A high-performance algorithmic trading platform and event-driven backtester

Project description

| Branch | Version | Status |

|---|---|---|

master |

|

|

nightly |

|

|

develop |

|

|

| Platform | Rust | Python |

|---|---|---|

Linux (x86_64) |

1.93.1 | 3.12-3.14 |

Linux (ARM64) |

1.93.1 | 3.12-3.14 |

macOS (ARM64) |

1.93.1 | 3.12-3.14 |

Windows (x86_64) |

1.93.1 | 3.12-3.14 |

- Docs: https://nautilustrader.io/docs/

- Website: https://nautilustrader.io

- Support: support@nautilustrader.io

Introduction

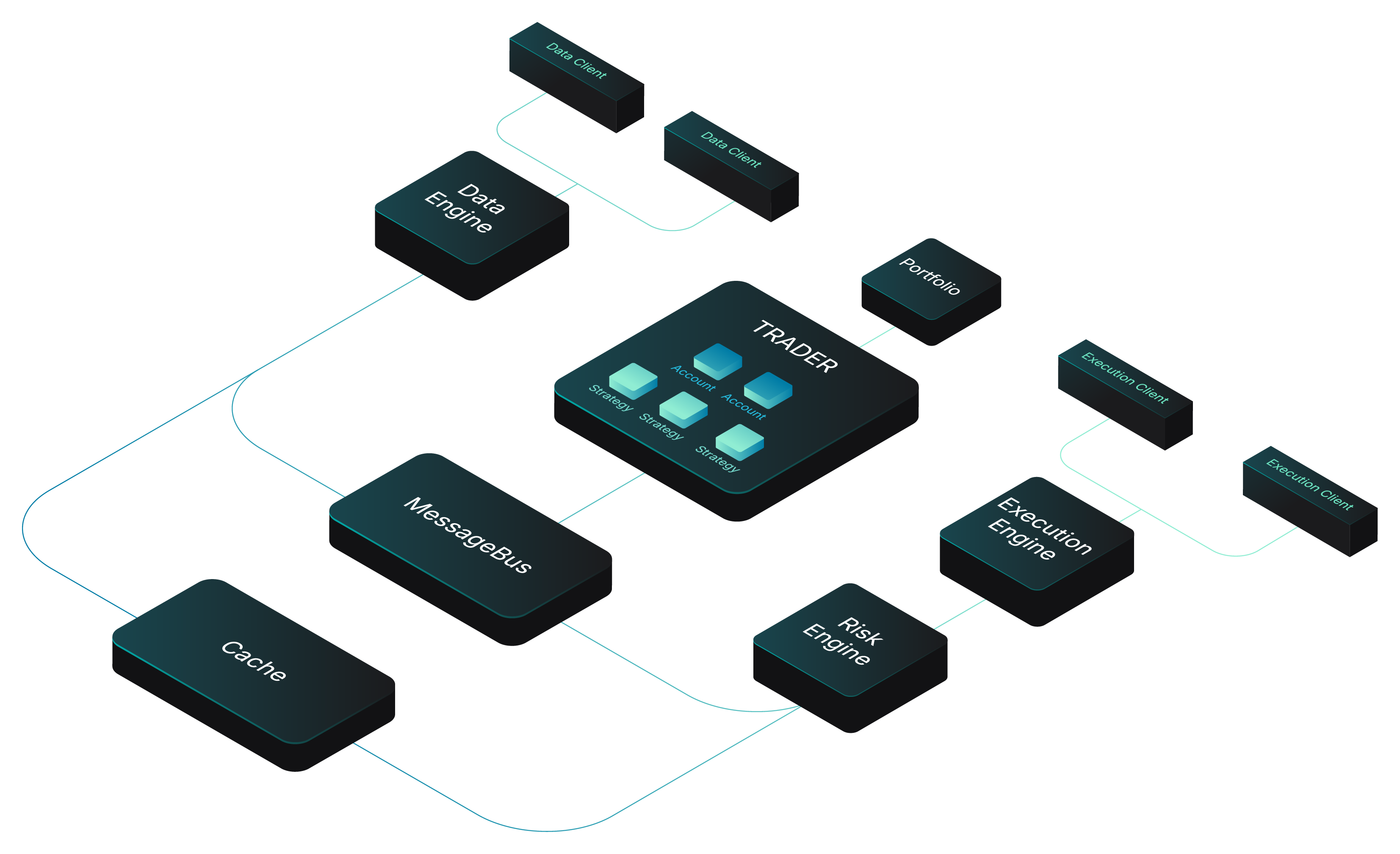

NautilusTrader is an open-source, high-performance, production-grade algorithmic trading platform, providing quantitative traders with the ability to backtest portfolios of automated trading strategies on historical data with an event-driven engine, and also deploy those same strategies live, with no code changes.

