A personal automated trading system

Project description

Minitrade

Minitrade is a personal trading system that supports both strategy backtesting and automated order execution.

It integrates with Backtesting.py under the hood, and:

- Is fully compatible with Backtesting.py strategies with minor adaptions.

- Supports multi-asset portfolio and rebalancing strategies.

Or it can be used as a full trading system that:

- Automatically executes trading strategies and submits orders.

- Manages strategy execution via web console.

- Runs on very low cost machines.

Limitations as a backtesting framework:

- Multi-asset strategy only supports long positions and market order.

Limitations (for now) as a trading system:

- Tested only on Linux

- Support only daily bar and market-on-open order

- Support only long positions

- Support only Interactive Brokers

On the other hand, Minitrade is intended to be easily hackable to fit individual's needs.

Installation

Minitrade requires python=3.10.*

If only used as a backtesting framework:

$ pip install minitrade

If used as a trading system, continue with the following:

$ minitrade init

For a detailed setup guide on Ubuntu, check out Installation.

Backtesting

Minitrade uses Backtesting.py as the core library for backtesting and adds the capability to implement multi-asset strategies.

Single asset strattegy

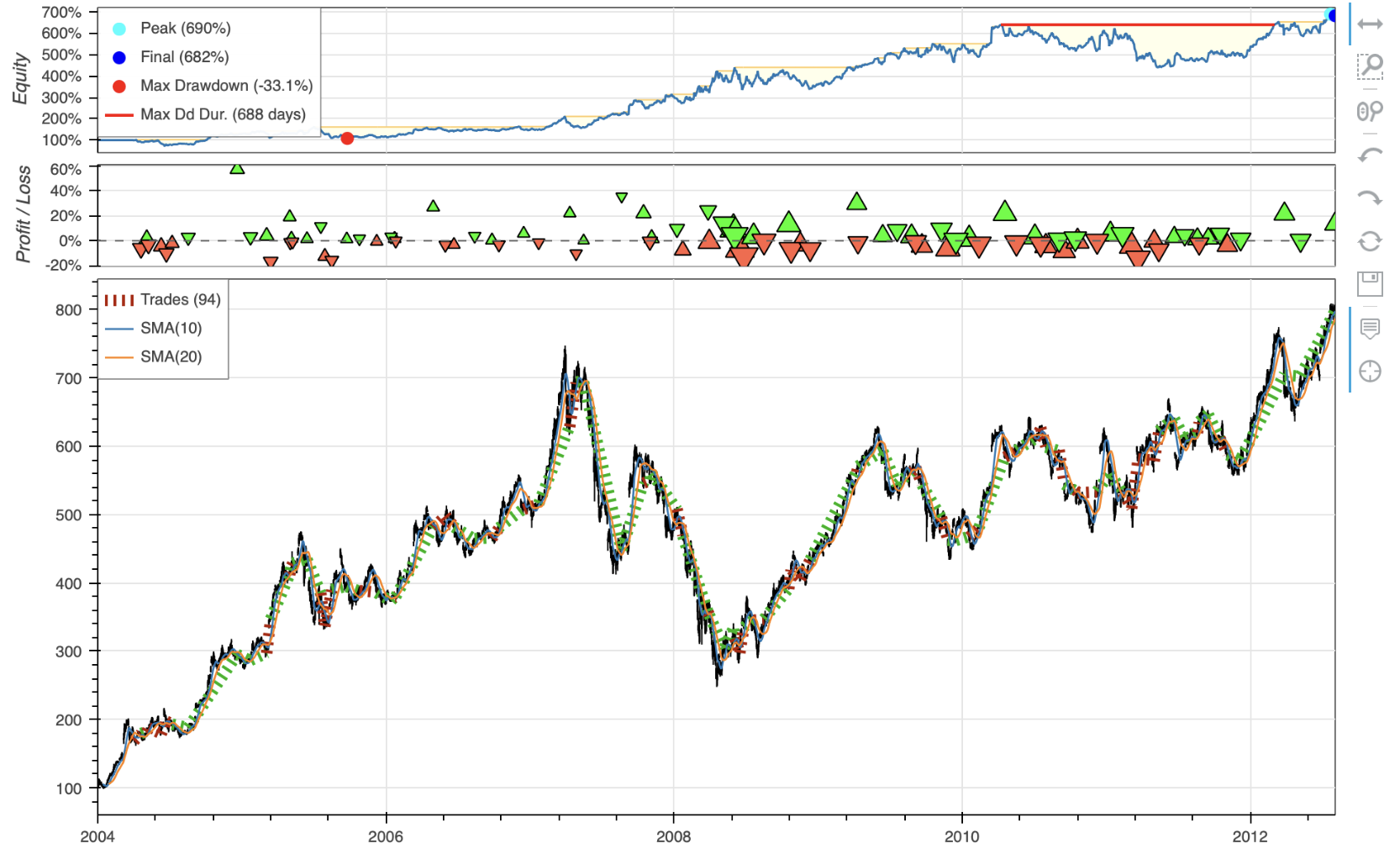

For single asset strategies, those written for Backtesting.py can be easily adapted to work with Minitrade. The following illustrates what changes are necessary:

from minitrade.backtest import Backtest, Strategy

from minitrade.backtest.core.lib import crossover

from minitrade.backtest.core.test import SMA, GOOG

class SmaCross(Strategy):

def init(self):

price = self.data.Close.df

self.ma1 = self.I(SMA, price, 10, overlay=True)

self.ma2 = self.I(SMA, price, 20, overlay=True)

def next(self):

if crossover(self.ma1, self.ma2):

self.position().close()

self.buy()

elif crossover(self.ma2, self.ma1):

self.position().close()

self.sell()

bt = Backtest(GOOG, SmaCross, commission=.002)

stats = bt.run()

bt.plot()

- Change to import from minitrade modules. Generally

backtestingbecomesminitrade.backtest.core. - Minitrade expects

Volumedata to be always avaiable.Strategy.datashould be consisted of OHLCV. - Minitrade doesn't try to guess where to plot the indicators. So if you want to overlay the indicators on the main chart, set

