empyrical computes performance and risk statistics commonly used in quantitative finance

Project description

Common financial return and risk metrics in Python.

Installation

empyrical requires Python 3.10+. You can install it using pip:

pip install empyrical-reloaded

or conda from the conda-forge channel

conda install empyrical-reloaded -c conda-forge

empyrical requires and installs the following packages while executing the above commands:

- numpy>=1.23.5

- pandas>=1.3.0

- scipy>=0.15.1

Note that Numpy>=2.0 requires pandas>=2.2.2. If you are using an older version of pandas, you may need to upgrade accordingly, otherwise you may encounter compatibility issues.

Optional dependencies include yfinance to download price data from Yahoo! Finance and pandas-datareader to access Fama-French risk factors and FRED treasury yields.

Note that

pandas-datareaderis not compatible with Python>=3.12.

To install the optional dependencies, use:

pip install empyrical-reloaded[yfinance]

or

pip install empyrical-reloaded[datreader]

or

pip install empyrical-reloaded[yfinance,datreader]

Usage

Simple Statistics

Empyrical computes basic metrics from returns and volatility to alpha and beta, Value at Risk, and Shorpe or Sortino ratios.

import numpy as np

from empyrical import max_drawdown, alpha_beta

returns = np.array([.01, .02, .03, -.4, -.06, -.02])

benchmark_returns = np.array([.02, .02, .03, -.35, -.05, -.01])

# calculate the max drawdown

max_drawdown(returns)

# calculate alpha and beta

alpha, beta = alpha_beta(returns, benchmark_returns)

Rolling Measures

Empyrical also aggregates return and risk metrics for rolling windows:

import numpy as np

from empyrical import roll_max_drawdown

returns = np.array([.01, .02, .03, -.4, -.06, -.02])

# calculate the rolling max drawdown

roll_max_drawdown(returns, window=3)

Pandas Support

Empyrical also works with both NumPy arrays and Pandas data structures:

import pandas as pd

from empyrical import roll_up_capture, capture

returns = pd.Series([.01, .02, .03, -.4, -.06, -.02])

factor_returns = pd.Series([.02, .01, .03, -.01, -.02, .02])

# calculate a capture ratio

capture(returns, factor_returns)

-0.147387712263491

Fama-French Risk Factors

Empyrical downloads Fama-French risk factors from 1970 onward:

Note: requires optional dependency

pandas-datareader- see installation instructions above.gst

import pandas as pd

import empyrical as emp

risk_factors = emp.utils.get_fama_french()

pd.concat([risk_factors.head(), risk_factors.tail()])