The platform is AI-first, designed to develop and deploy algorithmic trading strategies within a highly performant and robust Python-native environment. This helps to address the parity challenge of keeping the Python research/backtest environment consistent with the production live trading environment.

NautilusTrader's design, architecture, and implementation philosophy prioritizes software correctness and safety at the highest level, with the aim of supporting Python-native, mission-critical, trading system backtesting and live deployment workloads.

The platform is also universal, and asset-class-agnostic — with any REST API or WebSocket feed able to be integrated via modular adapters. It supports high-frequency trading across a wide range of asset classes and instrument types including FX, Equities, Futures, Options, Crypto, DeFi, and Betting — enabling seamless operations across multiple venues simultaneously.

Features

- Fast: Core is written in Rust with asynchronous networking using tokio.

- Reliable: Rust-powered type- and thread-safety, with optional Redis-backed state persistence.

- Portable: OS independent, runs on Linux, macOS, and Windows. Deploy using Docker.

- Flexible: Modular adapters mean any REST API or WebSocket feed can be integrated.

- Advanced: Time in force

IOC,FOK,GTC,GTD,DAY,AT_THE_OPEN,AT_THE_CLOSE, advanced order types and conditional triggers. Execution instructionspost-only,reduce-only, and icebergs. Contingency orders includingOCO,OUO,OTO. - Customizable: Add user-defined custom components, or assemble entire systems from scratch leveraging the cache and message bus.

- Backtesting: Run with multiple venues, instruments and strategies simultaneously using historical quote tick, trade tick, bar, order book and custom data with nanosecond resolution.

- Live: Use identical strategy implementations between backtesting and live deployments.

- Multi-venue: Multiple venue capabilities facilitate market-making and statistical arbitrage strategies.

- AI Training: Backtest engine fast enough to be used to train AI trading agents (RL/ES).

nautilus - from ancient Greek 'sailor' and naus 'ship'.

The nautilus shell consists of modular chambers with a growth factor which approximates a logarithmic spiral. The idea is that this can be translated to the aesthetics of design and architecture.

Why NautilusTrader?

- Highly performant event-driven Python: Native binary core components.

- Parity between backtesting and live trading: Identical strategy code.

- Reduced operational risk: Enhanced risk management functionality, logical accuracy, and type safety.

- Highly extendable: Message bus, custom components and actors, custom data, custom adapters.

Traditionally, trading strategy research and backtesting might be conducted in Python using vectorized methods, with the strategy then needing to be reimplemented in a more event-driven way using C++, C#, Java or other statically typed language(s). The reasoning here is that vectorized backtesting code cannot express the granular time and event dependent complexity of real-time trading, where compiled languages have proven to be more suitable due to their inherently higher performance, and type safety.

One of the key advantages of NautilusTrader here, is that this reimplementation step is now circumvented - as the critical core components of the platform have all been written entirely in Rust or Cython. This means we're using the right tools for the job, where systems programming languages compile performant binaries, with CPython C extension modules then able to offer a Python-native environment, suitable for professional quantitative traders and trading firms.

Why Python?

Python was originally created decades ago as a simple scripting language with a clean straightforward syntax. It has since evolved into a fully fledged general purpose object-oriented programming language. Based on the TIOBE index, Python is currently the most popular programming language in the world. Not only that, Python has become the de facto lingua franca of data science, machine learning, and artificial intelligence.

Why Rust?

Rust is a multi-paradigm programming language designed for performance and safety, especially safe concurrency. Rust is "blazingly fast" and memory-efficient (comparable to C and C++) with no garbage collector. It can power mission-critical systems, run on embedded devices, and easily integrates with other languages.

