

- Storage Management: Flexible path configuration with validation and per-job output customization

- CLI & Python API: Complete programmatic access for automation and scripting

- Visualization Suite: Interactive Plotly charts for training curves, confusion matrices, PCA analysis, and forecast confidence intervals

Installation

Prerequisites

Important: AuToMaR requires PyTorch, TorchEval, and Ray Tune to be installed separately due to system-specific builds (CPU vs CUDA) and platform compatibility constraints.

Windows Users: Ray Tune does not support Python 3.13 on Windows. Use Python 3.12 instead. Linux users can use Python 3.13 without issues.

Step 1 - Install PyTorch

Visit PyTorch's official installation guide and follow the instructions for your system (CPU vs CUDA, operating system).

Step 2 - Install TorchEval

pip install torcheval

Step 3 - Install Ray Tune

pip install -U "ray[data,train,tune,serve]"

See Ray's installation guide for more details.

Step 4 - Install AuToMaR

pip install automar

From Source (Development)

For development without the web interface (faster, recommended for backend development):

git clone https://codeberg.org/Kzurro/Automar.git

cd Automar

# Install dependencies first (see Prerequisites above)

# Then install automar (without web UI)

pip install -e .

This installs the package without building the web UI. You can still use all CLI commands and the API server, but the automar gui command will not be available.

Building from Source with Web UI

To build the package with the web interface included:

Prerequisites: Node.js and npm must be installed.

Linux/macOS:

git clone https://codeberg.org/Kzurro/Automar.git

cd Automar

# Install Python dependencies (PyTorch, TorchEval, Ray - see Prerequisites section)

# Build and install with web UI

BUILD_WEB=1 pip install -e .

Windows (PowerShell):

git clone https://codeberg.org/Kzurro/Automar.git

cd Automar

# Install Python dependencies (PyTorch, TorchEval, Ray - see Prerequisites section)

# Build and install with web UI

$env:BUILD_WEB=1; pip install -e .

This will install npm dependencies, build the SvelteKit frontend, and install the Python package with web UI support.

Quick Start

Web Interface (Recommended)

Start the web UI with automatic browser opening:

automar gui

This command starts the API server and automatically opens your browser to the web interface, where you can access all features through an intuitive UI.

Alternative: API server only

automar api --host 127.0.0.1 --port 8000

Then manually navigate to http://127.0.0.1:8000 in your browser.

Command Line Interface

For automation and scripting, all operations are available via CLI:

# Extract stock data for a specific ticker

automar extract --ticker AAPL --history 10y

# Perform PCA

automar pca --dataset out/data/AAPL_10y.pkl

# Run hyperparameter tuning

automar tune --ticker AAPL --model gru

# Train a model with optimized parameters

automar train --param-file out/hyper/AAPL_gru_params.toml

# Perform cross-validation

automar crossvalidate --ticker AAPL --model gru

# Make predictions with a trained model

automar predict --model-path out/models/gru/AAPL_model.pth --dataset out/data/AAPL_10y.pkl

Python API

from automar.core.models import GRUModel

from automar.core.preprocessing import loaders

# Your custom code here

How It Works

AuToMaR implements a complete time series forecasting pipeline:

- Data Extraction: Fetches stock panel data from Yahoo Finance for a target company, with optional sector-wide extraction to include all S&P 500 companies in the chosen economic sector

- Feature Engineering: Generates technical indicators following applied deep learning literature

- Dimensionality Reduction (Optional): Apply PCA to sector-wide data to capture industry-level patterns and reduce feature space while preserving variance

- Time Series Transformation: Applies WEASEL-MUSE algorithm for time series classification

- Hyperparameter Optimization: Fine-tunes models using parallel Ray Tune optimization

- Model Training: Trains GRU, Transformer, and Logistic Regression models on either individual stock data or PCA-transformed sector features

- Robust Validation: Cross-validates using the growing windows method

- Prediction: Generates forecasts in two modes:

- Evaluation: Test set performance with comprehensive metrics

- Forecast: Multi-day ahead predictions using autoregressive synthesis

- Visualization: Creates interactive Plotly charts and statistical tables

- Job Tracking: Maintains persistent job history with filtering and result access

Visual Tutorial

This section walks through the complete workflow using the web interface. All screenshots show the actual AuToMaR GUI.

Main Operation Tabs

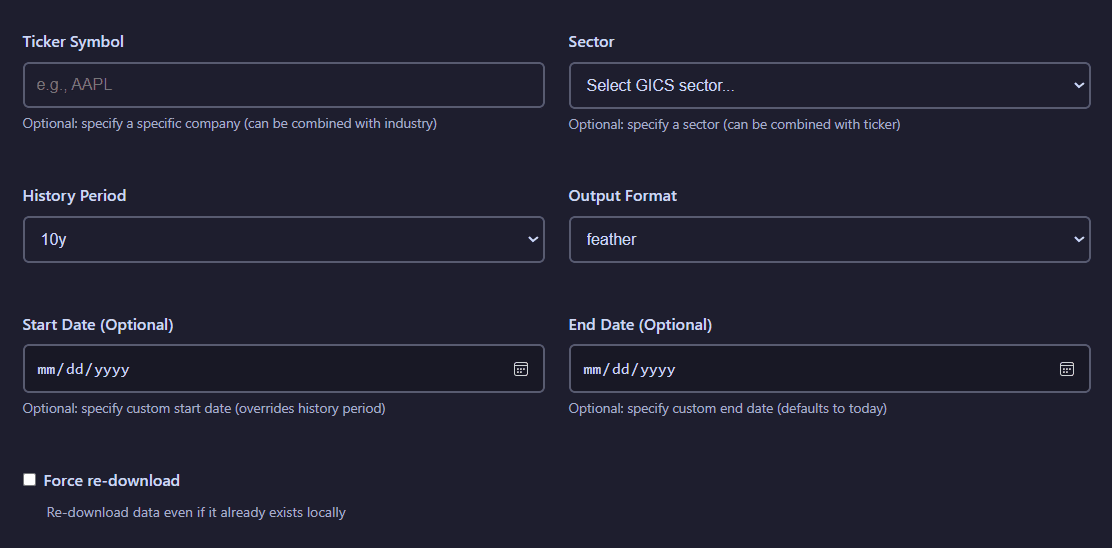

Data Extraction

The Data Extract tab provides an interface for fetching historical stock data from Yahoo Finance. You can configure ticker selection, time periods, output formats, and sector filtering options.

Data extraction configuration panel showing ticker selection, history period, output format, and sector filtering options

Configuration options:

- Ticker Symbol: Select from S&P 500 company ticker symbols via searchable dropdown

- Sector: Select a GICS sector whose S&P 500 companies' data will be used as context

- History Period: Choose historical data period (1y minimum, 10y maximum)

- Output Format: Export as Pickle, Feather, CSV, Excel, Parquet, or SQLite

- Start Date/End Date: Choose a range of dates to download data from, it will override the History Period settting

- Force re-download: If active, data will be downloaded even if it had been previously acquired already

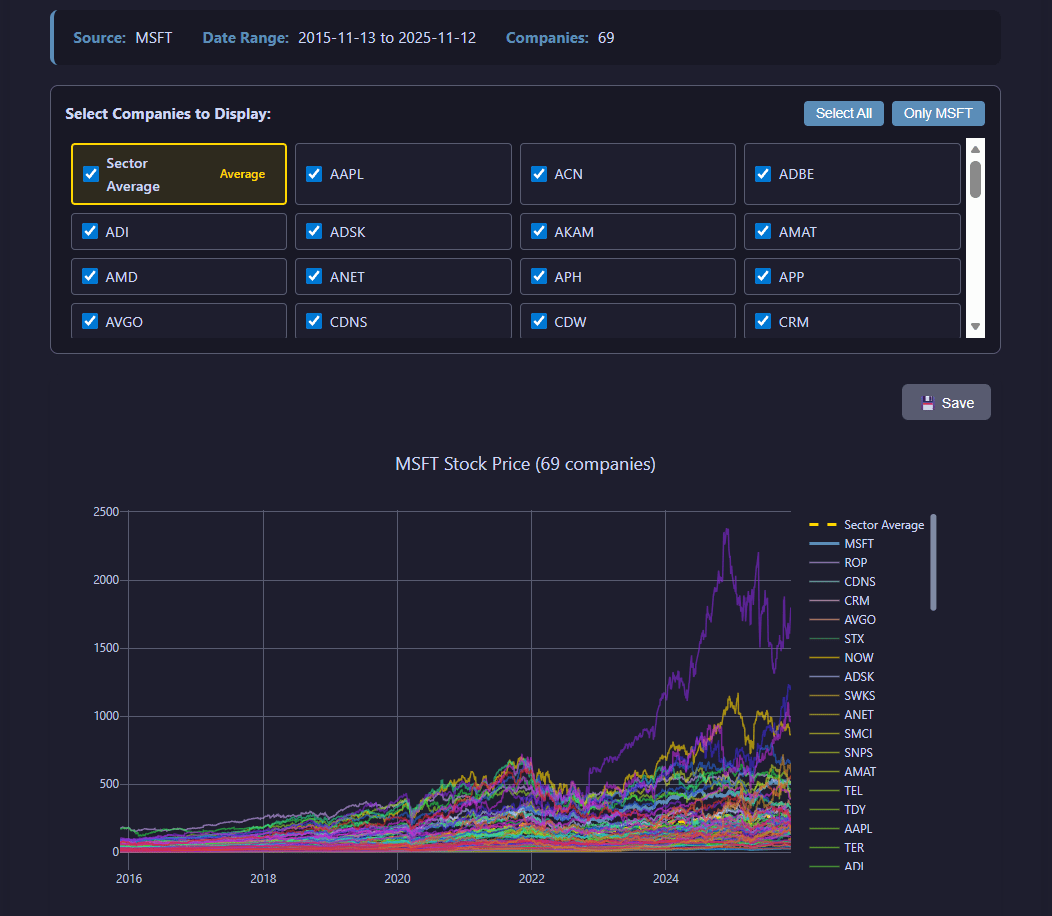

View extraction results visualization

After extraction completes, the job results display a time series for the stock price evolution of the selected companies, including the plot of the mean value in the selected GICS sector.

