Conformal classifiers, regressors, and predictive systems (crepes)

Project description

crepes is a Python package for conformal prediction that implements conformal classifiers,

regressors, and predictive systems on top of any standard classifier

and regressor, turning the original predictions into

well-calibrated p-values and cumulative distribution functions, or

prediction sets and intervals with coverage guarantees.

The crepes package implements standard and Mondrian conformal

classifiers as well as standard, normalized and Mondrian conformal

regressors and predictive systems. While the package allows you to use

your own functions to compute difficulty estimates, non-conformity

scores and Mondrian categories, there is also a separate module,

called crepes.extras, which provides some standard options for

these. For testing the underlying assumption of exchangeability,

you may use the classes in the module crepes.martingales.

Installation

From PyPI

pip install crepes

From conda-forge

conda install conda-forge::crepes

Documentation

For the complete documentation, see crepes.readthedocs.io.

Quickstart

Let us illustrate how we may use crepes to generate and apply

conformal classifiers with a dataset from

www.openml.org, which we first split into a

training and a test set using train_test_split from

sklearn, and then further split the

training set into a proper training set and a calibration set:

from sklearn.datasets import fetch_openml

from sklearn.model_selection import train_test_split

dataset = fetch_openml(name="qsar-biodeg", parser="auto")

X = dataset.data.values.astype(float)

y = dataset.target.values

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.5)

X_prop_train, X_cal, y_prop_train, y_cal = train_test_split(X_train, y_train,

test_size=0.25)

We now "wrap" a random forest classifier, fit it to the proper

training set, and fit a standard conformal classifier through the

calibrate method:

from crepes import WrapClassifier

from sklearn.ensemble import RandomForestClassifier

rf = WrapClassifier(RandomForestClassifier(n_jobs=-1))

rf.fit(X_prop_train, y_prop_train)

rf.calibrate(X_cal, y_cal)

We may now produce p-values for the test set (an array with as many columns as there are classes):

rf.predict_p(X_test)

array([[0.00427104, 0.74842304],

[0.07874355, 0.2950549 ],

[0.50529983, 0.01557963],

...,

[0.8413356 , 0.00201167],

[0.84402215, 0.00654927],

[0.29601955, 0.07766093]])

We can also get prediction sets, here at the 99% confidence level:

rf.predict_set(X_test, confidence=0.99)

[['2'],

['1', '2'],

['1', '2'],

...,

['1'],

['1'],

['1', '2']]

If we prefer the prediction sets to be represented by binary vectors indicating presence (1) or absence (0) of the class labels that correspond to the columns, we can request this by:

rf.predict_set(X_test, labels=False, confidence=0.99)

array([[0, 1],

[1, 1],

[1, 1],

...,

[1, 0],

[1, 0],

[1, 1]])

Since we have access to the true class labels, we can evaluate the conformal classifier (here using all available metrics which is the default), at the 99% confidence level:

rf.evaluate(X_test, y_test, confidence=0.99)

{'error': 0.007575757575757569,

'avg_c': 1.6136363636363635,

'one_c': 0.38636363636363635,

'empty': 0.0,

'ks_test': 0.0030978768439862566,

'time_fit': 9.5367431640625e-07,

'time_evaluate': 0.024116039276123047}

To control the error level across different groups of objects of

interest, we may use so-called Mondrian conformal classifiers. A

Mondrian conformal classifier is formed by providing a function or a

MondrianCategorizer (defined in crepes.extras) as an additional

argument, named mc, for the calibrate method.