Rust's rich type system and ownership model guarantee memory-safety and thread-safety in safe code, eliminating many classes of bugs at compile-time. Overall safety in this project also depends on correctly upheld invariants in unsafe blocks and FFI boundaries.

The project utilizes Rust for core performance-critical components. Python bindings are implemented via Cython and PyO3—no Rust toolchain is required at install time.

This project makes the Soundness Pledge:

“The intent of this project is to be free of soundness bugs. The developers will do their best to avoid them, and welcome help in analyzing and fixing them.”

[!NOTE]

MSRV: NautilusTrader relies heavily on improvements in the Rust language and compiler. As a result, the Minimum Supported Rust Version (MSRV) is generally equal to the latest stable release of Rust.

Integrations

NautilusTrader is modularly designed to work with adapters, enabling connectivity to trading venues and data providers by translating their raw APIs into a unified interface and normalized domain model.

The following integrations are currently supported; see docs/integrations/ for details:

| Name | ID | Type | Status | Docs |

|---|---|---|---|---|

| AX Exchange | AX |

Perpetuals Exchange |  |

Guide |

| Architect | ARCHITECT |

Brokerage (multi-venue) |  |

- |

| Betfair | BETFAIR |

Sports Betting Exchange |  |

Guide |

| Binance | BINANCE |

Crypto Exchange (CEX) | |

Guide |

| BitMEX | BITMEX |

Crypto Exchange (CEX) | |

Guide |

| Bybit | BYBIT |

Crypto Exchange (CEX) | |

Guide |

| Coinbase International | COINBASE_INTX |

Crypto Exchange (CEX) | |

Guide |

| Databento | DATABENTO |

Data Provider | |

Guide |

| Deribit | DERIBIT |

Crypto Exchange (CEX) | |

Guide |

| dYdX | DYDX |

Crypto Exchange (DEX) | |

Guide |

| Hyperliquid | HYPERLIQUID |

Crypto Exchange (DEX) | |

Guide |

| Interactive Brokers | INTERACTIVE_BROKERS |

Brokerage (multi-venue) | |

Guide |

| Kraken | KRAKEN |

Crypto Exchange (CEX) | |

Guide |

| OKX | OKX |

Crypto Exchange (CEX) | |

Guide |

| Polymarket | POLYMARKET |

Prediction Market (DEX) | |

Guide |

| Tardis | TARDIS |

Crypto Data Provider | |

Guide |

- ID: The default client ID for the integrations adapter clients.

- Type: The type of integration (often the venue type).

Status

planned: Planned for future development.building: Under construction and likely not in a usable state.beta: Completed to a minimally working state and in a beta testing phase.stable: Stabilized feature set and API, the integration has been tested by both developers and users to a reasonable level (some bugs may still remain).

See the Integrations documentation for further details.

Roadmap

The Roadmap outlines NautilusTrader's strategic direction. Current priorities include porting the core to Rust, improving documentation, and enhancing code ergonomics.

The open-source project focuses on single-node backtesting and live trading for individual and small-team quantitative traders. UI dashboards, distributed orchestration, and built-in AI/ML tooling are out of scope to maintain focus on the core engine and ecosystem sustainability.

New integration proposals should start with an RFC issue to discuss suitability before submitting a PR. See Community-contributed integrations for guidelines.

Versioning and releases

[!WARNING]

NautilusTrader is still under active development. Some features may be incomplete, and while the API is becoming more stable, breaking changes can occur between releases. We strive to document these changes in the release notes on a best-effort basis.

We aim to follow a bi-weekly release schedule, though experimental or larger features may cause delays.

Branches

We aim to maintain a stable, passing build across all branches.

master: Reflects the source code for the latest released version; recommended for production use.nightly: Daily snapshots of thedevelopbranch for early testing; merged at 14:00 UTC and as required.develop: Active development branch for contributors and feature work.

[!NOTE]

Our roadmap aims to achieve a stable API for version 2.x (likely after the Rust port). Once this milestone is reached, we plan to implement a formal deprecation process for any API changes. This approach allows us to maintain a rapid development pace for now.

Precision mode

NautilusTrader supports two precision modes for its core value types (Price, Quantity, Money),

which differ in their internal bit-width and maximum decimal precision.

- High-precision: 128-bit integers with up to 16 decimals of precision, and a larger value range.