Extraction results showing the evolution of the closing stock price

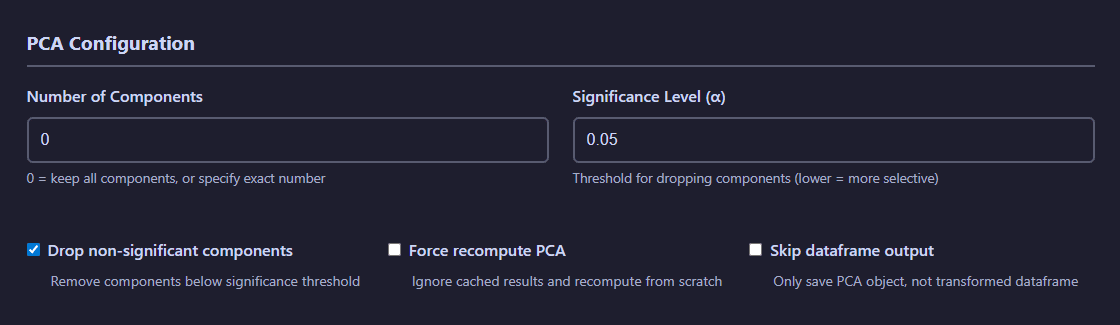

Principal Component Analysis (PCA)

The PCA tab enables dimensionality reduction on your datasets. Configure the number of components, select input data sources (regular files or SQLite databases), and visualize explained variance.

PCA configuration showing dataset selection, component count, output format, and feature visualization options

PCA Configuration:

- Number of Components: Specify target dimensionality for reduction

- Significance level: Defines threshold for the significance test

- Drop non-significant components: If active, non-significant principal components will be ignored

- Force recompute PCA: If active, PCA will be generated even if it already exists

- Skip dataframe output: If active, the transformed dataframe will not be saved

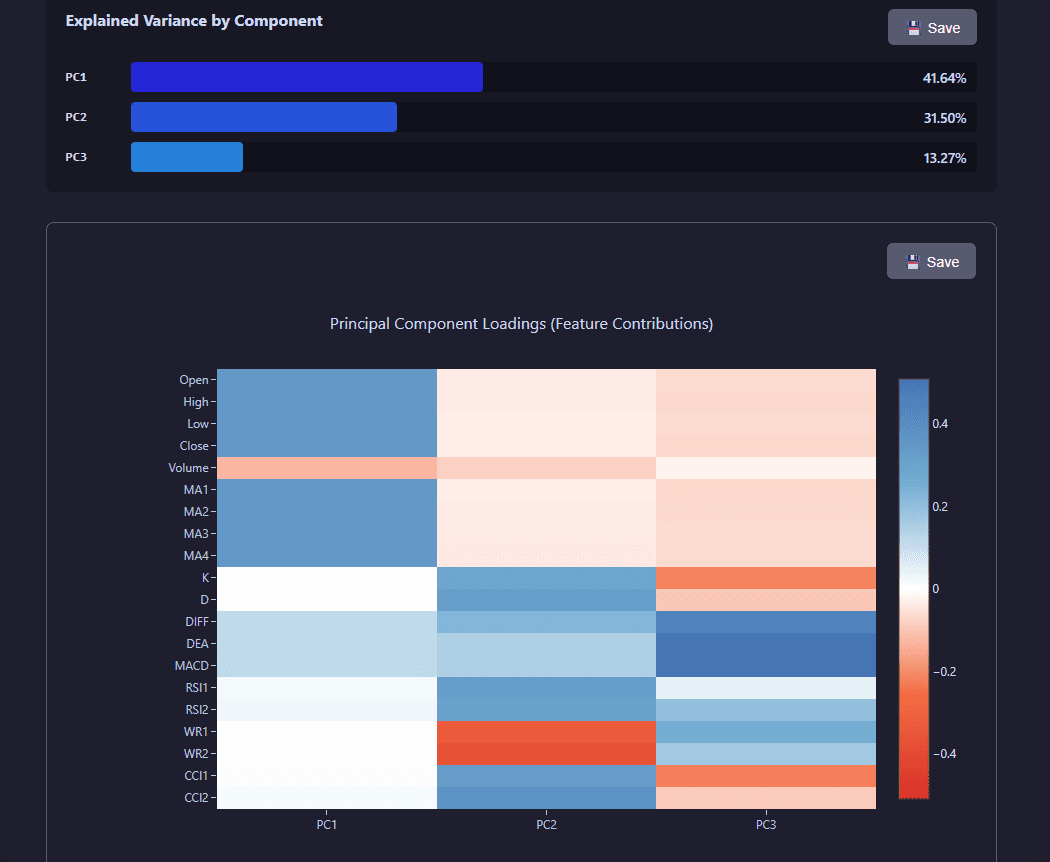

View PCA analysis visualization

PCA results include visualizations showing explained variance ratio, cumulative variance, and principal component contributions across features.

PCA analysis showing explained variance, cumulative variance, and component contributions

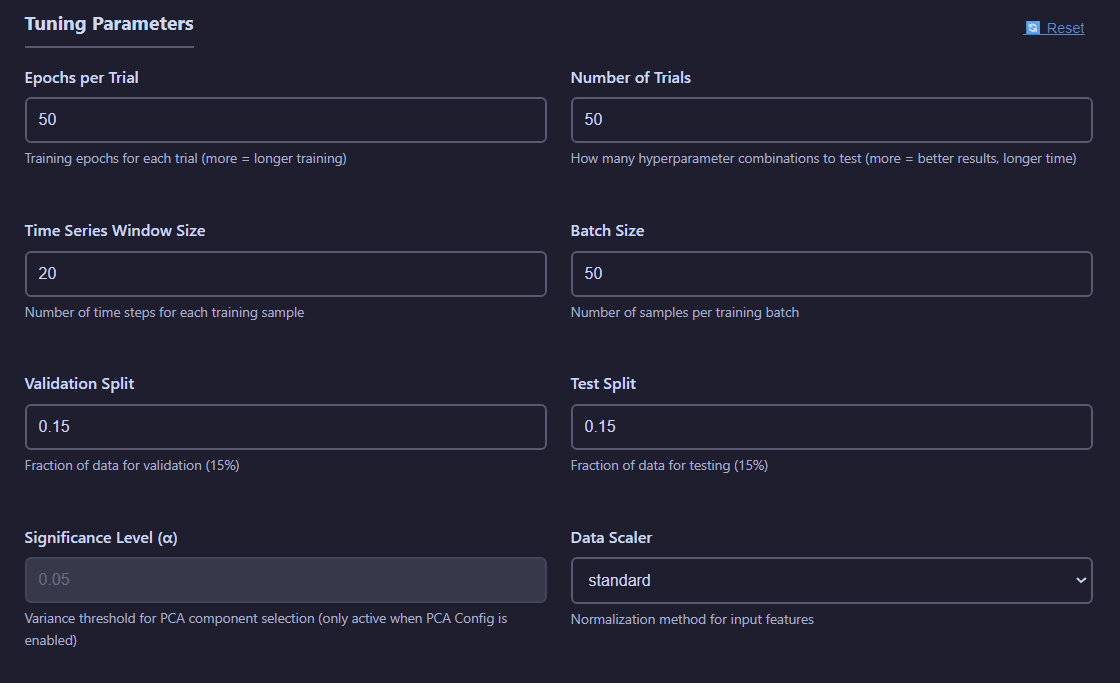

Hyperparameter Tuning

The Tuning tab provides Ray Tune-based hyperparameter optimization for your models. Configure search spaces, resource allocation, and the number of trials to explore.

Hyperparameter tuning interface with model selection, sample count, search space configuration, and compute resources

Tuning Parameters:

- Epochs: Number of training iterations for each trial

- Number of Trials: Number of experiments to test

- Time Series Window Size: Number of observations used for each prediction

- Batch Size: Number of observations in each training batch

- Validation Split: Fraction of the total number of observations used for validation purposes

- Test Split: Fraction of the total number of observations used for testing purposes

- Significance Level: Threshold for accepting a principal component (if PCA per batch is active)

- Data Scaler: Method for data standarization to employ.