For illustration, we will use the predicted labels of the underlying model to form the categories. Note that the prediction sets are generated for the test objects using the same categorization (under the hood).

rf_mond = WrapClassifier(rf.learner)

rf_mond.calibrate(X_cal, y_cal, mc=rf_mond.predict)

rf_mond.predict_set(X_test)

[['2'],

['1', '2'],

['1'],

...,

['1'],

['1'],

['1', '2']]

The class-conditional conformal classifier is a special type of Mondrian

conformal classifier, for which the categories are formed by the true labels;

we can generate one by setting class_cond=True in the call to calibrate

rf_classcond = WrapClassifier(rf.learner)

rf_classcond.calibrate(X_cal, y_cal, class_cond=True)

rf_classcond.evaluate(X_test, y_test, confidence=0.99)

{'error': 0.0018939393939394478,

'avg_c': 1.740530303030303,

'one_c': 0.25946969696969696,

'empty': 0.0,

'ks_test': 0.11458837583733483,

'time_fit': 7.152557373046875e-07,

'time_evaluate': 0.06147575378417969}

When employing an inductive conformal predictor, the predicted

p-values (and consequently the errors made) for a test set are not

independent. Semi-online conformal predictors can however make them

independent by updating the calibration set immediately after each

prediction (assuming that the true label is then available). We can

turn the conformal classifiers into semi-online conformal classifiers

by enabling online calibration, i.e., setting online=True when calling

the above methods, while also providing the true labels, e.g.,

rf_classcond.predict_p(X_test, y_test, online=True)

array([[8.13837566e-05, 8.86436603e-01],

[6.60518590e-02, 4.02350293e-01],

[4.28646783e-01, 4.29930890e-02],

...,

[7.05118942e-01, 9.45056960e-03],

[7.27003479e-01, 1.27347189e-02],

[1.76403756e-01, 1.21434924e-01]])

Similarly, we can evaluate the conformal classifier while using online calibration:

rf_classcond.evaluate(X_test, y_test, confidence=0.99, online=True)

{'error': 0.007575757575757569,

'avg_c': 1.6117424242424243,

'one_c': 0.38825757575757575,

'empty': 0.0,

'ks_test': 0.14097384777782784,

'time_fit': 1.9073486328125e-06,

'time_evaluate': 0.05298352241516113}

Let us also illustrate how crepes can be used to generate conformal

regressors and predictive systems. Again, we import a dataset from

www.openml.org, which we split into a

training and a test set and then further split the training set into a

proper training set and a calibration set:

from sklearn.datasets import fetch_openml

from sklearn.model_selection import train_test_split

dataset = fetch_openml(name="house_sales", version=3, parser="auto")

X = dataset.data.values.astype(float)

y = dataset.target.values.astype(float)

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.5)

X_prop_train, X_cal, y_prop_train, y_cal = train_test_split(X_train, y_train,

test_size=0.25)

Let us now "wrap" a RandomForestRegressor from

sklearn using the class WrapRegressor

from crepes and fit it (in the usual way) to the proper training

set:

from sklearn.ensemble import RandomForestRegressor

from crepes import WrapRegressor

rf = WrapRegressor(RandomForestRegressor())

rf.fit(X_prop_train, y_prop_train)

We may now fit a conformal regressor using the calibration set through

the calibrate method:

rf.calibrate(X_cal, y_cal)

The conformal regressor can now produce prediction intervals for the test set, here using a confidence level of 99%:

rf.predict_int(X_test, confidence=0.99)

array([[1938866.06, 3146372.54],

[ 225335.1 , 1432841.58],

[-403305.49, 804200.99],

...,

[ 443742.33, 1651248.81],

[-343684.48, 863822. ],

[-153629.93, 1053876.55]])

The output is a NumPy array with a row for each test instance, and where the two columns specify the lower and upper bound of each prediction interval.

We may request that the intervals are cut to exclude impossible values, in this case below 0, and if we also rely on the default confidence level (0.95), the output intervals will be a bit tighter:

rf.predict_int(X_test, y_min=0)

array([[2302049.84, 2783188.76],

[ 588518.88, 1069657.8 ],

[ 0. , 441017.21],

...,

[ 806926.11, 1288065.03],

[ 19499.3 , 500638.22],

[ 209553.85, 690692.77]])

The above intervals are not normalized, i.e., they are all of the same size (at least before they are cut). We could make them more informative through normalization using difficulty estimates; objects considered more difficult will be assigned wider intervals.

