DQuant is an open-source Python library for automated volatility forecasting of financial time series. It handles all stages of model construction, from raw prices to the final forecast.

Project description

DQuant

Automated Volatility Forecasting for Traders and Analysts

Volatility forecast with DQuant

About the Project

DQuant is an open-source Python library for automated volatility forecasting of financial time series. It handles all stages of model building: from raw prices to ready-made forecasts.

Key Idea

A trader doesn't need to know machine learning to use AI for volatility forecasting.

Features

| Automated feature engineering | Creates dozens of features from raw prices (open, high, low, close, volume) |

| Target variable without look-ahead bias | Correct calculation of realized volatility |

| 3 models to choose from | Gradient Boosting, XGBoost, LightGBM with early stopping |

| Training visualization | Error plot on train/validation to monitor overfitting |

| Save and load | Train once — use forever |

| Flexible customization | Your own features, model parameters, data sources |

| Integration with any data | Yahoo Finance, MetaTrader 5 |

Who is this for

- Algorithmic traders — for model calibration and risk management

- Discretionary traders — for assessing market regime and position sizing

- Quantitative analysts — for rapid prototyping

- Developers — for embedding into trading systems

- Students — as a ready-made benchmark and learning example

Installation

Requirements

- Python 3.7 or higher

- pip

pip install dquant

Verify Installation

import dquant

print(dquant.__version__) # Should output the version

Quick Start

Minimal working example with Bitcoin

import pandas as pd

import yfinance as yf

from dquant.models import VolClustXGB

# 1. Load data

df = yf.download("BTC-USD", start="2020-01-01", interval='1d')

df = pd.DataFrame({

'open': df[('Open', 'BTC-USD')].values,

'high': df[('High', 'BTC-USD')].values,

'low': df[('Low', 'BTC-USD')].values,

'close': df[('Close', 'BTC-USD')].values,

'volume': df[('Volume', 'BTC-USD')].values

}, index=df.index)

# 2. Create model

model = VolClustXGB({}, early_stopping=True)

# 3. Train model

features = [

'TR',

'returns',

'abs_returns',

'gap',

'body',

'shadow',

'close_position',

'roll_atr_14'

]

model.fit(df, feature_list=features, input_bars=70, horizon=20, trees_count=200, show_results=True)

# 4. Make forecast

rez = model.forecast(df.iloc[-70:].copy(), show=True)