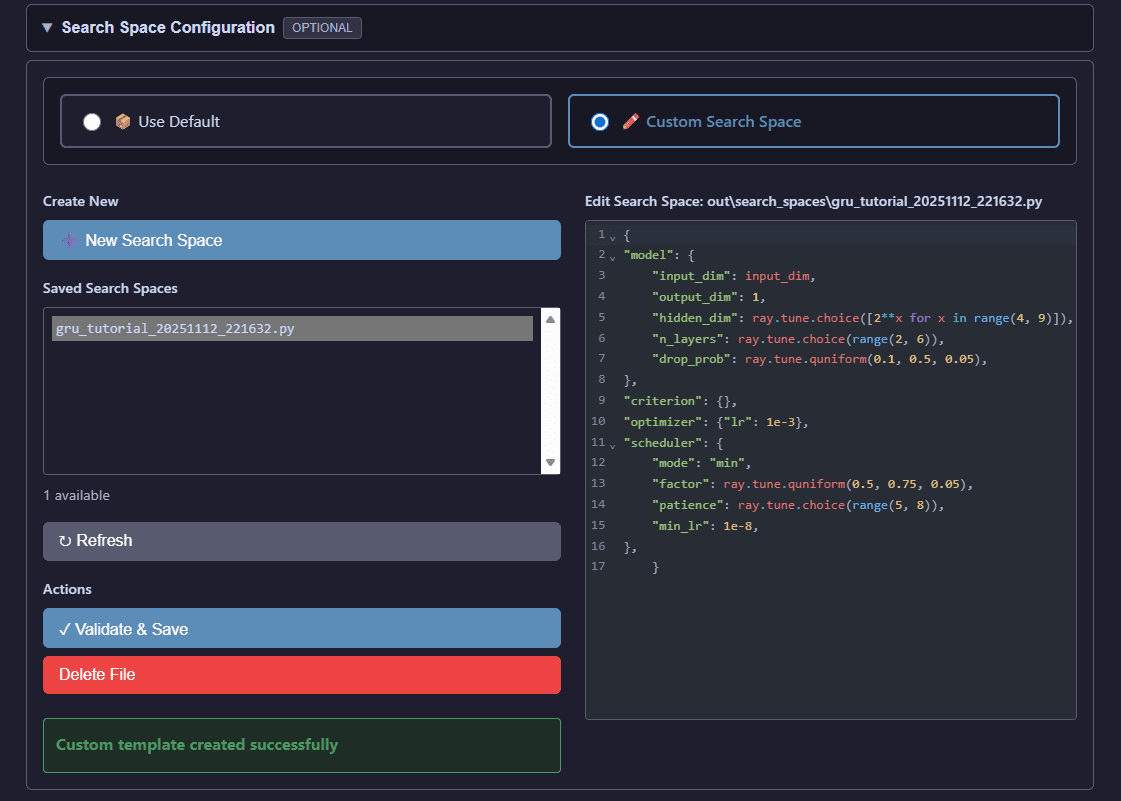

Search Space Configuration:

You can customize Ray Tune search spaces to define the hyperparameter ranges explored during optimization.

Custom search space editor for defining hyperparameter ranges and distributions

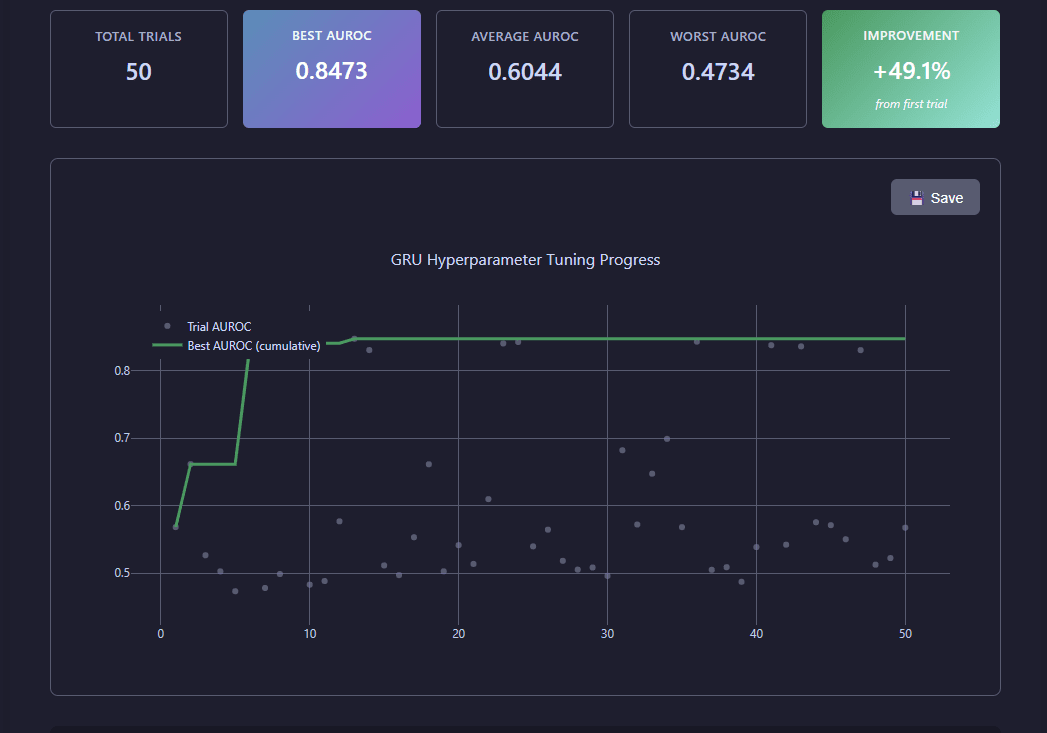

View tuning results visualization

Tuning results display Ray Tune optimization progress, showing AUROC evolution across trials, best hyperparameters found, and performance metrics.

Ray Tune optimization results showing trial performance, best parameters, and convergence metrics

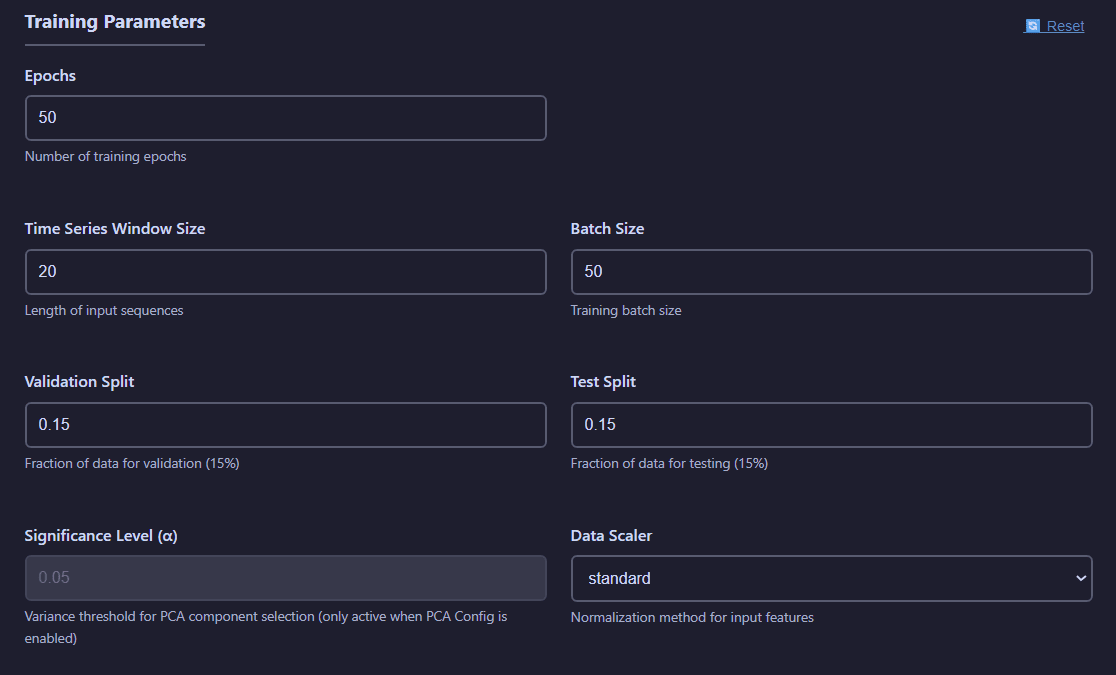

Model Training

The Training tab allows you to train models using optimized hyperparameters from tuning results. Configure training epochs, batch sizes, and compute resources.

Model training configuration with hyperparameter file selection, dataset choice, and training parameters

Training Parameters:

- Epochs: Number of training iterations for each trial

- Time Series Window Size: Number of observations used for each prediction

- Batch Size: Number of observations in each training batch

- Validation Split: Fraction of the total number of observations used for validation purposes

- Test Split: Fraction of the total number of observations used for testing purposes

- Significance Level: Threshold for accepting a principal component (if PCA per batch is active)

- Data Scaler: Method for data standarization to employ.