- Standard-precision: 64-bit integers with up to 9 decimals of precision, and a smaller value range.

[!NOTE]

By default, the official Python wheels ship in high-precision (128-bit) mode on Linux and macOS. On Windows, only standard-precision (64-bit) Python wheels are available because MSVC's C/C++ frontend does not support

__int128, preventing the Cython/FFI layer from handling 128-bit integers.For pure Rust crates, high-precision works on all platforms (including Windows) since Rust handles

i128/u128via software emulation. The default is standard-precision unless you explicitly enable thehigh-precisionfeature flag.

See the Installation Guide for further details.

Rust feature flag: To enable high-precision mode in Rust, add the high-precision feature to your Cargo.toml:

[dependencies]

nautilus_model = { version = "*", features = ["high-precision"] }

Installation

We recommend using the latest supported version of Python and installing nautilus_trader inside a virtual environment to isolate dependencies.

There are two supported ways to install:

- Pre-built binary wheel from PyPI or the Nautech Systems package index.

- Build from source.

[!TIP]

We highly recommend installing using the uv package manager with a "vanilla" CPython.

Conda and other Python distributions may work but aren’t officially supported.

From PyPI

To install the latest binary wheel (or sdist package) from PyPI using Python's pip package manager:

pip install -U nautilus_trader

Install optional dependencies as 'extras' for specific integrations (e.g., betfair, docker, dydx, ib, polymarket, visualization):

pip install -U "nautilus_trader[docker,ib]"

See the Installation Guide for the full list of available extras.

From the Nautech Systems package index

The Nautech Systems package index (packages.nautechsystems.io) complies with PEP-503 and hosts both stable and development binary wheels for nautilus_trader.

This enables users to install either the latest stable release or pre-release versions for testing.

Stable wheels

Stable wheels correspond to official releases of nautilus_trader on PyPI, and use standard versioning.

To install the latest stable release:

pip install -U nautilus_trader --index-url=https://packages.nautechsystems.io/simple

[!TIP]

Use

--extra-index-urlinstead of--index-urlif you want pip to fall back to PyPI automatically.

Development wheels

Development wheels are published from both the nightly and develop branches,

allowing users to test features and fixes ahead of stable releases.

This process also helps preserve compute resources and provides easy access to the exact binaries tested in CI pipelines, while adhering to PEP-440 versioning standards:

developwheels use the version formatdev{date}+{build_number}(e.g.,1.208.0.dev20241212+7001).nightlywheels use the version formata{date}(alpha) (e.g.,1.208.0a20241212).

| Platform | Nightly | Develop |

|---|---|---|

Linux (x86_64) |

✓ | ✓ |

Linux (ARM64) |

✓ | - |

macOS (ARM64) |

✓ | ✓ |

Windows (x86_64) |

✓ | ✓ |

Note: Development wheels from the develop branch publish for every supported platform except Linux ARM64.

Skipping that target keeps CI feedback fast while avoiding unnecessary build resource usage.

[!WARNING]

We do not recommend using development wheels in production environments, such as live trading controlling real capital.

Installation commands

By default, pip will install the latest stable release. Adding the --pre flag ensures that pre-release versions, including development wheels, are considered.

To install the latest available pre-release (including development wheels):

pip install -U nautilus_trader --pre --index-url=https://packages.nautechsystems.io/simple

To install a specific development wheel (e.g., 1.221.0a20251026 for October 26, 2025):

pip install nautilus_trader==1.221.0a20251026 --index-url=https://packages.nautechsystems.io/simple

Available versions

You can view all available versions of nautilus_trader on the package index.

To programmatically fetch and list available versions:

curl -s https://packages.nautechsystems.io/simple/nautilus-trader/index.html | grep -oP '(?<=<a href=")[^"]+(?=")' | awk -F'#' '{print $1}' | sort

[!NOTE]

On Linux, confirm your glibc version with

ldd --versionand ensure it reports 2.35 or newer before installing binary wheels.

Branch updates

developbranch wheels (.dev): Build and publish continuously with every merged commit.nightlybranch wheels (a): Build and publish daily when we automatically merge thedevelopbranch at 14:00 UTC (if there are changes).

Retention policies

developbranch wheels (.dev): We retain only the most recent wheel build.nightlybranch wheels (a): We retain only the 30 most recent wheel builds.