Mkt - RF

SMB

HML

RF

Mom

Date

1970 - 01 - 02

00: 00:00 + 00: 00

0.0118

0.0129

0.0101

0.00029 - 0.0340

1970 - 01 - 05

00: 00:00 + 00: 00

0.0059

0.0067

0.0072

0.00029 - 0.0153

1970 - 01 - 06

00: 00:00 + 00: 00 - 0.0074

0.0010

0.0021

0.00029

0.0038

1970 - 01 - 07

00: 00:00 + 00: 00 - 0.0015

0.0040 - 0.0033

0.00029

0.0011

1970 - 01 - 0

8

00: 00:00 + 00: 00

0.0004

0.0018 - 0.0017

0.00029

0.0033

2024 - 03 - 22

00: 00:00 + 00: 00 - 0.0023 - 0.0087 - 0.0053

0.00021

0.0043

2024 - 03 - 25

00: 00:00 + 00: 00 - 0.0026 - 0.0024

0.0088

0.00021 - 0.0034

2024 - 03 - 26

00: 00:00 + 00: 00 - 0.0026

0.0009 - 0.0013

0.00021

0.0009

2024 - 03 - 27

00: 00:00 + 00: 00

0.0088

0.0104

0.0091

0.00021 - 0.0134

2024 - 03 - 28

00: 00:00 + 00: 00

0.0010

0.0029

0.0048

0.00021 - 0.0044

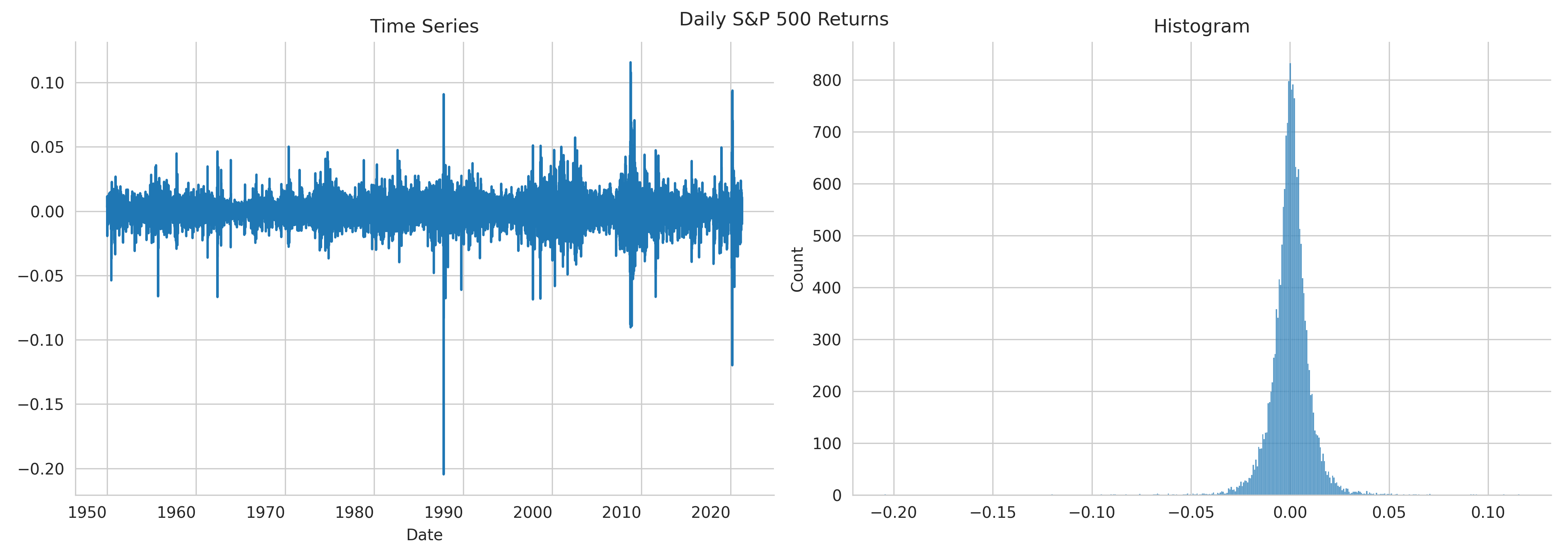

Asset Prices and Benchmark Returns

Empyrical use yfinance to download price data from Yahoo! Finance. To obtain the S&P returns since 1950, use:

Note: requires optional dependency

yfinance- see installation instructions above.

import empyrical as emp

symbol = '^GSPC'

returns = emp.utils.get_symbol_returns_from_yahoo(symbol,

start='1950-01-01')

import seaborn as sns # requires separate installation

import matplotlib.pyplot as plt # requires separate installation

fig, axes = plt.subplots(ncols=2, figsize=(14, 5))

with sns.axes_style('whitegrid'):

returns.plot(ax=axes[0], rot=0, title='Time Series', legend=False)

sns.histplot(returns, ax=axes[1], legend=False)

axes[1].set_title('Histogram')

sns.despine()

plt.tight_layout()

plt.suptitle('Daily S&P 500 Returns')

Documentation

See the documentation for details on the API.

Support

Please open an issue for support.

Contributing

Please contribute using Github Flow. Create a branch, add commits, and open a pull request.

Testing

- install requirements

- "pytest>=6.2.0",

pytest tests

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file empyrical_reloaded-0.5.12.tar.gz.

File metadata

- Download URL: empyrical_reloaded-0.5.12.tar.gz

- Upload date:

- Size: 84.3 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.12.9

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

e01f0bbf24f0aaab2767c85a7dee8f05a59d25355cf50c3371efda056613e323

|

|

| MD5 |

250231b3edd0dacce85eba636e548a34

|

|

| BLAKE2b-256 |

97432dd510760e12fb9a07d2ab4dcf67f263e6eb103c73285d040005fe3d5da9

|

File details

Details for the file empyrical_reloaded-0.5.12-py3-none-any.whl.

File metadata

- Download URL: empyrical_reloaded-0.5.12-py3-none-any.whl

- Upload date:

- Size: 33.0 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.12.9

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

1bd8b53810c760ae5a12a03f2cefc6af0e905f854b71e7d99074b673abdd4fd6

|

|

| MD5 |

4329b69a33ed0e1f8c5c94b2f3116981

|

|

| BLAKE2b-256 |

695423d8f6d36c66575b8d31e354c8bba2c857f9ca41e4b76388c6ca53938fd8

|