View training visualizations

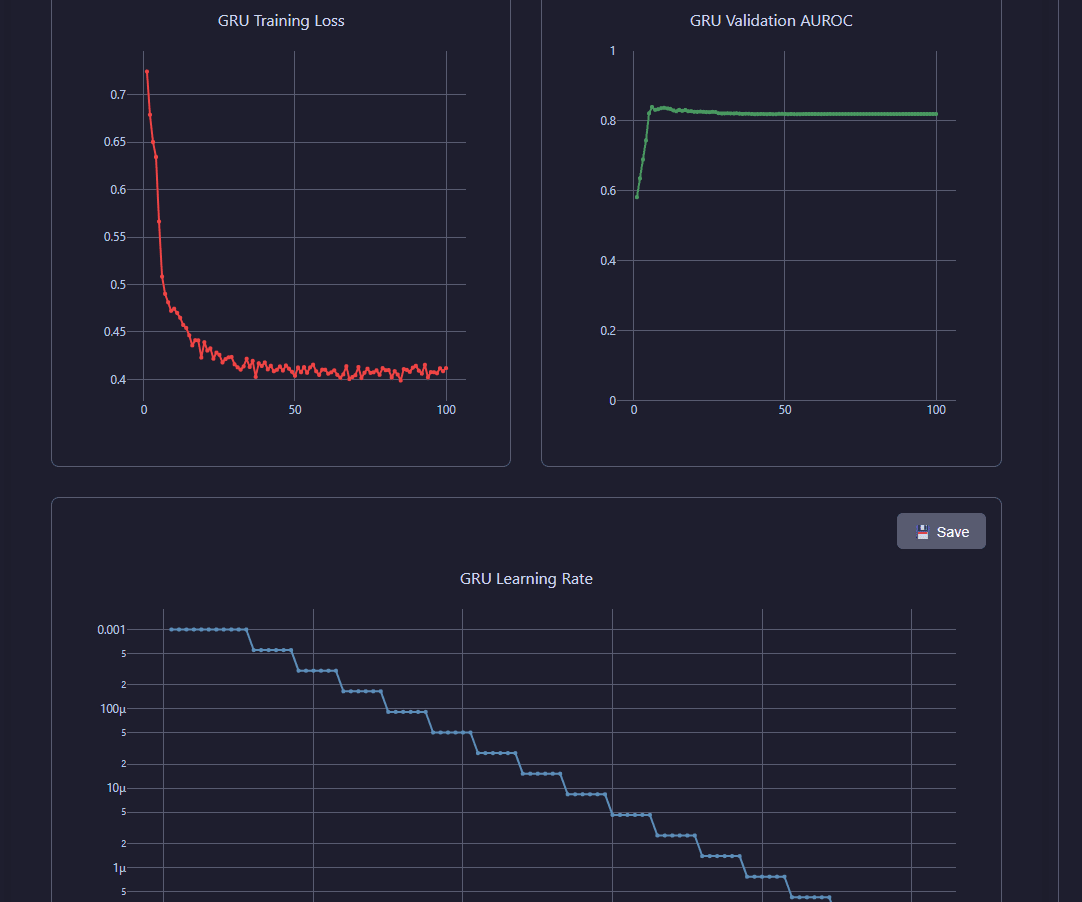

Training Loss Curves:

Inspect training and validation loss evolution throughout the training process.

Training and validation loss curves showing model convergence over epochs

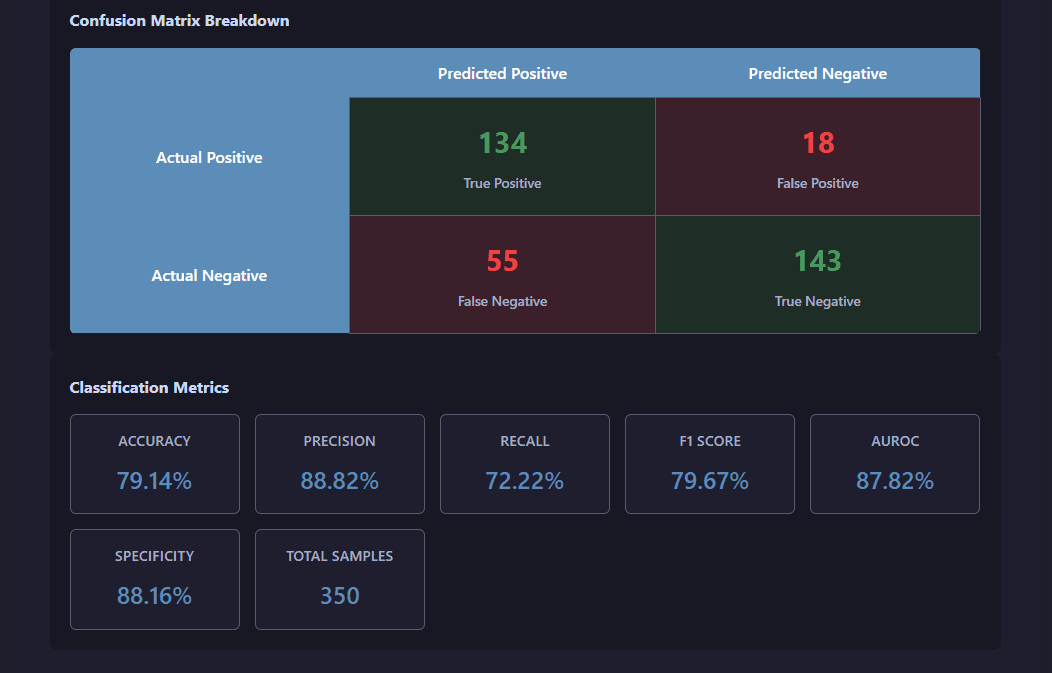

Training Metrics:

View statistics of the test for the trained model: confusion matrix and derived performance indicators.

Comprehensive training metrics including AUROC, accuracy, and learning rate evolution

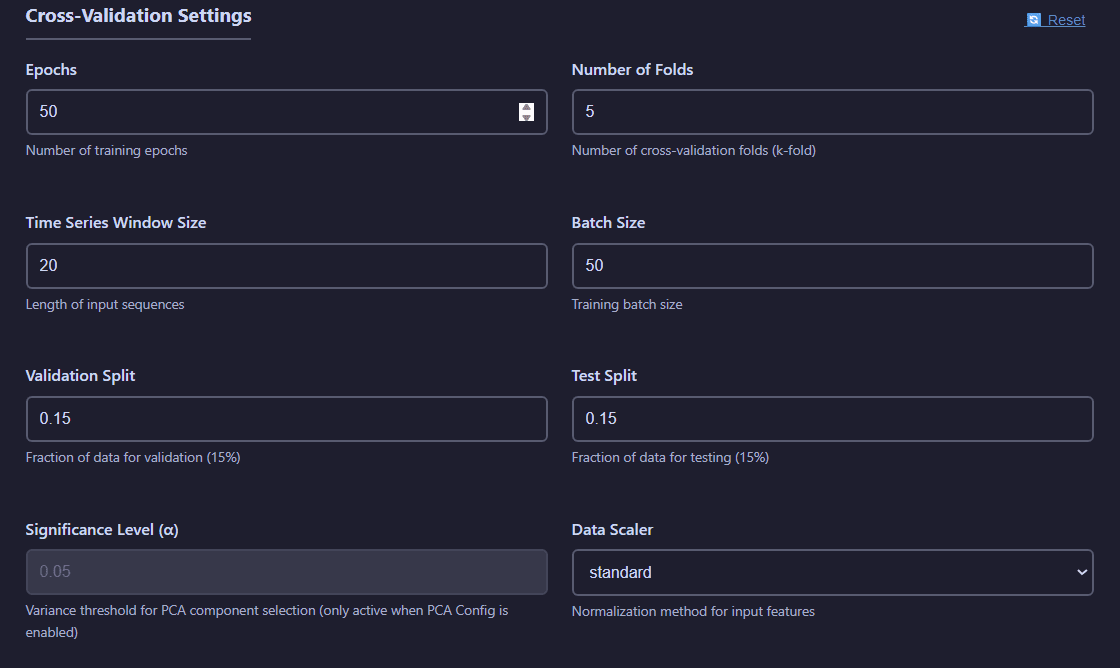

Cross-Validation

The Cross-Validation tab provides robust model evaluation using the growing windows method, specifically designed for time series validation.

Cross-validation configuration showing fold count, model selection, and validation strategy

Cross-Validation Settings:

- Epochs: Number of training iterations for each trial

- Number of Folds: Number of growing windows models will be trained on.

- Number of Trials: Number of experiments to test

- Time Series Window Size: Number of observations used for each prediction

- Batch Size: Number of observations in each training batch

- Validation Split: Fraction of the total number of observations used for validation purposes

- Test Split: Fraction of the total number of observations used for testing purposes

- Significance Level: Threshold for accepting a principal component (if PCA per batch is active)

- Data Scaler: Method for data standarization to employ.