We will use a DifficultyEstimator from the crepes.extras module

for this purpose. Here we estimate the difficulty by the standard

deviation of the target of the k (default k=25) nearest neighbors in

the proper training set to each object in the calibration set. A small

value (beta) is added to the estimates, which may be given through an

argument to the function; below we just use the default, i.e.,

beta=0.01.

We first fit the difficulty estimator and then calibrate the conformal regressor, using the calibration objects and labels together the difficulty estimator:

from crepes.extras import DifficultyEstimator

de = DifficultyEstimator()

de.fit(X_prop_train, y=y_prop_train)

rf.calibrate(X_cal, y_cal, de=de)

To obtain prediction intervals, we just have to provide test objects

to the predict_int method, as the difficulty estimates will be

computed by the incorporated difficulty estimator:

rf.predict_int(X_test, y_min=0)

array([[1769594.36212355, 3315644.23787645],

[ 693827.99796647, 964348.68203353],

[ 124886.97469338, 276008.52530662],

...,

[ 661373.45043166, 1433617.68956833],

[ 178769.2939384 , 341368.2260616 ],

[ 222837.12801117, 677409.49198883]])

Depending on the employed difficulty estimator, the normalized intervals may sometimes be unreasonably large, in the sense that they may be several times larger than any previously observed error. Moreover, if the difficulty estimator is uninformative, e.g., completely random, the varying interval sizes may give a false impression of that we can expect lower prediction errors for instances with tighter intervals. Ideally, a difficulty estimator providing little or no information on the expected error should instead lead to more uniformly distributed interval sizes.

A Mondrian conformal regressor can be used to address these problems,

by dividing the object space into non-overlapping so-called Mondrian

categories, and forming a (standard) conformal regressor for each

category. We may form a Mondrian conformal regressor by providing a

function or a MondrianCategorizer (defined in crepes.extras) as an

additional argument, named mc, for the calibrate method.

Here we employ a MondrianCategorizer; it may be fitted in several

different ways, and below we show how to form categories by binning of

the difficulty estimates into 20 bins, using the difficulty estimator

fitted above.

from crepes.extras import MondrianCategorizer

mc_diff = MondrianCategorizer()

mc_diff.fit(X_cal, de=de, no_bins=20)

rf.calibrate(X_cal, y_cal, mc=mc_diff)

When making predictions, the test objects will be assigned to Mondrian categories

according to the incorporated MondrianCategorizer (or labeling function):

rf.predict_int(X_test, y_min=0)

array([[1152528.9 , 3932709.7 ],

[ 692366.75, 965809.93],

[ 124254.81, 276640.69],

...,

[ 622939.57, 1472051.57],

[ 155346.82, 364790.7 ],

[ 239474.31, 660772.31]])

Similarly to semi-online conformal classifiers, we may enable online calibration

also for conformal regressors; this is again done by setting online=True when

calling any of the applicable methods, while also providing the true labels, e.g.,

rf.predict_p(X_test, y_test, online=True)

array([0.09369225, 0.52548032, 0.49992477, ..., 0.72979714, 0.87495964,

0.58352253])

We can easily switch from conformal regressors to conformal predictive systems. The latter produce cumulative distribution functions (conformal predictive distributions). From these we can generate prediction intervals, but we can also obtain percentiles, calibrated point predictions, as well as p-values for given target values. Let us see how we can go ahead to do that.

Well, there is only one thing above that changes: just provide

cps=True to the calibrate method.