overlay=Trueexplicitly. Strategy.positionis no longer a property but a function. Any occurrence ofself.positionshould be changed toself.position().

That's it. Check out compatibility for more details.

Also note that some original utility functions and strategy classes only make sense for single asset strategy. Don't use those in multi-asset strategies.

Multi-asset strategy

Minitrade extends Backtesting.py to support backtesting of multi-asset strategies.

Multi-asset strategies take a 2-level DataFrame as data input. For example, for a strategy class that intends to invest in AAPL and GOOG as a portfolio, the self.data should look like:

$ print(self.data)

AAPL GOOG

Open High Low Close Volume Open High Low Close Volume

Date

2018-01-02 00:00:00-05:00 40.39 40.90 40.18 40.89 102223600 52.42 53.35 52.26 53.25 24752000

2018-01-03 00:00:00-05:00 40.95 41.43 40.82 40.88 118071600 53.22 54.31 53.16 54.12 28604000

2018-01-04 00:00:00-05:00 40.95 41.18 40.85 41.07 89738400 54.40 54.68 54.20 54.32 20092000

2018-01-05 00:00:00-05:00 41.17 41.63 41.08 41.54 94640000 54.70 55.21 54.60 55.11 25582000

2018-01-08 00:00:00-05:00 41.38 41.68 41.28 41.38 82271200 55.11 55.56 55.08 55.35 20952000

Like in Backtesting.py, self.data is _Data type that supports progressively revealing of data, and the raw DataFrame can be accessed by self.data.df.

To facilitate indicator calculation, Minitrade has built-in integration with pandas_ta a TA library. pandas_ta is accessible using .ta property of any DataFrame. Check out here for usage. .ta is also enhanced to support 2-level DataFrames.

For example,

$ print(self.data.df.ta.sma(3))

AAPL GOOG

Date

2018-01-02 00:00:00-05:00 NaN NaN

2018-01-03 00:00:00-05:00 NaN NaN

2018-01-04 00:00:00-05:00 40.946616 53.898000

2018-01-05 00:00:00-05:00 41.163408 54.518500

2018-01-08 00:00:00-05:00 41.331144 54.926167

Even simpler, self.data.ta.sma(3) works the same on self.data.

self.I() can take both DataFrame/Series and functions as arguments to define an indicator. If DataFrame/Series is given as input, it's expected to have exactly the same index as self.data. For example,

self.sma = self.I(self.data.df.ta.sma(3), name='SMA_3')

Within Strategy.next(), indicators are returned as type _Array, essentially numpy.ndarray, same as in Backtesting.py. The .df accessor returns either DataFrame or Series of the corresponding value. It's the caller's responsibility to know which exact type should be returned. .s accessor is also available but only as a syntax suger to return a Series. If the actual data is a DataFrame, .s throws a ValueError.