Verifying build provenance

All release artifacts (wheels and source distributions) published to PyPI, GitHub Releases, and the Nautech Systems package index include cryptographic attestations that prove their authenticity and build provenance.

These attestations are generated automatically during the CI/CD pipeline using SLSA build provenance, and can be verified to ensure:

- The artifact was built by the official NautilusTrader GitHub Actions workflow.

- The artifact corresponds to a specific commit SHA in the repository.

- The artifact hasn't been tampered with since it was built.

To verify a wheel file using the GitHub CLI:

gh attestation verify nautilus_trader-1.220.0-*.whl --owner nautechsystems

This provides supply chain security by allowing you to cryptographically verify that the installed package came from the official NautilusTrader build process.

[!NOTE]

Attestation verification requires the GitHub CLI (

gh) to be installed. Development wheels fromdevelopandnightlybranches are also attested and can be verified the same way.

From source

It's possible to install from source using pip if you first install the build dependencies as specified in the pyproject.toml.

-

Install rustup (the Rust toolchain installer):

-

Linux and macOS:

curl https://sh.rustup.rs -sSf | sh

-

Windows:

- Download and install

rustup-init.exe - Install "Desktop development with C++" using Build Tools for Visual Studio 2022

- Download and install

-

Verify (any system): from a terminal session run:

rustc --version

-

-

Enable

cargoin the current shell:-

Linux and macOS:

source $HOME/.cargo/env

-

Windows:

- Start a new PowerShell

-

-

Install clang (a C language frontend for LLVM):

-

Linux:

sudo apt-get install clang

-

macOS:

xcode-select --install -

Windows:

-

Add Clang to your Build Tools for Visual Studio 2022:

- Start | Visual Studio Installer | Modify | C++ Clang tools for Windows (latest) = checked | Modify

-

Enable

clangin the current shell:[System.Environment]::SetEnvironmentVariable('path', "C:\Program Files\Microsoft Visual Studio\2022\BuildTools\VC\Tools\Llvm\x64\bin\;" + $env:Path,"User")

-

-

Verify (any system): from a terminal session run:

clang --version

-

-

Install uv (see the uv installation guide for more details):

-

Linux and macOS:

curl -LsSf https://astral.sh/uv/install.sh | sh

-

Windows (PowerShell):

irm https://astral.sh/uv/install.ps1 | iex

-

-

Clone the source with

git, and install from the project's root directory:git clone --branch develop --depth 1 https://github.com/nautechsystems/nautilus_trader cd nautilus_trader uv sync --all-extras

[!NOTE]

The

--depth 1flag fetches just the latest commit for a faster, lightweight clone.

-

Set environment variables for PyO3 compilation (Linux and macOS only):

# Linux only: Set the library path for the Python interpreter export LD_LIBRARY_PATH="$(python -c 'import sys; print(sys.base_prefix)')/lib:$LD_LIBRARY_PATH" # Set the Python executable path for PyO3 export PYO3_PYTHON=$(pwd)/.venv/bin/python # Required for Rust tests when using uv-installed Python export PYTHONHOME=$(python -c "import sys; print(sys.base_prefix)")

[!NOTE]

The

LD_LIBRARY_PATHexport is Linux-specific and not needed on macOS.The

PYTHONHOMEvariable is required when runningmake cargo-testwith auv-installed Python. Without it, tests that depend on PyO3 may fail to locate the Python runtime.

See the Installation Guide for other options and further details.

Redis

Using Redis with NautilusTrader is optional and only required if configured as the backend for a cache database or message bus. See the Redis section of the Installation Guide for further details.

Makefile

A Makefile is provided to automate most installation and build tasks for development. Some of the targets include:

make install: Installs inreleasebuild mode with all dependency groups and extras.make install-debug: Same asmake installbut withdebugbuild mode.make install-just-deps: Installs just themain,devandtestdependencies (does not install package).make build: Runs the build script inreleasebuild mode (default).make build-debug: Runs the build script indebugbuild mode.make build-wheel: Runs uv build with a wheel format inreleasemode.make build-wheel-debug: Runs uv build with a wheel format indebugmode.make cargo-test: Runs all Rust crate tests usingcargo-nextest.make clean: Deletes all build results, such as.soor.dllfiles.make distclean: CAUTION Removes all artifacts not in the git index from the repository. This includes source files which have not beengit added.make docs: Builds the documentation HTML using Sphinx.make pre-commit: Runs the pre-commit checks over all files.make ruff: Runs ruff over all files using thepyproject.tomlconfig (with autofix).make pytest: Runs all tests withpytest.make test-performance: Runs performance tests with codspeed.