We can, for example, form normalized Mondrian conformal predictive

systems, by providing both a Mondrian categorizer and difficulty estimator

to the calibrate method. Here we will consider Mondrian categories formed

from binning the point predictions:

mc_pred = MondrianCategorizer()

mc_pred.fit(X_cal, f=rf.predict, no_bins=5)

rf.calibrate(X_cal, y_cal, de=de, mc=mc_pred, cps=True)

We can now make predictions with the conformal predictive system,

through several different methods, e.g., predict_percentiles:

rf.predict_percentiles(X_test, higher_percentiles=[90, 95, 99])

array([[3120432.14791764, 3403976.16608241, 3952384.13595105],

[ 930191.36994287, 979804.59585495, 1075762.49571536],

[ 236278.82580469, 253387.66592079, 329933.49293406],

...,

[1336110.21956702, 1477739.04927264, 1751666.10820498],

[ 298621.13482031, 317029.35735016, 399388.68783836],

[ 564574.75363948, 615226.06727944, 762212.9912238 ]])

Similarly to semi-online conformal classifiers and regressors, we can enable online calibration also for conformal predictive systems; here we generate prediction intervals at the default (95%) confidence level:

rf.predict_int(X_test, y_test, y_min=0, online=True)

array([[1719676.80439219, 3707173.76806116],

[ 684289.27240227, 1032856.71531186],

[ 127189.61835749, 274385.59426486],

...,

[ 630347.70469164, 1594876.58130005],

[ 167399.51044545, 337513.60197203],

[ 232815.51352497, 641580.14787679]])

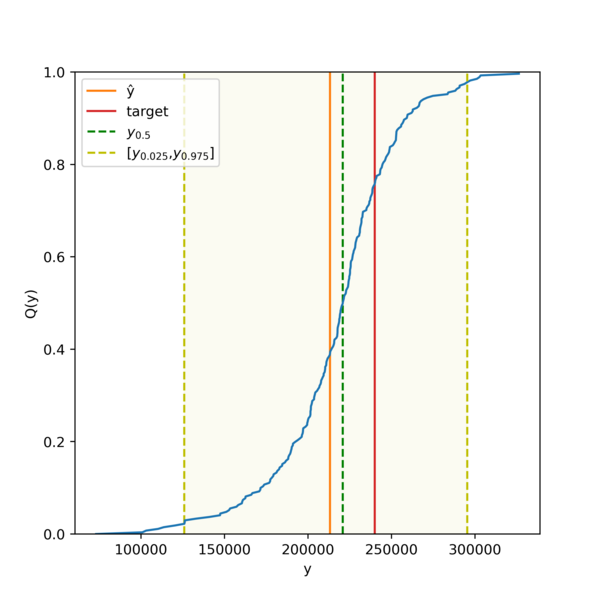

We may also obtain the full conformal predictive distribution for each test instance, as defined by the threshold values:

rf.predict_cpds(X_test)

For a Mondrian conformal predictive system (or any semi-online conformal predictive system), the output is a vector containing one CPD per test instance, while for a standard or normalized conformal predictive system (for which online calibration is not enabled), the output is a 2-dimensional array.

The resulting vector of vectors is not displayed here, but we instead provide a plot for the CPD of a random test instance:

We may also test the exchangeability assumption using conformal test martingales. Assume that we have obtained p-values using a semi-online conformal predictor, e.g.,

p_values = rf.predict_p(X_test, y_test, online=True)

We can now test if the p-values are distributed independently and uniformly over [0, 1] using any of the

available conformal test martingale algorithms in crepes.martingales. If the exchangeability assumption

holds then the probability of observing a martingale value exceeding c is less than or equal to 1/c.

This means that probability of incorrectly rejecting the assumption is bounded by 1/c. We here show

how to obtain martingale values for the above p-values using Simple Jumper:

from crepes.martingales import SimpleJumper

martingale_values = SimpleJumper().apply(p_values)

We may also ask for the lowest index for which the martingale value exceeds a specified threshold:

SimpleJumper().apply(np.sort(p_values), c=100)

Since the p-values are sorted in the above example, the conformal test martingale will detect a violation of the exchangeability assumption early on and return a low index. If instead the original (unsorted) p-values are provided, it is very likely that the conformal test martingale will not detect any data drift and will just return the length of the p-value vector.

Examples

For additional examples of how to use the package and module, see the documentation. Examples on how to wrap learners to obtain conformal predictors are given in this Jupyter notebook , while this Jupyter notebook shows how to obtain conformal predictors that are decoupled from the learners. For examples on conformal test martingales, you may consult this Jupyter notebook.