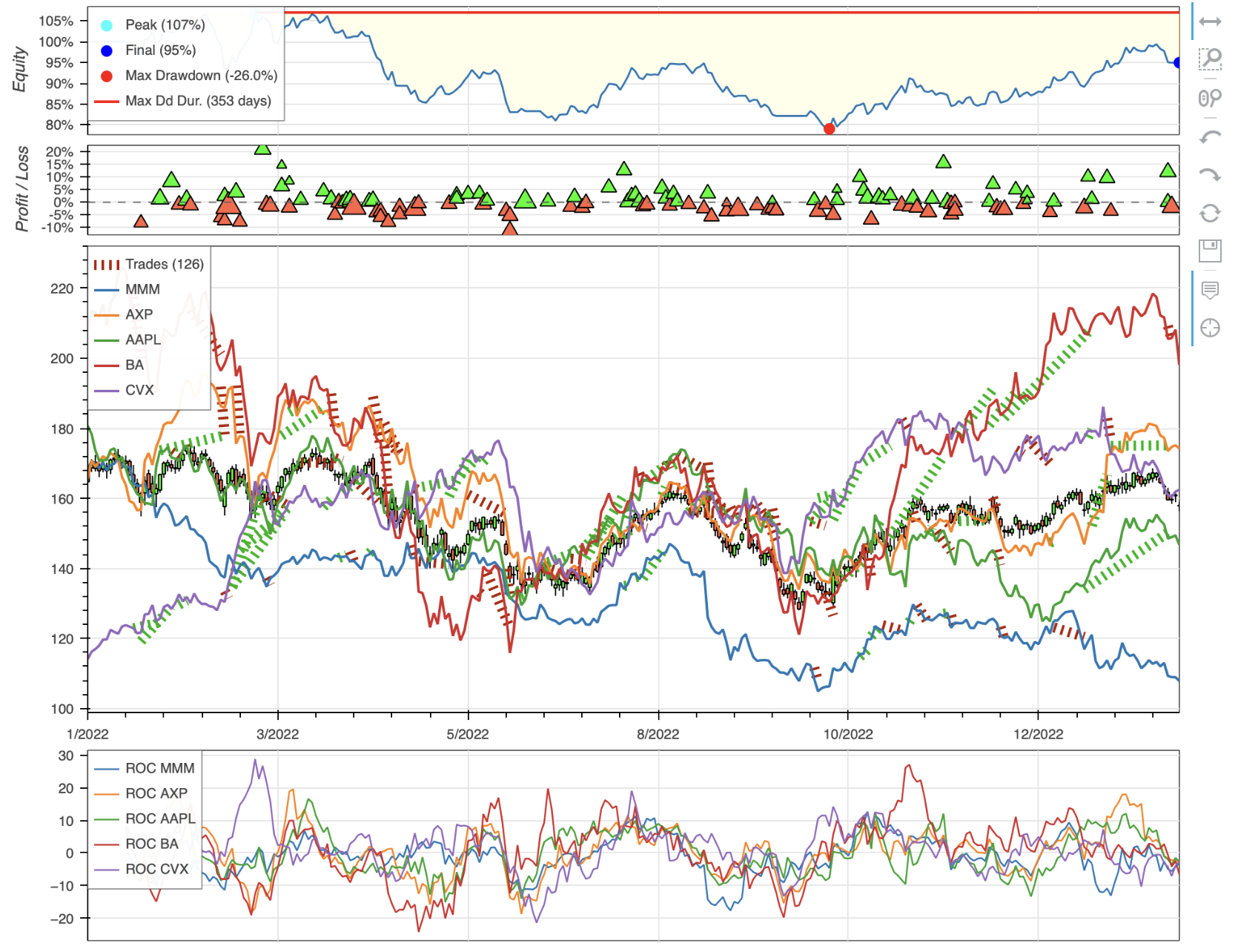

A key addition to support multi-asset strategy is a Strategy.alloc attribute, which combined with Strategy.rebalance() API, allows to specify how cash value should be allocate among the different assets.

Here is an example:

# This strategy evenly allocates cash into the assets

# that have the top 2 highest rate-of-change every day,

# on condition that the ROC is possitive.

class TopPositiveRoc(Strategy):

n = 10

def init(self):

roc = self.data.ta.roc(self.n)

self.roc = self.I(roc, name='ROC')

def next(self):

roc = self.roc.df.iloc[-1]

self.alloc.add(

roc.nlargest(2).index,

roc > 0

).equal_weight()

self.rebalance()

self.alloc keeps track of what assets you want to buy and how much weight you want to assign to each.