[!TIP]

Run

make helpfor documentation on all available make targets.

[!TIP]

See the crates/infrastructure/TESTS.md file for running the infrastructure integration tests.

Examples

Indicators and strategies can be developed in both Python and Cython. For performance and latency-sensitive applications, we recommend using Cython. Below are some examples:

- indicator example written in Python.

- indicator implementations written in Cython.

- strategy examples written in Python.

- backtest examples using a

BacktestEnginedirectly.

Docker

Docker containers are built using the base image python:3.12-slim with the following variant tags:

nautilus_trader:latesthas the latest release version installed.nautilus_trader:nightlyhas the head of thenightlybranch installed.jupyterlab:latesthas the latest release version installed along withjupyterlaband an example backtest notebook with accompanying data.jupyterlab:nightlyhas the head of thenightlybranch installed along withjupyterlaband an example backtest notebook with accompanying data.

You can pull the container images as follows:

docker pull ghcr.io/nautechsystems/<image_variant_tag> --platform linux/amd64

You can launch the backtest example container by running:

docker pull ghcr.io/nautechsystems/jupyterlab:nightly --platform linux/amd64

docker run -p 8888:8888 ghcr.io/nautechsystems/jupyterlab:nightly

Then open your browser at the following address:

http://127.0.0.1:8888/lab

[!WARNING]

NautilusTrader currently exceeds the rate limit for Jupyter notebook logging (stdout output). Therefore, we set the

log_leveltoERRORin the examples. Lowering this level to see more logging will cause the notebook to hang during cell execution. We are investigating a fix that may involve either raising the configured rate limits for Jupyter or throttling the log flushing from Nautilus.

Development

We aim to provide the most pleasant developer experience possible for this hybrid codebase of Python, Cython and Rust. See the Developer Guide for helpful information.

[!TIP]

Run

make build-debugto compile after changes to Rust or Cython code for the most efficient development workflow.

Testing with Rust

cargo-nextest is the standard Rust test runner for NautilusTrader. Its key benefit is isolating each test in its own process, ensuring test reliability by avoiding interference.

You can install cargo-nextest by running:

cargo install cargo-nextest

[!TIP]

Run Rust tests with

make cargo-test, which uses cargo-nextest with an efficient profile.

Contributing

Thank you for considering contributing to NautilusTrader! We welcome any and all help to improve the project. If you have an idea for an enhancement or a bug fix, the first step is to open an issue on GitHub to discuss it with the team. This helps to ensure that your contribution will be well-aligned with the goals of the project and avoids duplication of effort.

Before getting started, be sure to review the open-source scope outlined in the project’s roadmap to understand what’s in and out of scope.

Once you're ready to start working on your contribution, make sure to follow the guidelines outlined in the CONTRIBUTING.md file. This includes signing a Contributor License Agreement (CLA) to ensure that your contributions can be included in the project.

[!NOTE]

Pull requests should target the

developbranch (the default branch). This is where new features and improvements are integrated before release.

Thank you again for your interest in NautilusTrader! We look forward to reviewing your contributions and working with you to improve the project.

Community

Join our community of users and contributors on Discord to chat and stay up-to-date with the latest announcements and features of NautilusTrader. Whether you're a developer looking to contribute or just want to learn more about the platform, all are welcome on our Discord server.

[!WARNING]

NautilusTrader does not issue, promote, or endorse any cryptocurrency tokens. Any claims or communications suggesting otherwise are unauthorized and false.

All official updates and communications from NautilusTrader will be shared exclusively through https://nautilustrader.io, our Discord server, or our X (Twitter) account: @NautilusTrader.

If you encounter any suspicious activity, please report it to the appropriate platform and contact us at info@nautechsystems.io.

License

The source code for NautilusTrader is available on GitHub under the GNU Lesser General Public License v3.0. Contributions to the project are welcome and require the completion of a standard Contributor License Agreement (CLA).