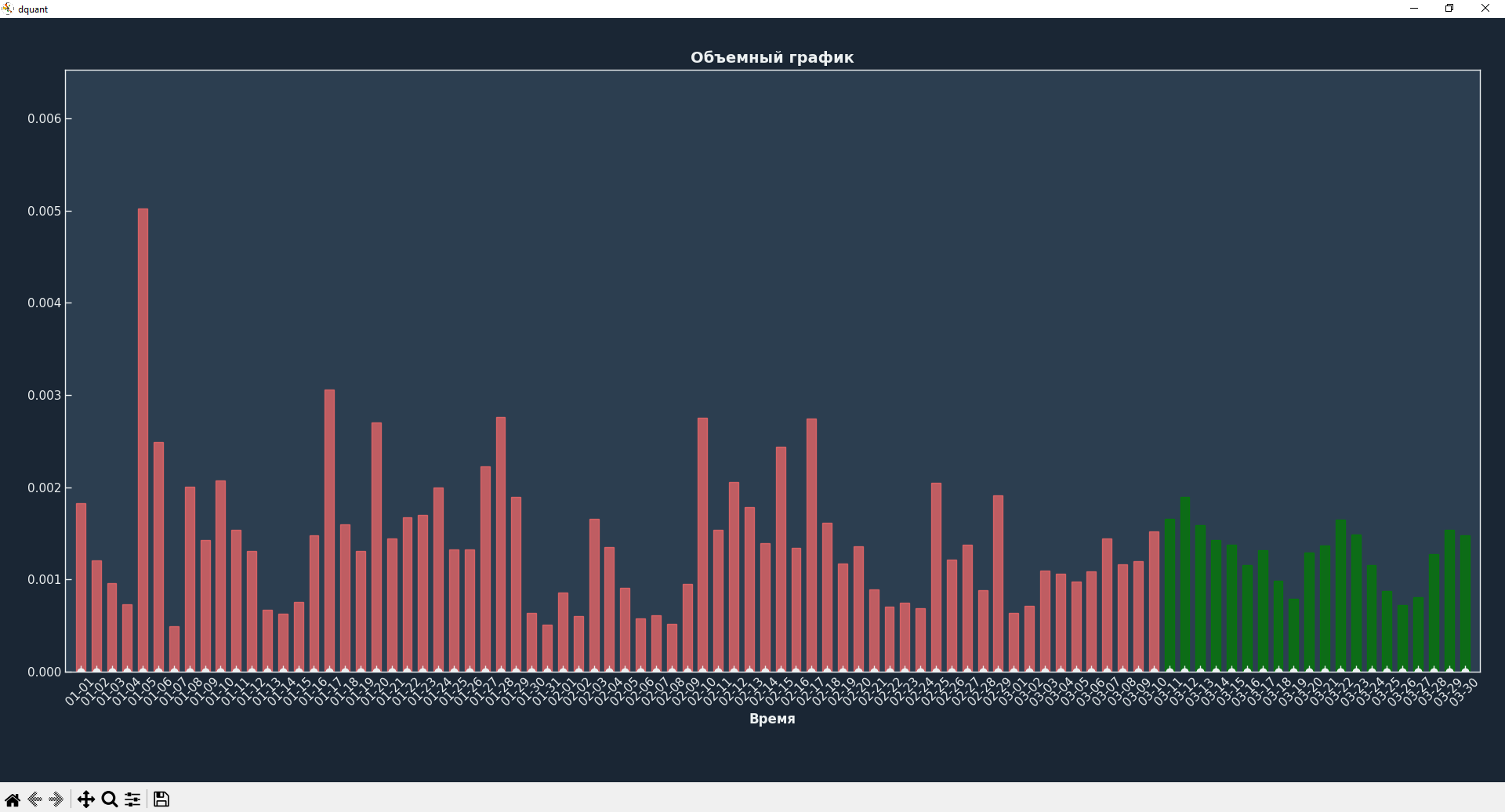

Execution result

[0.0016554 0.0018979 0.0015921 0.0014239 0.0013767 0.0011586 0.0013139

0.0009813 0.0007931 0.0012909 0.0013664 0.0016466 0.0014836 0.0011577

0.0008737 0.0007213 0.0008084 0.0012699 0.0015358 0.0014748]

Red shows volatility for previous candles, green shows future volatility.

Documentation

| Resource | Description |

|---|---|

| Full documentation | All classes, methods, parameters |

Usage Examples

With Yahoo Finance

import pandas as pd

import yfinance as yf

from dquant.models import VolClustXGB

# 1. Load data

df = yf.download("BTC-USD", start="2020-01-01", interval='1d')

df = pd.DataFrame({

'open': df[('Open', 'BTC-USD')].values,

'high': df[('High', 'BTC-USD')].values,

'low': df[('Low', 'BTC-USD')].values,

'close': df[('Close', 'BTC-USD')].values,

'volume': df[('Volume', 'BTC-USD')].values

}, index=df.index)

# 2. Create model

model = VolClustXGB({}, early_stopping=True)

# 3. Train model

features = [

'TR',

'returns',

'abs_returns',

'gap',

'body',

'shadow',

'close_position',

'roll_atr_14'

]

model.fit(df, feature_list=features, input_bars=70, horizon=20, trees_count=200, show_results=True)

# 4. Make forecast

rez = model.forecast(df.iloc[-70:].copy(), show=True)

With MetaTrader 5

import pandas as pd

import MetaTrader5 as mt5

import datetime as dt

from dquant.models import VolClustXGB

symbol = "EURUSD" # symbol to watch

timeframe = mt5.TIMEFRAME_H1 # M1, M5, M15, H1, D1, etc.

days_back = 1000 # how many days of history to load

# Connect to MT5

if not mt5.initialize():

print("Failed to connect to MetaTrader5")

quit()

# Check that symbol is available

if not mt5.symbol_select(symbol, True):

print(f"Symbol {symbol} not found or not enabled")

mt5.shutdown()

quit()

# Calculate dates

to_date = dt.datetime.now() + dt.timedelta(hours=3)

from_date = to_date - dt.timedelta(days=days_back)

# Load bars

rates = mt5.copy_rates_range(symbol, timeframe, from_date, to_date)

mt5.shutdown() # terminal no longer needed

if rates is None or len(rates) == 0:

print("No data!")

quit()

# Convert to DataFrame

df = pd.DataFrame(rates)

df['time'] = pd.to_datetime(df['time'], unit='s')

df.rename(columns={

'tick_volume': 'volume'

}, inplace=True)

# Create model

model = VolClustXGB({}, early_stopping=True)

# Train model

features = [

'TR',

'returns',

'abs_returns',

'gap',

'body',

'shadow',

'close_position',

'roll_atr_14'

]

model.fit(df, feature_list=features, input_bars=70, horizon=20, trees_count=200, show_results=True)

# Make forecast

rez = model.forecast(df.iloc[-70:].copy(), show=True)

Creating an indicator for Meta Trader 5

Immediately after training the model, you can export it to a working mql5 indicator. Just one more line of code is needed:

model.save('indicator_name', type_to_save='mql5')

Done! Now you can use your trained models in Meta Trader 5.

How to Contribute

We welcome any contribution to the project! Here are a few ways to help:

Report a bug

Found a bug? Create an Issue with a detailed description:

- What you did

- What you expected

- What actually happened

- Code to reproduce (if possible)

Suggest an idea

Have an idea for improvement? Write to Telegram or create an Issue with the enhancement label.

License

The project is distributed under the MIT license. See the LICENSE file for details.

Project Support

If dquant has helped you in your work or studies:

- Star the project on GitHub ⭐ — it's very motivating!

- Tell your colleagues about the library

- Write to me about your experience using it

Contacts

Author: Denis Makarov

- Telegram: @Denchik_ai

- GitHub: @artrdon

- Project website: dquant.space

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file dquant-1.1.3.tar.gz.

File metadata

- Download URL: dquant-1.1.3.tar.gz

- Upload date:

- Size: 21.9 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.11.0

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d2ca31123ad8fd3fd225e5f94422f1d5c1a7c9f15038671f92c4fb74fa205f62

|

|

| MD5 |

1fafa447b06e66fa620efa2be6f41cb4

|

|

| BLAKE2b-256 |

1c2b625d33d227fdf32a1647145b476e16c15013b6adb6c0f7a770e3bf1499a4

|

File details

Details for the file dquant-1.1.3-py3-none-any.whl.

File metadata

- Download URL: dquant-1.1.3-py3-none-any.whl

- Upload date:

- Size: 20.1 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.11.0

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

54acae8cd1c6c98c9329349b62ebfbc2e950db6ba4bf6e147bd6c95ae7b6f64d

|

|

| MD5 |

33676ddffca90367f35a9266e3b58591

|

|

| BLAKE2b-256 |

fbd381de911371470a3dca5d396086c9907102a80902fa9253a75adc8e74d442

|