View cross-validation visualizations

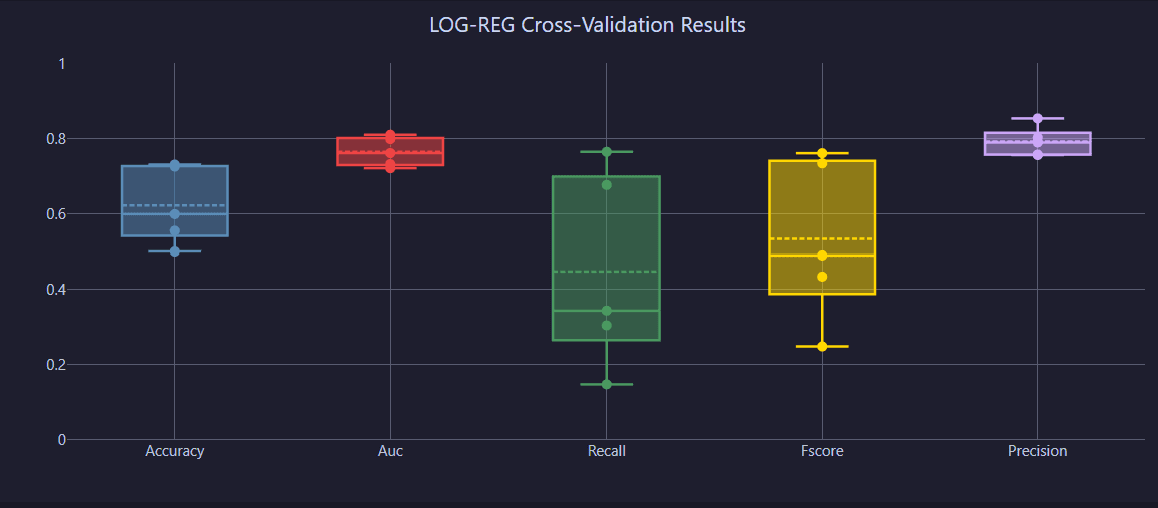

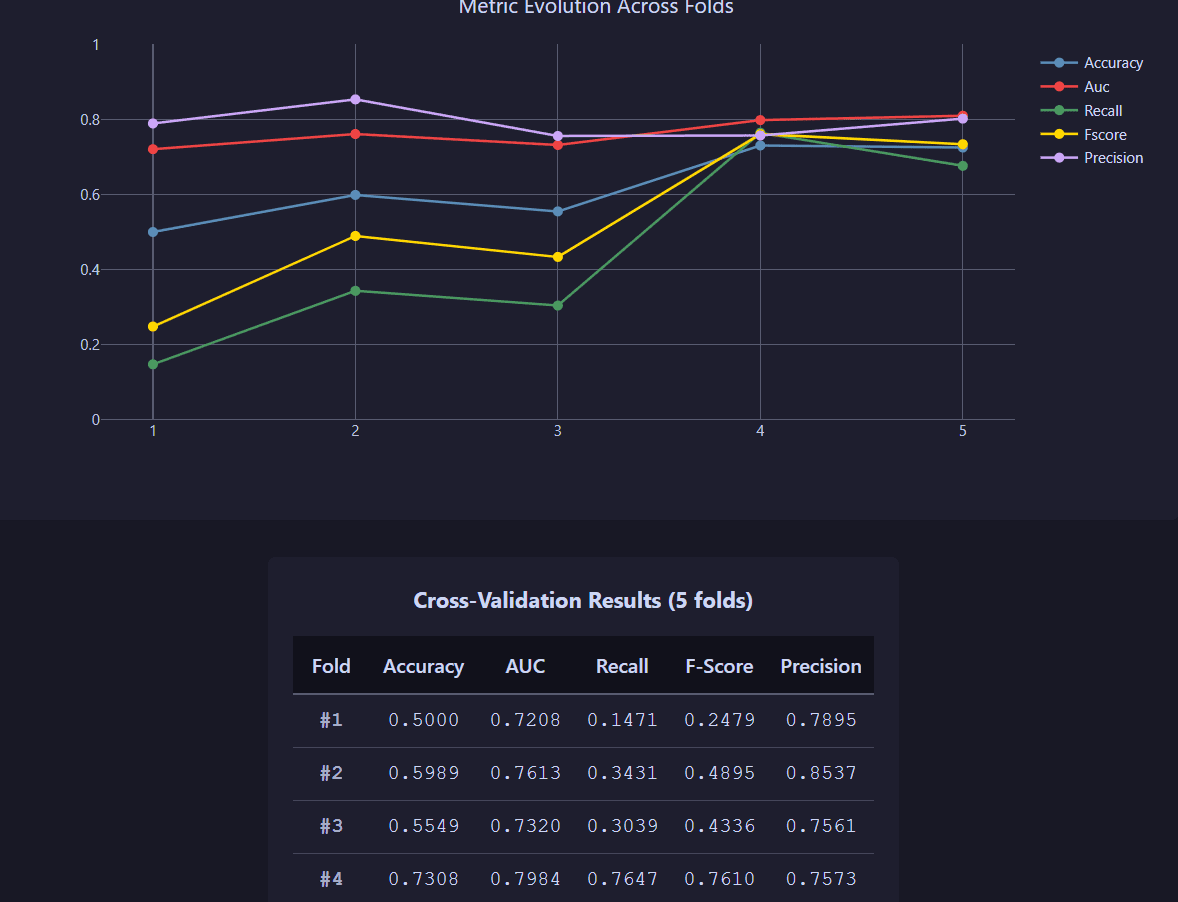

Fold Results:

Performance metrics across all validation folds with statistical distributions.

Performance metrics distribution across validation folds

Detailed Metrics:

Analyze detailed statistics and performance distributions for each fold.

Detailed fold-by-fold performance analysis with metric breakdowns

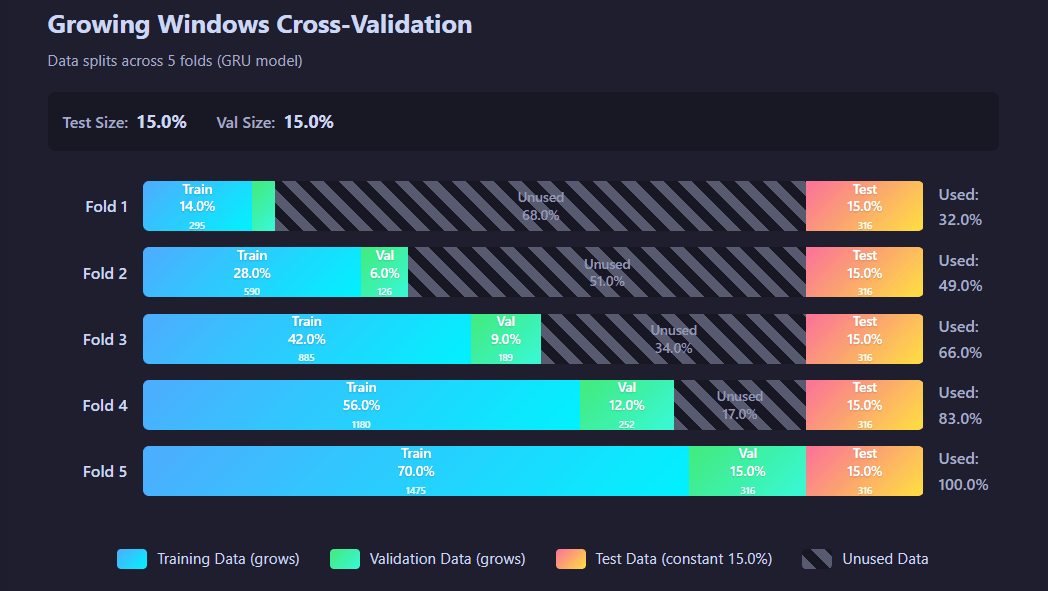

Growing windows structure:

Distribution of available data across the requested number of folds, detailed by training, validation and test class.

Structure of data distribution in each fold

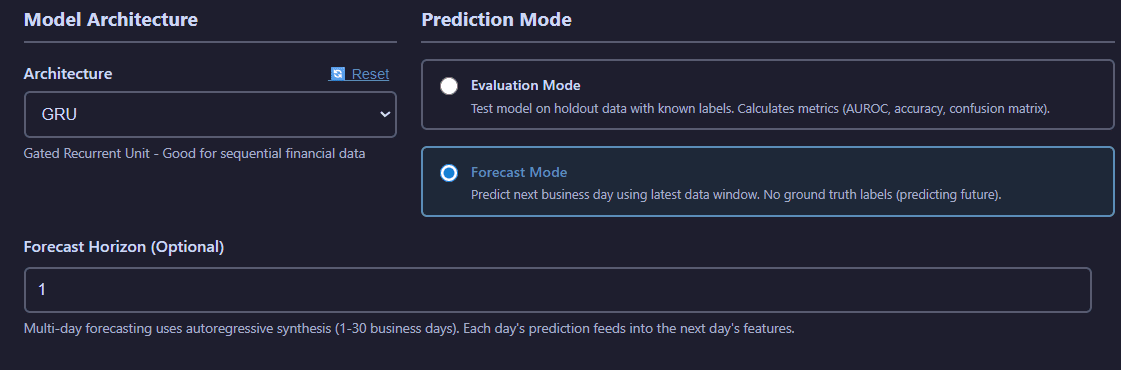

Predictions

The Prediction tab offers model inference in two modes: Evaluation (test set performance) and Forecast (multi-day ahead predictions).