You may also take a look at some tutorial slides and the accompanying Jupyter notebook.

Citing crepes

You are welcome to cite the following paper:

Boström, H. 2024. Conformal Prediction in Python with crepes. Proceedings of the 13th Symposium on Conformal and Probabilistic Prediction with Applications, PMLR 230:236-249 Link

Bibtex entry:

@inproceedings{bostrom2024,

title={Conformal Prediction in Python with crepes},

author={Bostr{\"o}m, Henrik},

booktitle={Proc. of the 13th Symposium on Conformal and Probabilistic Prediction with Applications},

pages={236--249},

year={2024},

organization={PMLR}

}

An early version of the package was described in:

Boström, H., 2022. crepes: a Python Package for Generating Conformal Regressors and Predictive Systems. Proceedings of the 11th Symposium on Conformal and Probabilistic Prediction with Applications, PMLR 179:24-41 Link

Bibtex entry:

@inproceedings{bostrom2022,

title={crepes: a Python Package for Generating Conformal Regressors and Predictive Systems},

author={Bostr{\"o}m, Henrik},

booktitle={Proc. of the 11th Symposium on Conformal and Probabilistic Prediction with Applications},

pages={24--41},

year={2022},

organization={PMLR}

}

References

[1] Vovk, V., Gammerman, A. and Shafer, G., 2022. Algorithmic learning in a random world. 2nd edition. Springer Link

[2] Papadopoulos, H., Proedrou, K., Vovk, V. and Gammerman, A., 2002. Inductive confidence machines for regression. European Conference on Machine Learning, pp. 345-356. Link

[3] Johansson, U., Boström, H., Löfström, T. and Linusson, H., 2014. Regression conformal prediction with random forests. Machine learning, 97(1-2), pp. 155-176. Link

[4] Boström, H., Linusson, H., Löfström, T. and Johansson, U., 2017. Accelerating difficulty estimation for conformal regression forests. Annals of Mathematics and Artificial Intelligence, 81(1-2), pp.125-144. Link

[5] Boström, H. and Johansson, U., 2020. Mondrian conformal regressors. In Conformal and Probabilistic Prediction and Applications. PMLR, 128, pp. 114-133. Link

[6] Vovk, V., Petej, I., Nouretdinov, I., Manokhin, V. and Gammerman, A., 2020. Computationally efficient versions of conformal predictive distributions. Neurocomputing, 397, pp.292-308. Link

[7] Boström, H., Johansson, U. and Löfström, T., 2021. Mondrian conformal predictive distributions. In Conformal and Probabilistic Prediction and Applications. PMLR, 152, pp. 24-38. Link

[8] Vovk, V., 2022. Universal predictive systems. Pattern Recognition. 126: pp. 108536 Link

Author: Henrik Boström (bostromh@kth.se) Copyright 2026 Henrik Boström License: BSD 3 clause

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file crepes-0.9.1.tar.gz.

File metadata

- Download URL: crepes-0.9.1.tar.gz

- Upload date:

- Size: 51.1 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.12.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

14255bfeef3d3cb76fefa78f9cef1d05ecf106dfae6f2bf76096eb7f5524c099

|

|

| MD5 |

98ab771ece5f62b667043485be091647

|

|

| BLAKE2b-256 |

675c926ea5b808fd8cc8b3cdda9c90d08897340d295bf2ece2d6fa8b1c3b5012

|

File details

Details for the file crepes-0.9.1-py3-none-any.whl.

File metadata

- Download URL: crepes-0.9.1-py3-none-any.whl

- Upload date:

- Size: 44.6 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.12.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d1e0c4c212c72883f2be3d3b58242782040c5c40295453f561112d23deb29fd2

|

|

| MD5 |

896647f769e0e0d7809db319bec005b1

|

|

| BLAKE2b-256 |

a7d0f30abace5048356fec034784f20afe1daa84a3d40cddd7812351b2d004a1

|