NautilusTrader™ is developed and maintained by Nautech Systems, a technology company specializing in the development of high-performance trading systems. For more information, visit https://nautilustrader.io.

© 2015-2026 Nautech Systems Pty Ltd. All rights reserved.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distributions

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file nautilus_trader-1.223.0.tar.gz.

File metadata

- Download URL: nautilus_trader-1.223.0.tar.gz

- Upload date:

- Size: 5.2 MB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

4f623dbc7bd74dccd0b20da2bc06fad2be2088c860bd4beb16fba240f303ce1a

|

|

| MD5 |

67e17cfe3d4e52e7614787048e03c442

|

|

| BLAKE2b-256 |

9e98bc92d031e9324411ea8b1942e6be366d0e51ef0cb570687d17a2b1a3a399

|

File details

Details for the file nautilus_trader-1.223.0-cp314-cp314-win_amd64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp314-cp314-win_amd64.whl

- Upload date:

- Size: 49.6 MB

- Tags: CPython 3.14, Windows x86-64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

a275c7a47dab503f1612987b0c4c171a9960b4f8f4c8bab45f9b3cd2b0e2095c

|

|

| MD5 |

db060e859006cf22bb1bf7ef1951827a

|

|

| BLAKE2b-256 |

d2465c6dd98c34df7a05d18dfd7e87655131f16d9f7d3bcd0014982ffc908627

|

File details

Details for the file nautilus_trader-1.223.0-cp314-cp314-manylinux_2_35_x86_64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp314-cp314-manylinux_2_35_x86_64.whl

- Upload date:

- Size: 93.1 MB

- Tags: CPython 3.14, manylinux: glibc 2.35+ x86-64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d6621f86fced0cf75663a101d66959c98640c27717bd2f35bea1684d842b1712

|

|

| MD5 |

6d38a1a434dc63ce773af47a83b9142f

|

|

| BLAKE2b-256 |

b6cb5d791eff5606e4fa8ed49e888e52107ceab66552f01d053a59bafc02d431

|

File details

Details for the file nautilus_trader-1.223.0-cp314-cp314-manylinux_2_35_aarch64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp314-cp314-manylinux_2_35_aarch64.whl

- Upload date:

- Size: 87.3 MB

- Tags: CPython 3.14, manylinux: glibc 2.35+ ARM64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

4d3ab0b99f82b41b42132a03c0a6ce1da412fcd7ca8cb7fb753d03664a37bbde

|

|

| MD5 |

6abf24619d81e590bf4c26538facd2ac

|

|

| BLAKE2b-256 |

6858c8989aa6b6c6ff68e5345c24bcd46cd35805fb13279f5f6b33ee6e8d8d3d

|

File details

Details for the file nautilus_trader-1.223.0-cp314-cp314-macosx_15_0_arm64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp314-cp314-macosx_15_0_arm64.whl

- Upload date:

- Size: 82.7 MB

- Tags: CPython 3.14, macOS 15.0+ ARM64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

7ad67b93486491134a65f1a60f710701c093a2e943c4a8a103ea1d8fed0a7d79

|

|

| MD5 |

e2e9d3c6f637ae4a590396c106f53484

|

|

| BLAKE2b-256 |

3f8059d66d26fe8a1f1efdc0abe85afc54794b1b1238a5bbd8d88ceb8e9403ae

|

File details

Details for the file nautilus_trader-1.223.0-cp313-cp313-win_amd64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp313-cp313-win_amd64.whl

- Upload date:

- Size: 48.4 MB

- Tags: CPython 3.13, Windows x86-64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

1a765d6f39547cc85bfe99b60fc67763fd13ba754330511554e3339aea01e3e1

|

|

| MD5 |

4cc53eb102377b3f58c2b333ced8d24d

|

|

| BLAKE2b-256 |

62da2ab6d76e96acb7a83e9ba8f5db0d3bc84580bf88e7ede3fc5c6f2666d680

|

File details

Details for the file nautilus_trader-1.223.0-cp313-cp313-manylinux_2_35_x86_64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp313-cp313-manylinux_2_35_x86_64.whl

- Upload date:

- Size: 93.1 MB

- Tags: CPython 3.13, manylinux: glibc 2.35+ x86-64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