Prediction interface with mode selection, model file picker, and forecast horizon configuration

Prediction Configuration:

- Mode Selection:

- Evaluation Mode: Test model performance on holdout data with known labels

- Forecast Mode: Multi-day forecasting (1-30 business days) using autoregressive synthesis

- Forecast Horizon: Number of days ahead to predict (Forecast mode only)

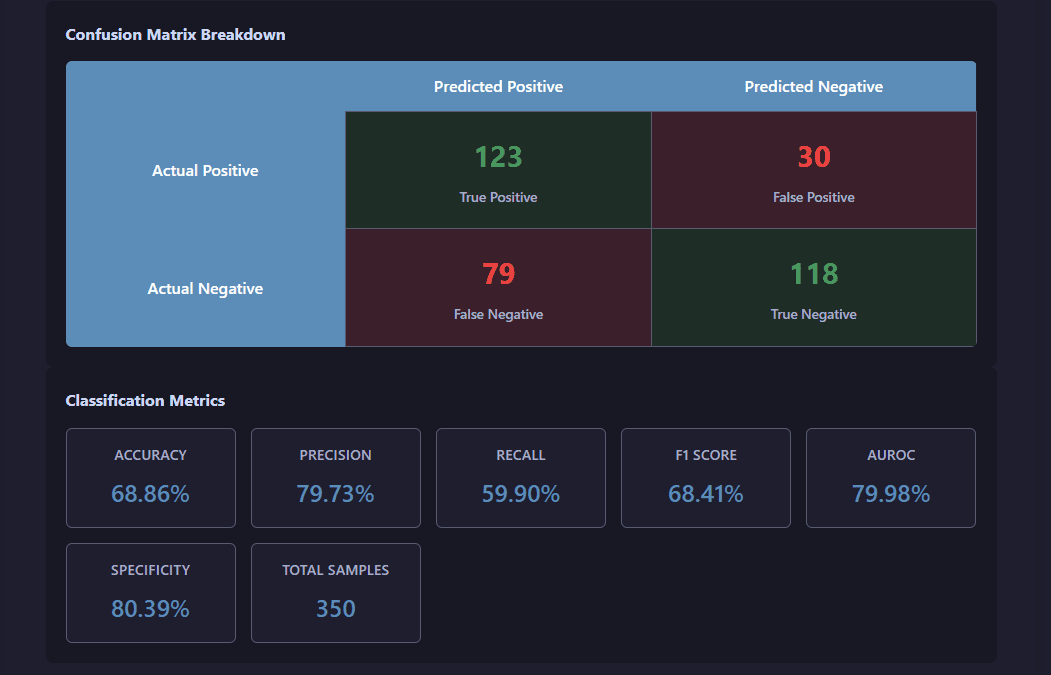

View evaluation mode visualization

Evaluation mode provides comprehensive performance analysis of the pre-trained model running on the new inputted data, including the confusion matrix and classification metrics.

Evaluation results showing prediction accuracy, confusion matrix, and performance metrics

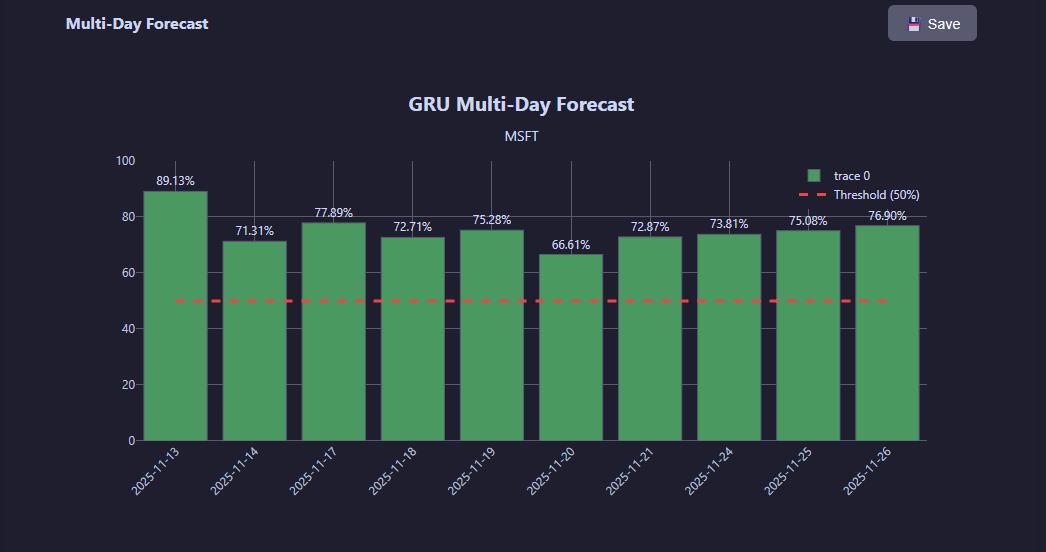

View forecast mode visualization

Forecast mode generates multi-day ahead predictions with confidence intervals and historical price context.

Multi-day forecast with confidence intervals, probability distributions, and historical trend context

Shared Components

The web interface includes several powerful shared components that appear across multiple operation tabs.

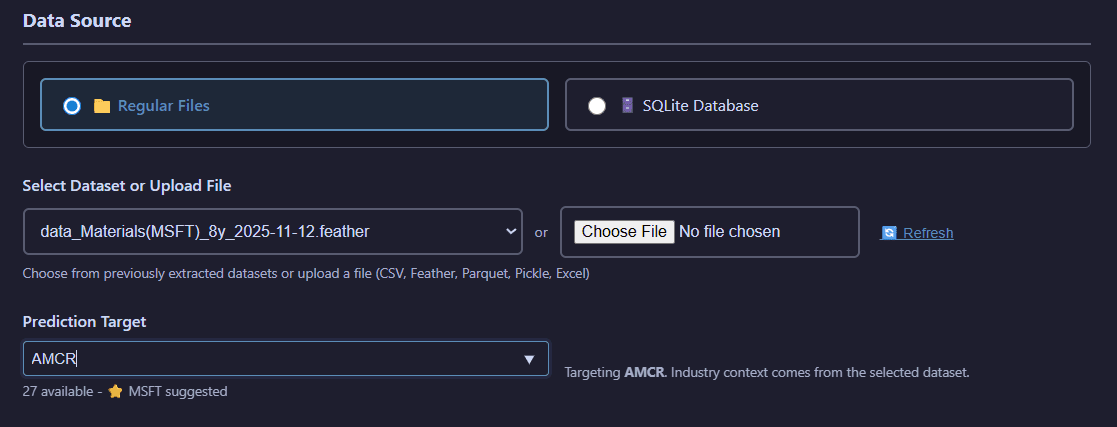

Data Source Selection

Choose between regular file selection and SQLite database mode with advanced filtering capabilities.

Regular File Mode:

Regular file selection with ticker-specific filtering for quick dataset location

Browse and select files from the filesystem with optional ticker-based filtering to quickly find datasets for specific companies.

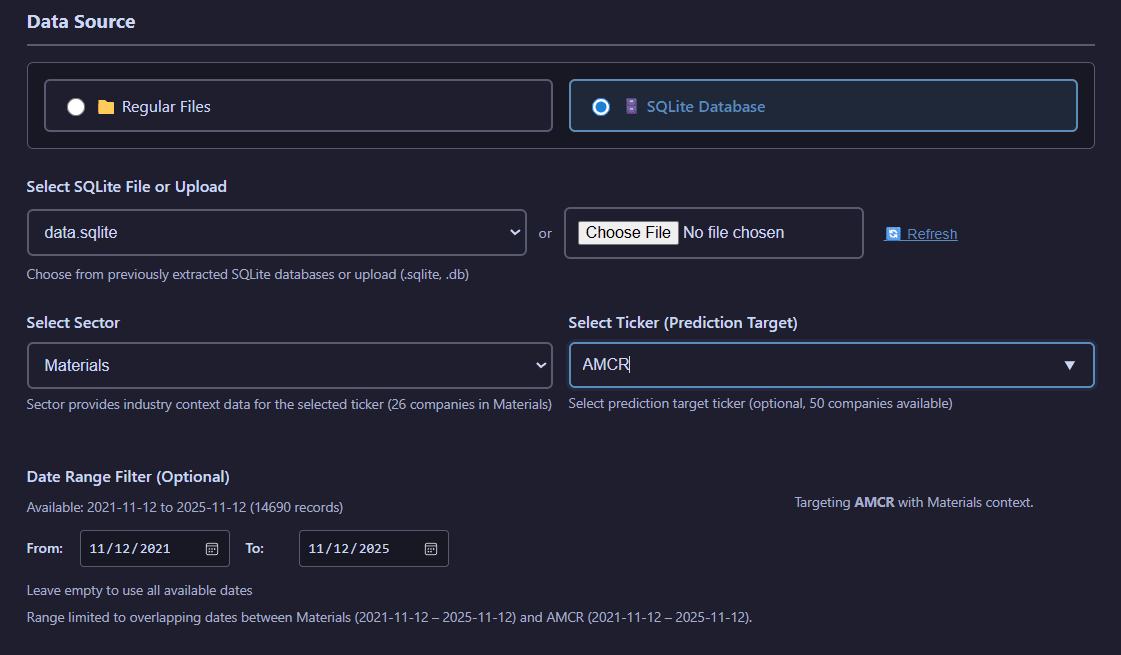

SQLite Database Mode:

SQLite database selection with sector filtering, ticker selection, and date range controls

Query SQLite databases with advanced filtering including sector selection, target company specification, and date range constraints.