At the beginning of each Strategy.next() call, self.alloc starts empty.

Use alloc.add() to add assets to a candidate pool. alloc.add() takes either an index or a boolean Series as input. If it's an index, all asset in the index are added to the pool. If it's a boolean Series, index items having a True value are added to the pool. When multiple conditions are specified in the same call, the conditions are joined by logical AND and the resulted assets are added the the pool. alloc.add() can be called multiple times which means a logical OR relation and add all assets involved to the pool.

Once candidate assets are determined, Call alloc.equal_weight() to assign equal weight in term of value to each selected asset.

And finally, call Strategy.rebalance(), which will look at the current equity value, calculate the target value for each asset, calculate how many shares to buy or sell based on the current long/short positions, and generate orders that will bring the portfolio to the target allocation.

Run the above strategy on some DJIA components:

Trading

Trading a strategy manually is demanding. Running backtest, submitting orders, sticking to the plan despite ups and downs, and tracking performance takes not only effort, but also discipline. Minitrade makes it easy by automating the entire process.

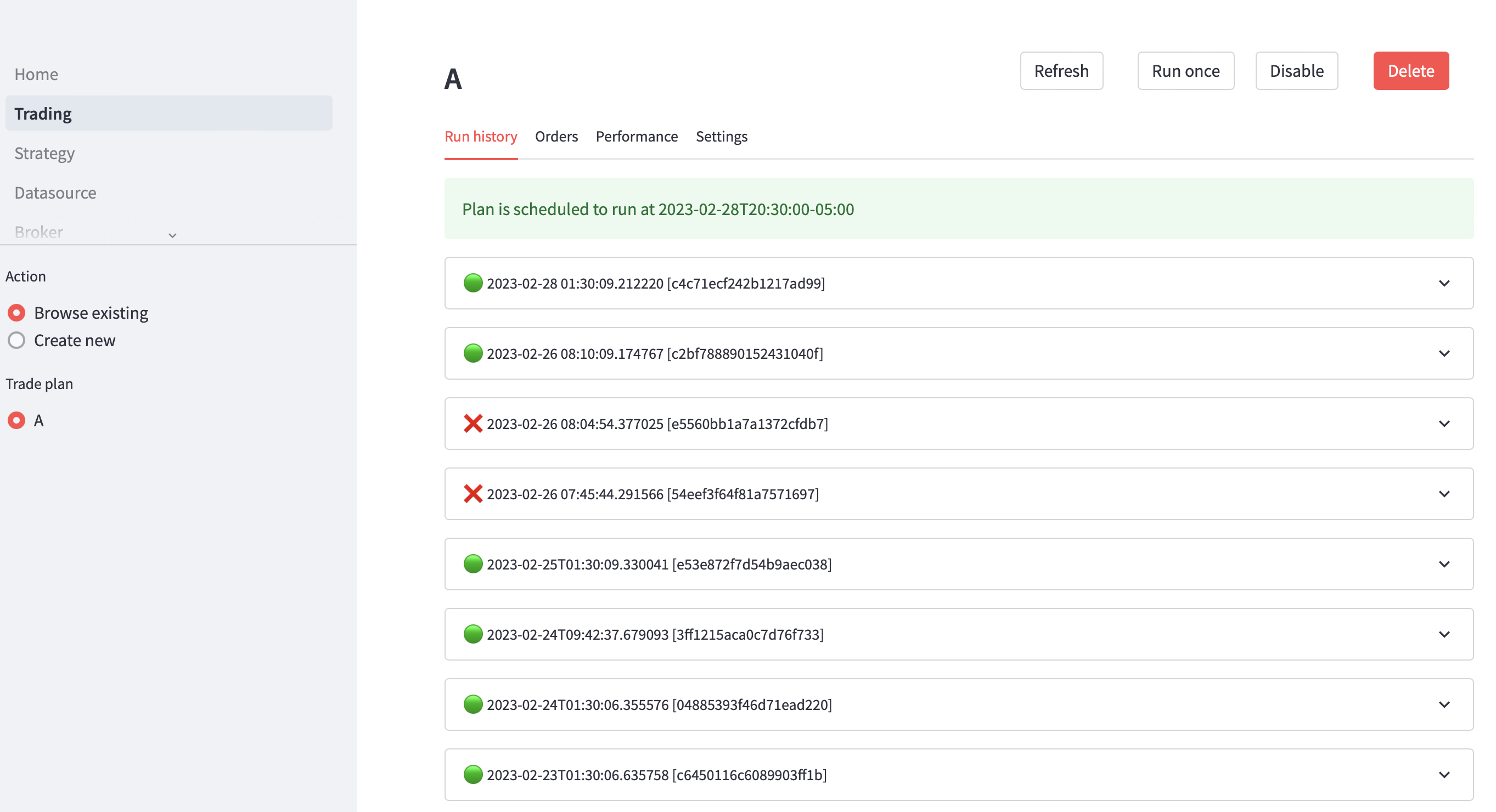

Minitrade's trading system consists of 3 modules:

- A scheduler, that runs strategies periodically and triggers order submission.

- A broker gateway, that interfaces with the broker system (IB in this case) and handles the communication.

- A web UI, that allows managing trading plans and monitoring the executions.

Launch

To start trading, run the following:

# start scheduler

minitrade scheduler start

# start ibgateway

minitrade ib start

# start web UI

minitrade web

Use nohup or other tools to keep the processes running after quiting the shell.

The web UI can be accessed at: http://127.0.0.1:8501

Configure

Configuring the system takes a few steps:

-

Data source

Test the data source and make sure it works. Currently only Yahoo is supported. If a proxy is needed to visit Yahoo, configure it in the UI.