3d0a31769dfd9af7d3638bf3d1d1d12d9180354ac3b1296dca483ae250280ca7

|

|

| MD5 |

a92ce956609ea9131d12c32b754cc184

|

|

| BLAKE2b-256 |

ef02bead2b74a6384d519720e44318a05d6a8140eaecf476c424d791606a6bfd

|

File details

Details for the file nautilus_trader-1.223.0-cp313-cp313-manylinux_2_35_aarch64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp313-cp313-manylinux_2_35_aarch64.whl

- Upload date:

- Size: 87.3 MB

- Tags: CPython 3.13, manylinux: glibc 2.35+ ARM64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

4f899559ae74c161bc816282d06402b4728fa0a78b8c6866c5055c6700c6fe9b

|

|

| MD5 |

811c92c0052974bc93c5ce0a751c684b

|

|

| BLAKE2b-256 |

b815c022a1e3b172fbe805d7325747a2fb1760be83361b8b7b4b19c28557f4fc

|

File details

Details for the file nautilus_trader-1.223.0-cp313-cp313-macosx_15_0_arm64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp313-cp313-macosx_15_0_arm64.whl

- Upload date:

- Size: 82.6 MB

- Tags: CPython 3.13, macOS 15.0+ ARM64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d21d1e0daea3d9a18f7b74caf6602d40af1bb0dba4fb926668c8e890ae5503f1

|

|

| MD5 |

370228fee5ee1e99b84785d14d84f832

|

|

| BLAKE2b-256 |

4a2f17da0c8ad940af8f2ae3982be022d37861219b4d5602b7199c046feacf9b

|

File details

Details for the file nautilus_trader-1.223.0-cp312-cp312-win_amd64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp312-cp312-win_amd64.whl

- Upload date:

- Size: 48.4 MB

- Tags: CPython 3.12, Windows x86-64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

4e0d7aee6632a350dc0f590af0096f228d4702b027924d911696cba62c4c1456

|

|

| MD5 |

b7c2954859c66a3e1cb4749b5abc8eae

|

|

| BLAKE2b-256 |

18bdfe89ac8bdf19fe020532697d89ff88ae7cc83c7e46c0cca7496bf9459043

|

File details

Details for the file nautilus_trader-1.223.0-cp312-cp312-manylinux_2_35_x86_64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp312-cp312-manylinux_2_35_x86_64.whl

- Upload date:

- Size: 93.2 MB

- Tags: CPython 3.12, manylinux: glibc 2.35+ x86-64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

20a022ef35fb56e16aa1618d2b931d2d6d4b8e389f711cf3d2cd99cb9ef45738

|

|

| MD5 |

f25a2fec53077bafc5815ee0e7a78913

|

|

| BLAKE2b-256 |

bd5475193e221fc1d52147e15147e98f05b67669f3916467addcfc91f669e2f0

|

File details

Details for the file nautilus_trader-1.223.0-cp312-cp312-manylinux_2_35_aarch64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp312-cp312-manylinux_2_35_aarch64.whl

- Upload date:

- Size: 87.2 MB

- Tags: CPython 3.12, manylinux: glibc 2.35+ ARM64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

fe7e05ad0a2d3dc17718dcbb80561fa8d9d11783e770369a7bff39e1fd6b514f

|

|

| MD5 |

64608b8c2322b4df7cf52ec5b9069a2c

|

|

| BLAKE2b-256 |

6134bfb9c30600c7c74f24c02520355cb85bed039e596b6d95d090fc20ac3045

|

File details

Details for the file nautilus_trader-1.223.0-cp312-cp312-macosx_15_0_arm64.whl.

File metadata

- Download URL: nautilus_trader-1.223.0-cp312-cp312-macosx_15_0_arm64.whl

- Upload date:

- Size: 82.5 MB

- Tags: CPython 3.12, macOS 15.0+ ARM64

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.10.4 {"installer":{"name":"uv","version":"0.10.4","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

6eb91f7e35de9445f55644cc675ba83f62a6c8f1d0bc7ceb8cef99c43ce4967e

|

|

| MD5 |

6fae300898d6ea8424246f3aa05b36e7

|

|

| BLAKE2b-256 |

340bd79e2b1c470fa16c7dba83f9ca00c7697b11ba9f23d677767f0830f90803

|