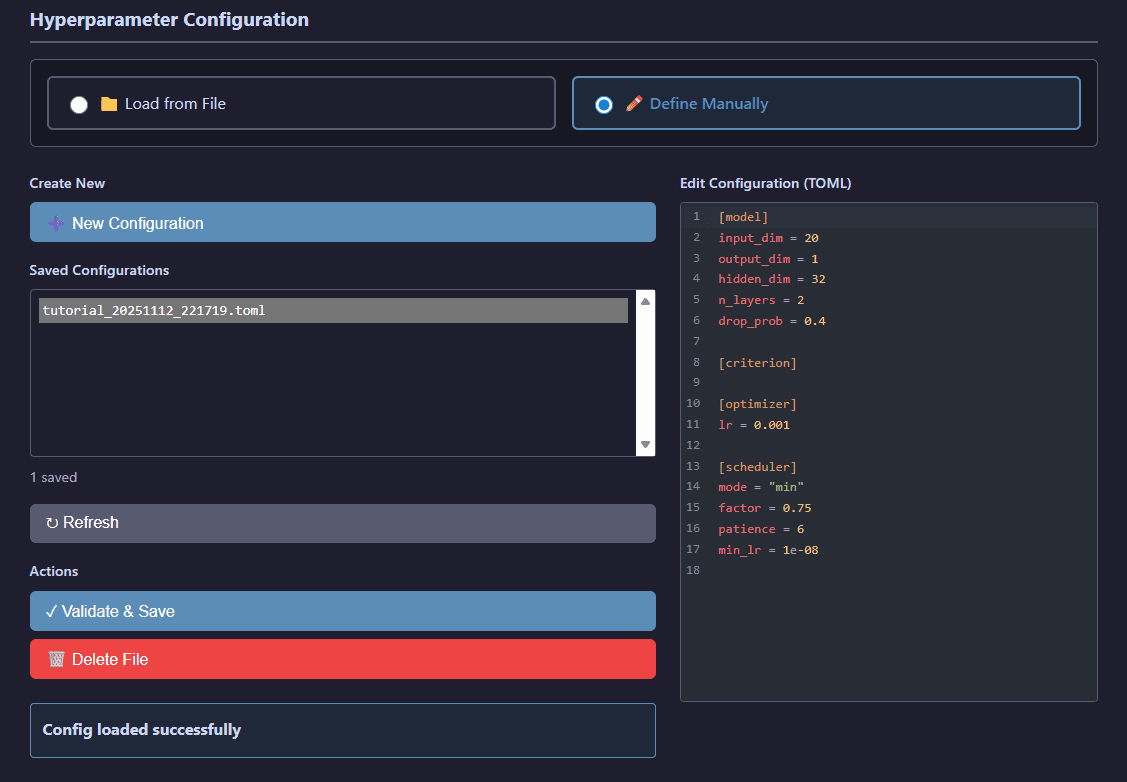

Hyperparameter Configuration

Load and manage model hyperparameters from TOML configuration files generated by tuning operations.

Hyperparameter file selector showing available configurations organized by model type

Browse hyperparameter configuration files organized by model architecture (GRU, Transformer, Logistic Regression) and select optimized settings from previous tuning runs.

Compute Resources

Configure CPU/GPU allocation and memory limits for computationally intensive operations.

Compute resource allocation panel for device selection, CPU cores, and memory limits

Resource Configuration:

- Device: Select CPU or GPU (CUDA) execution

- CPU Cores: Number of CPU cores to utilize for parallel processing

- Memory: RAM allocation limits for data loading and processing

- GPU Memory: VRAM limits for GPU-accelerated operations

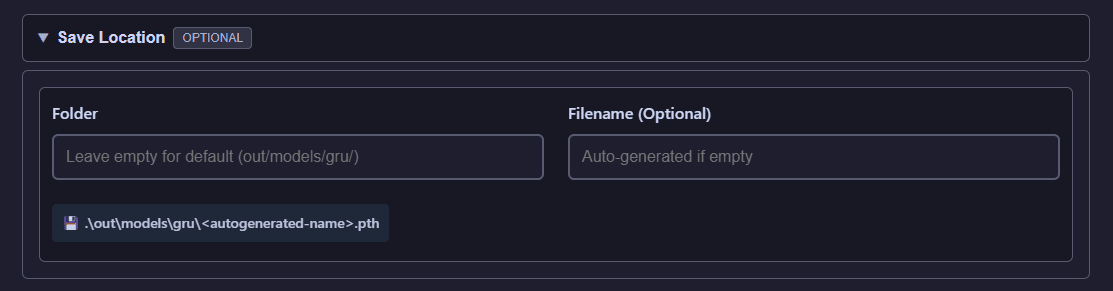

Save Location

Override default storage configuration on a per-job basis with custom output paths.

Custom save location selector for per-job output path overrides

Specify a custom output directory for individual operations, allowing you to organize results outside the default storage configuration.

System Features

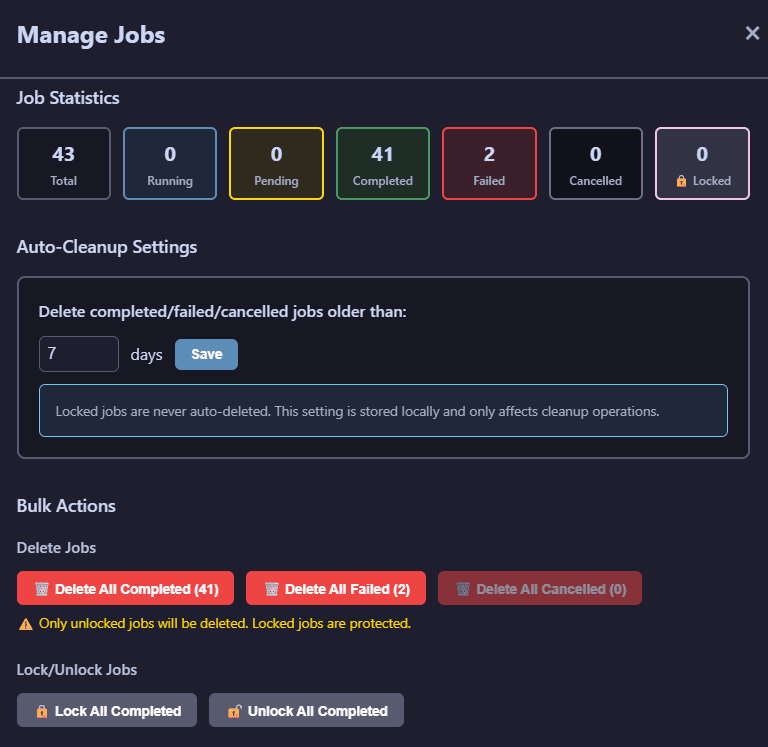

Job Management

Track all operations through the persistent job management system with filtering and real-time progress monitoring.

Job management panel showing active and completed jobs with filtering options

Job Management Features:

- Quantifies number of jobs in each status.

- Quick management of jobs in bulk: lock all, unlock all, delete all. Check the job card in Job Status for manipulating specific jobs.

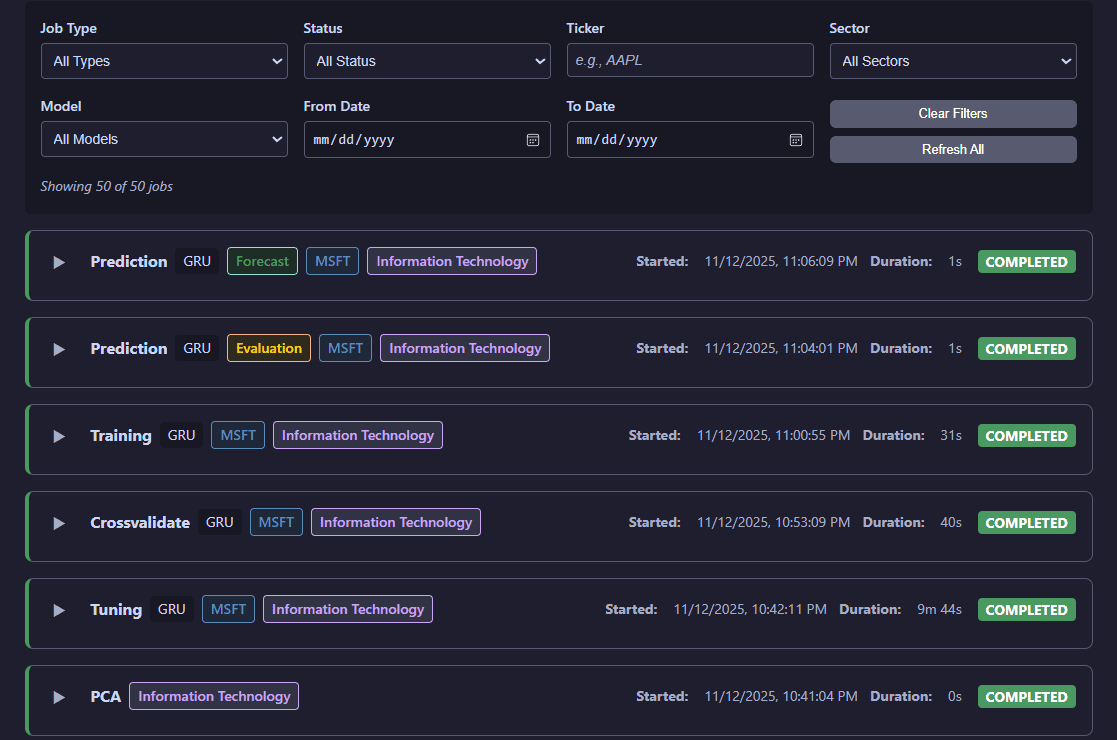

Job Status

Access comprehensive details for individual operations including logs, parameters, and result visualizations.