-

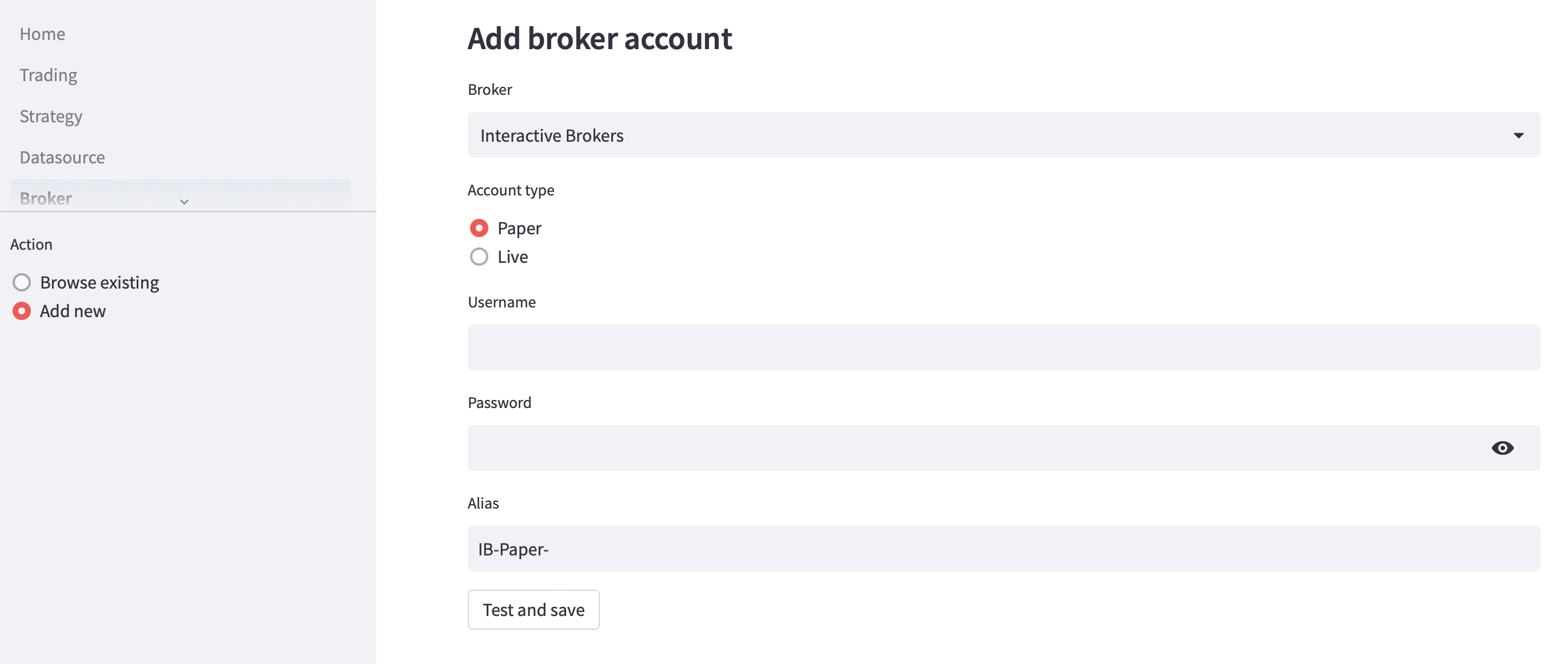

Broker

Put in the username and password, and give the account an alias. Note the Account type selected is only a hint to help remember. Whether it's paper or live depends on the account itself, rather than on what's chosen here.

A test connection to the broker is made before the account is saved. It verifies if the credentials are correct and a connection can be established successfully. For IB, if two-factor authentication is enabled, a notification will be sent to the mobile phone. Confirming on the mobile to finish login.

The credentials are saved in a local database. Be sure to secure the access to the server.

-

Telegram bot (required)

Configure a Telegram bot to receive notifications and to control trader execution. Follow the instructions to create a bot, and take note of the token and chat ID. Configure those in web UI. On saving the configuration, a test message will be sent. Setup is successful if the message can be received.

After changing telegram settings, restart all minitrade processes to make the change effective.

-

Email provider (optional)

Configure a Mailjet account to receive email notifcations about backtesting and trading results. A free-tier account should be enough. Configure authorized senders in Mailjet, otherwise sending will fail. Try use different domains for senders and receivers if free email services like Hotmail, Gmail are used, otherwise, e.g., an email sending from a Hotmail address, through 3rd part servers, to the same or another Hotmail address is likely to be treated as spam and not delivered. Sending from Hotmail address to Gmail address or vice versa increases the chance of going through. On saving the configuration, a test email will be sent. Setup is successful if the email can be received.

-

Strategy

Strategies are just Python files containing a strategy class implementation inherited from the

Strategyclass. The files can be uploaded via the UI and be made available for defining a trade plan. If a strategy class can't be found, it will show an error. If multiple strategy classes exist in a file, the one to be run should be decorated with@entry_strategy. To update a strategy, upload a differnt file with the same filename. -

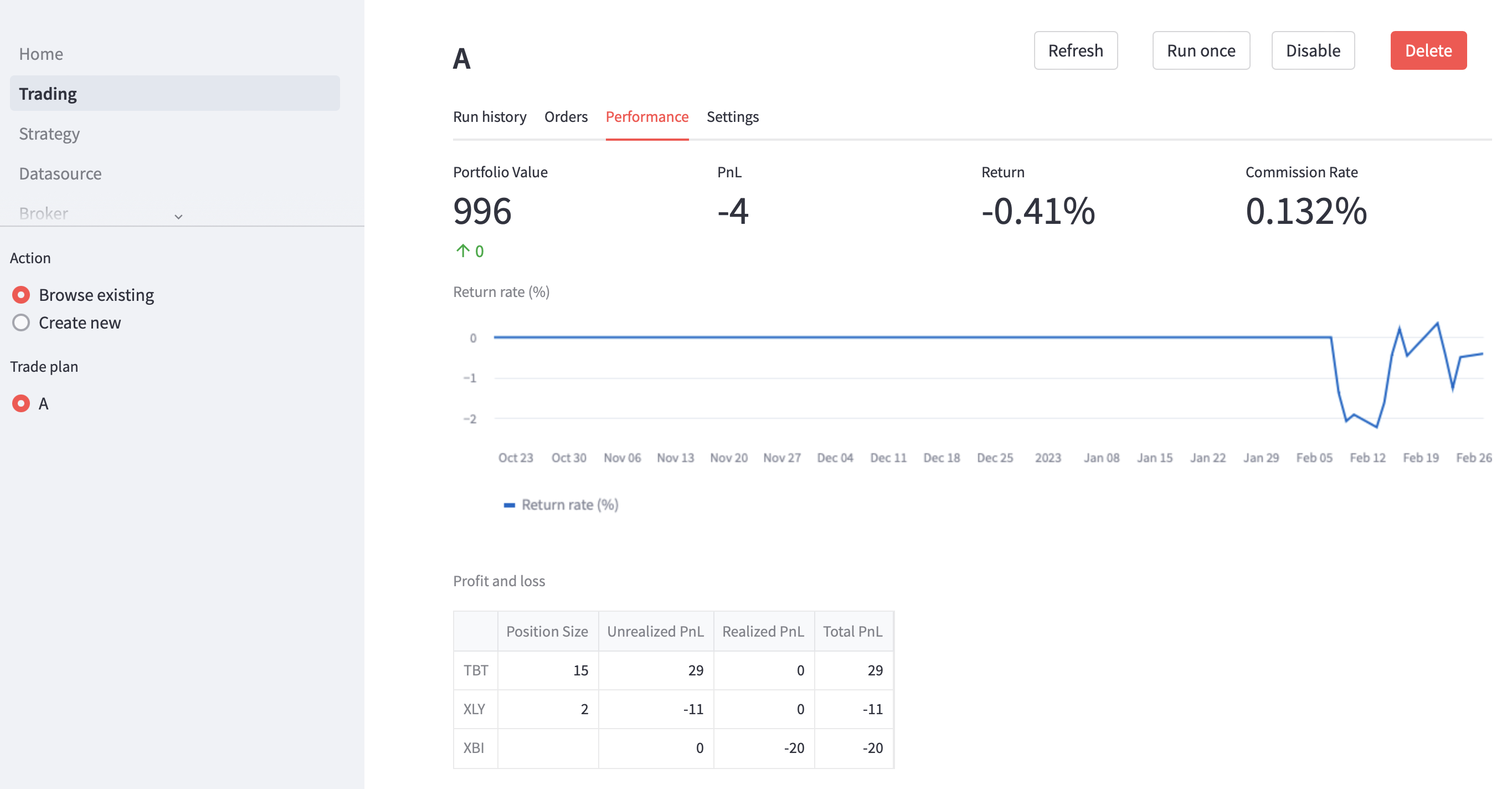

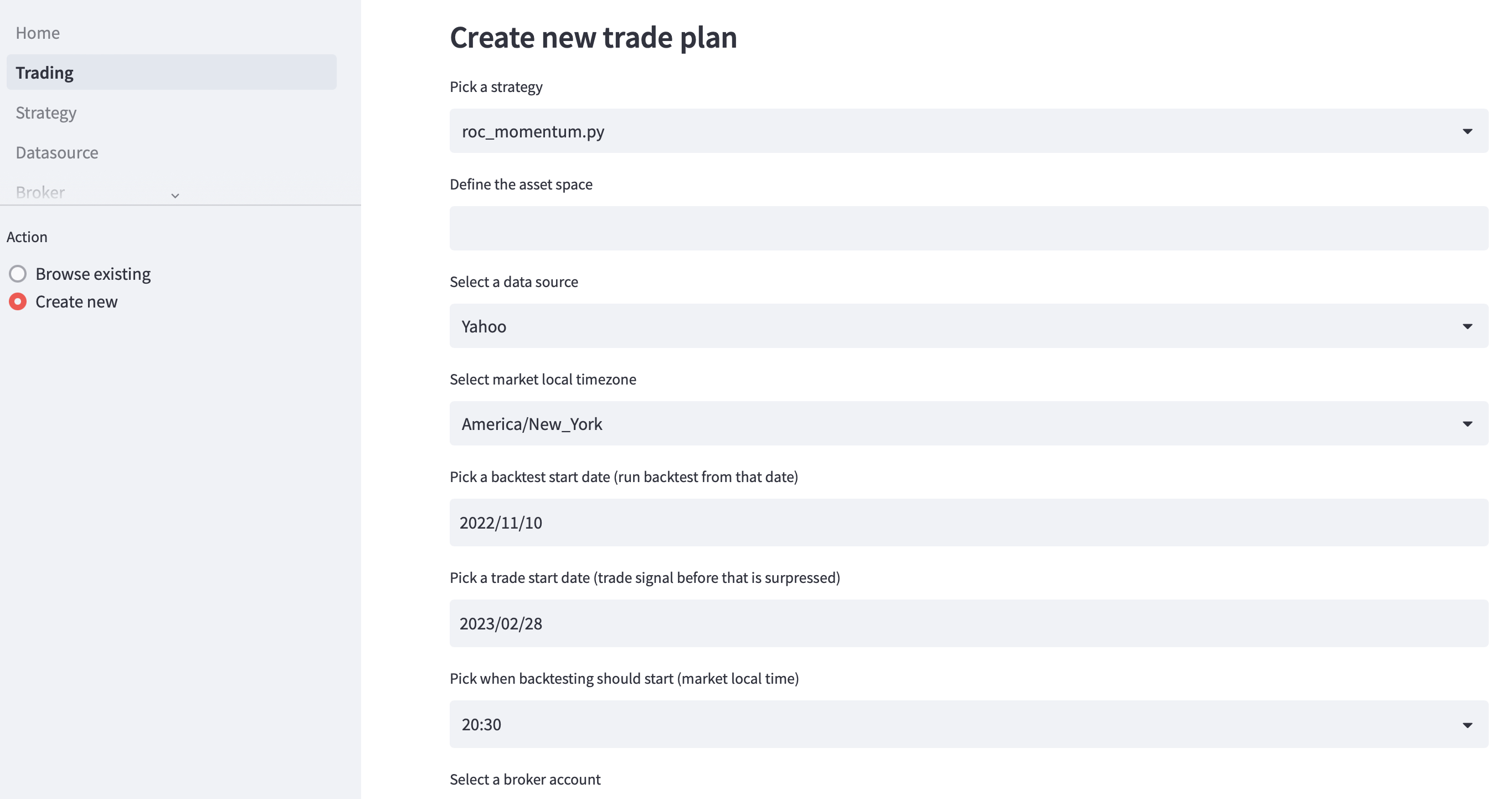

Trade plan

A trade plan provides all necessary information to trade a strategy, including:

- which strategy to run

- the universe of assets as a list of tickers

- which data source to get price data from

- which timezone are the assets traded

- which date should a backtest starts

- which date should a trade order be generated from

- at what time of day should a backtest run

- which broker account should orders be submitted through

- how much initial cash should be invested

The generic tickers need to be resolved to broker specific instrument IDs. Therefore a connection to broker will be made, which may trigger 2FA authentication. Pay attention to 2FA push on mobile phone if necessary.

Once everything is defined, a test backtest dryrun will start. It should finish without error, though it will not generate any actual orders.

If the test run is successful, the trade plan is scheduled to run every Mon-Fri at the specified time. The time should be between market close and next market open and after when EOD market data becomes available from the selected data source.

Backtests can be triggered at any time without duplicate orders or any other side effects.