Detailed job status view with execution logs, parameters, and visualization access

Job Status Provides:

- Detailed execution logs and progress tracking

- Complete job parameters and configuration

- Output file locations and results

- Direct access to interactive visualizations for completed operations

- Status updates and error diagnostics for failed jobs

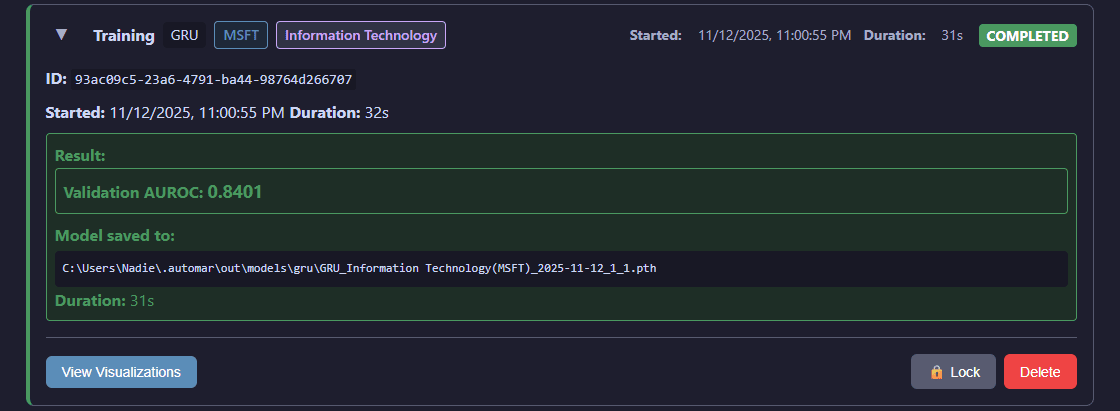

Individual Job Card:

Each job in the Job Status tab displays as an expandable card with detailed information and controls.

Expanded job card showing detailed information, visualization access, and management options (lock, unlock, delete)

The expanded card for each job provides quick access to the lock/unlock function (preventing both its automated and bulk deletion), delete function, and to view visualizations for succesful jobs.

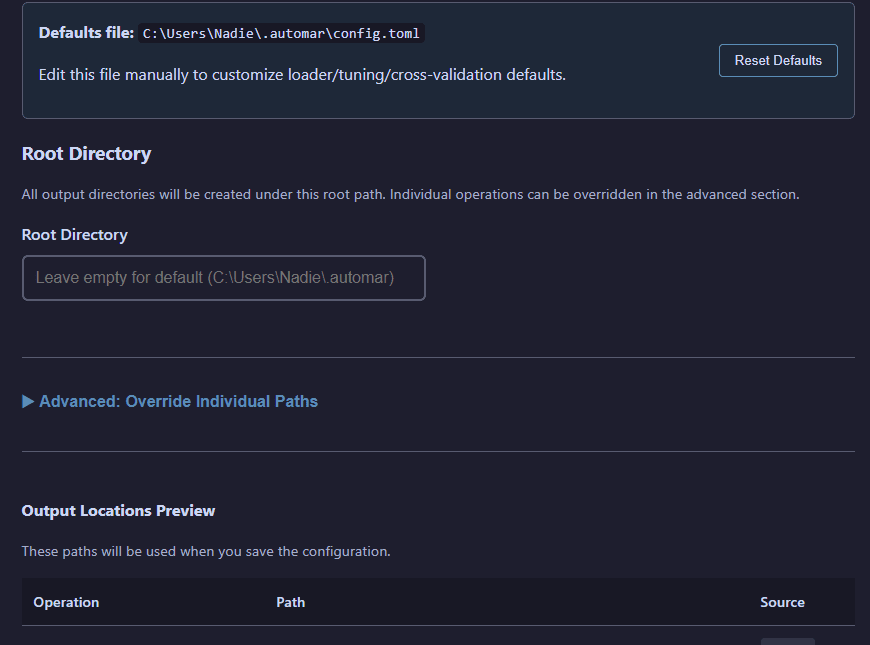

Storage Configuration

Configure custom storage paths through the Settings feature accessible from the top navigation bar.

Settings interface for customizing output paths with validation

Storage Management:

- View current storage paths for all operations (data, models, PCA, predictions, etc.)

- Override root directory to change all operation paths at once

- Override individual operation paths for granular control

- Validate paths before saving to prevent configuration errors

- Changes take effect immediately without requiring server restart

Configuration

AuToMaR uses TOML configuration files for system-wide settings. A default config.toml is provided with sensible defaults. When running the web UI, these defaults are loaded directly from schema.py, then overridden by $HOME/.automar/config.toml (auto-created on first launch) before reaching the frontend. Edit that file manually to customize loader/tuning/cross-validation defaults or use the Settings modal to reset it back to schema values.

Storage Configuration

AuToMaR provides flexible path configuration with a 3-tier priority system:

- Custom paths in config.toml - Highest priority

- AUTOMAR_DATA_DIR environment variable - Medium priority

- Default location - Lowest priority (repository root or

~/.automar/)

Using the Web UI (Recommended)

The web interface includes a Manage Storage button in the top navigation bar that opens a configuration modal. You can view current paths, override the root directory or individual operation paths, validate configurations, and apply changes immediately without restarting the server.

Additionally, all operation tabs include an optional Save Location field for per-job path overrides.

Manual Configuration

Edit config.toml directly to configure storage paths:

[paths]

# Override the root directory (all operations use this as base)

root = "/custom/path/to/data"

# Or override individual operation directories

data = "/custom/path/to/datasets"

models = "/custom/path/to/models"

pca = "/custom/path/to/pca"

Environment Variable

Set the AUTOMAR_DATA_DIR environment variable to change the default storage location:

Linux/macOS:

export AUTOMAR_DATA_DIR=/path/to/custom/directory

Windows (PowerShell):

$env:AUTOMAR_DATA_DIR="C:\path\to\custom\directory"

Output Structure

Results are stored following the 3-tier path configuration priority. The default output structure within the configured location is:

out/

├── data/ # Extracted datasets (.pkl, .feather, .xlsx, .csv, .parquet, .sqlite)

├── pca/ # PCA transformations (.joblib) with feature names

│ └── data/ # PCA-transformed dataframes (.feather)

├── hyper/ # Hyperparameter configurations (.toml)

│ ├── gru/ # GRU model hyperparameters

│ ├── transformer/ # Transformer model hyperparameters

│ └── logreg/ # Logistic Regression hyperparameters

├── models/ # Trained model weights (.pth) with training context metadata

│ ├── gru/ # GRU model checkpoints

│ ├── transformer/ # Transformer model checkpoints

│ └── logreg/ # Logistic Regression model checkpoints

├── cross/ # Cross-validation results (.pkl)

├── preds/ # Prediction results (.pkl, .json)

│ ├── eval/ # Evaluation mode predictions with metrics

│ └── forecast/ # Forecast mode predictions (multi-day)

├── jobs/ # Job tracking database (.db)

├── ray/ # Ray Tune trial reports

└── search_spaces/ # Custom search spaces for tuning (.py)

Building Distribution Packages

To create distribution packages (wheels) for PyPI or local distribution:

Without Web UI (API and CLI only - smaller package):

python -m build

With Web UI (includes compiled frontend - recommended for end users):

Linux/macOS:

BUILD_WEB=1 python -m build

Windows (PowerShell):

$env:BUILD_WEB=1; python -m build

This creates:

dist/automar-*.tar.gz- Source distributiondist/automar-*-py3-none-any.whl- Wheel distribution

The wheel can be installed with pip install dist/automar-*.whl

Note: Building with

BUILD_WEB=1requires Node.js and npm installed. The build process takes longer (~30-60 seconds extra) but creates a complete package with the web UI ready to use.

Requirements

- Python >= 3.12 (Python 3.13 not supported on Windows due to Ray Tune compatibility)

- PyTorch 2.4.0+

- TorchEval 0.0.7+

- Ray Tune 2.34.0+

- See pyproject.toml for complete dependency list

Developed with

- Python 3.12

- PyTorch 2.4.0

- Scikit-Learn 1.5.1

- Sktime 0.31.0

- Ray Tune 2.34.0

- SvelteKit 1.20.4

- Plotly.js

References

Zhao, J., Zeng, D., Liang, S., Kang, H., & Liu, Q. (2021). Prediction model for stock price trend based on recurrent neural network. Journal of Ambient Intelligence and Humanized Computing, 12(1), 745-753. https://doi.org/10.1007/s12652-020-02057-0

Authors

- Alejandro Gil (Kzurro)

- Sergio Pablo-García

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file automar-26.6.22.tar.gz.

File metadata

- Download URL: automar-26.6.22.tar.gz

- Upload date:

- Size: 2.0 MB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.13.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

63a690ea9657f9973a4124a10d7d66c89b6c251868c48eb014d1d0a14dacc14f

|

|

| MD5 |

f243da13f110ed3402f426ac625fc9f4

|

|

| BLAKE2b-256 |

763f1623e1dc7e64d1045054b882ca54302dde47eb59b21fc07f14cb215ae480

|

File details

Details for the file automar-26.6.22-py3-none-any.whl.

File metadata

- Download URL: automar-26.6.22-py3-none-any.whl

- Upload date:

- Size: 2.0 MB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.13.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

681b260bbe3473ebf2f11b890e25f950e3b521b2ef9d68c39a069db0f1bd1df1

|

|

| MD5 |

c7879a17c3a9c4ddb0ffddf661ffb8e1

|

|

| BLAKE2b-256 |

67a43de2e0e2d19f68c9f8536114c06e26c34b3b50d70fa7a371d948e3fc76eb

|