Backtesting and trading can be enabled or disabled via the UI.

IB gateway

Minitrade uses IB's client portal API to submit orders. The gateway client will be automatically downloaded and configured when minitrade init is run. It handles automatically login via Chrome and Selenium webdriver.

IB automatically disconnects a session after 24 hours or so. Minitrade checks connection status when it needs to interact with IB, i.e. when an order should be submitted or account info is retrieved via web UI. Therefore, Should Minitrade initiates a connection, if dead, automatically, a silent 2FA push notification would be sent to mobile phone at random times, which would be quite easy to miss and result in a login failure. After a few consecutive failed attempts, IB may lock out the account and one has to contact customer service to unlock.

To avoid this, Minitrade only submits orders where there is already a working connection to a broker. If there is not, Minitrade sends messages via Telegram bot to notify that there are pending orders to be submitted. User should issue /ib login command manually to the bot to trigger a login to IB account. The 2FA push notification should be received in a few seconds and user can complete the login process on mobile phone. Once login is successful, Minitrade will be able to submit orders when trader runs again every 20 minutes.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file minitrade-0.1.8.tar.gz.

File metadata

- Download URL: minitrade-0.1.8.tar.gz

- Upload date:

- Size: 221.7 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: poetry/1.2.2 CPython/3.10.8 Darwin/22.3.0

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d87b6457b3f9dc25beb97597a2bffa944b1dee084265c3a09bfc6ce1bbd125d2

|

|

| MD5 |

14e4de3201c4e24dabe8694f0da28314

|

|

| BLAKE2b-256 |

5fb2f641ba28684c7fa8b23f530366cc52dff178045351134c33142d49317684

|

File details

Details for the file minitrade-0.1.8-py3-none-any.whl.

File metadata

- Download URL: minitrade-0.1.8-py3-none-any.whl

- Upload date:

- Size: 226.9 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: poetry/1.2.2 CPython/3.10.8 Darwin/22.3.0

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

b3e1c4023a64cc7c1dcbdf59db607bcaf66b94e969aa4779cdf66c21b595faf4

|

|

| MD5 |

288e6430c95dc2d99069f96644cf827f

|

|

| BLAKE2b-256 |

8a7b4650b34956cf5737c8478f8f4677ca185cd4e99ad278806bdff31530914c

|