The world's most elegant, institutional-grade quantitative risk API.

Project description

Nexus: The Enterprise Quantitative Risk Framework

Welcome to Nexus. Nexus is an institutional-grade library implementing 40+ advanced risk measurements, including classical metrics, downside asymmetry, tail exceedance, and convex entropic bounds (EVaR, EDaR, RLDaR).

Inspired by scikit-learn and Google's core architectures, Nexus seamlessly abstracts disjointed mathematical scripts into a devastatingly powerful execution manifold: the NexusAnalyzer. Whether you are an indie quant building alpha models who has identified undervalued opportunities, or a Wall Street hedge fund requiring millisecond precision optimizations via MOSEK/CVXPY, Nexus provides the native mathematical infrastructure needed to evaluate and construct risk-efficient portfolios.

| Documentation · Tutorials · Release Notes | |

|---|---|

| Open Source |   |

| Tutorials |  |

| Community |   |

| CI/CD |   |

| Code |    |

| Downloads |    |

Table of contents

- 📚 Official Documentation

- Why Nexus?

- Getting started

- Features & Mathematical Supremacy

- Unparalleled Solver Routing

- Project Principles

- Installation

- Testing & Developer Setup

- License & Disclaimer

📚 Official Documentation

Nexus is built with the rigor and scale of Tier-1 technology groups (such as DeepMind or Google Research), cleanly abstracting extreme mathematical theories into a functional programmatic mesh.

For an exhaustive and mathematically rigorous breakdown of our architectural patterns, Entropic bounds, solver routing algorithms, and a complete API reference, please consult the official ReadTheDocs portal:

📖 Read the Full Documentation on ReadTheDocs ➔

The documentation deeply covers:

- Core Architecture & The Analyzer Facade

- Dynamic Solver Fallbacks (MOSEK/CVXPY Integration)

- Entropic Mathematics & Chernoff Boundaries

- Comprehensive Data Handling Pipelines

Why Nexus?

Nexus was explicitly engineered for absolute scale and mathematical extremity.

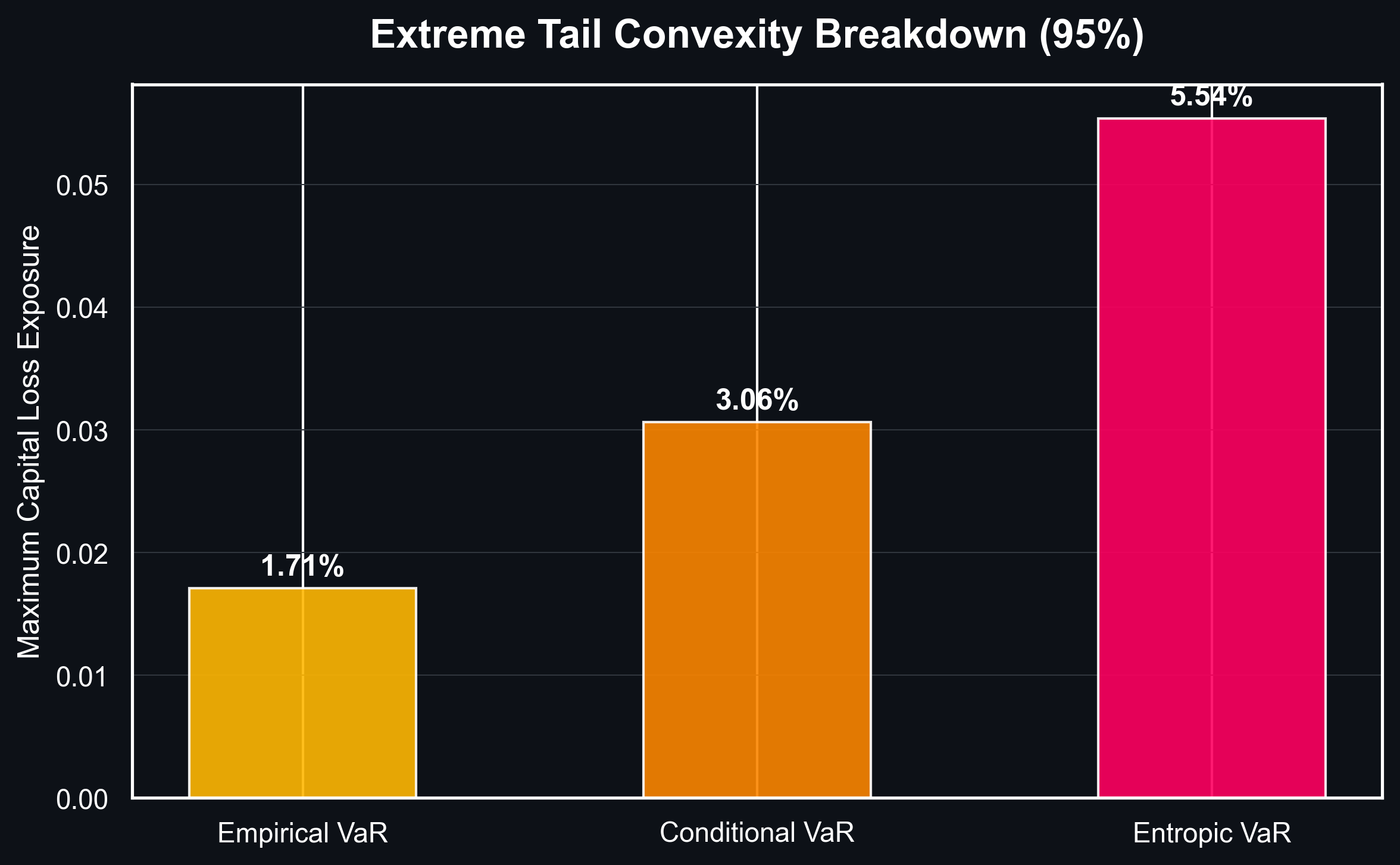

- Convex Entropic Supremacy: Standard libraries rely on empirical Historical VaR or CVaR. Nexus natively implements Entropic Value at Risk (EVaR) and Relativistic VaR (RLVaR), bounding tail risks using strict Chernoff inequalities that are completely invisible to standard historical sampling.

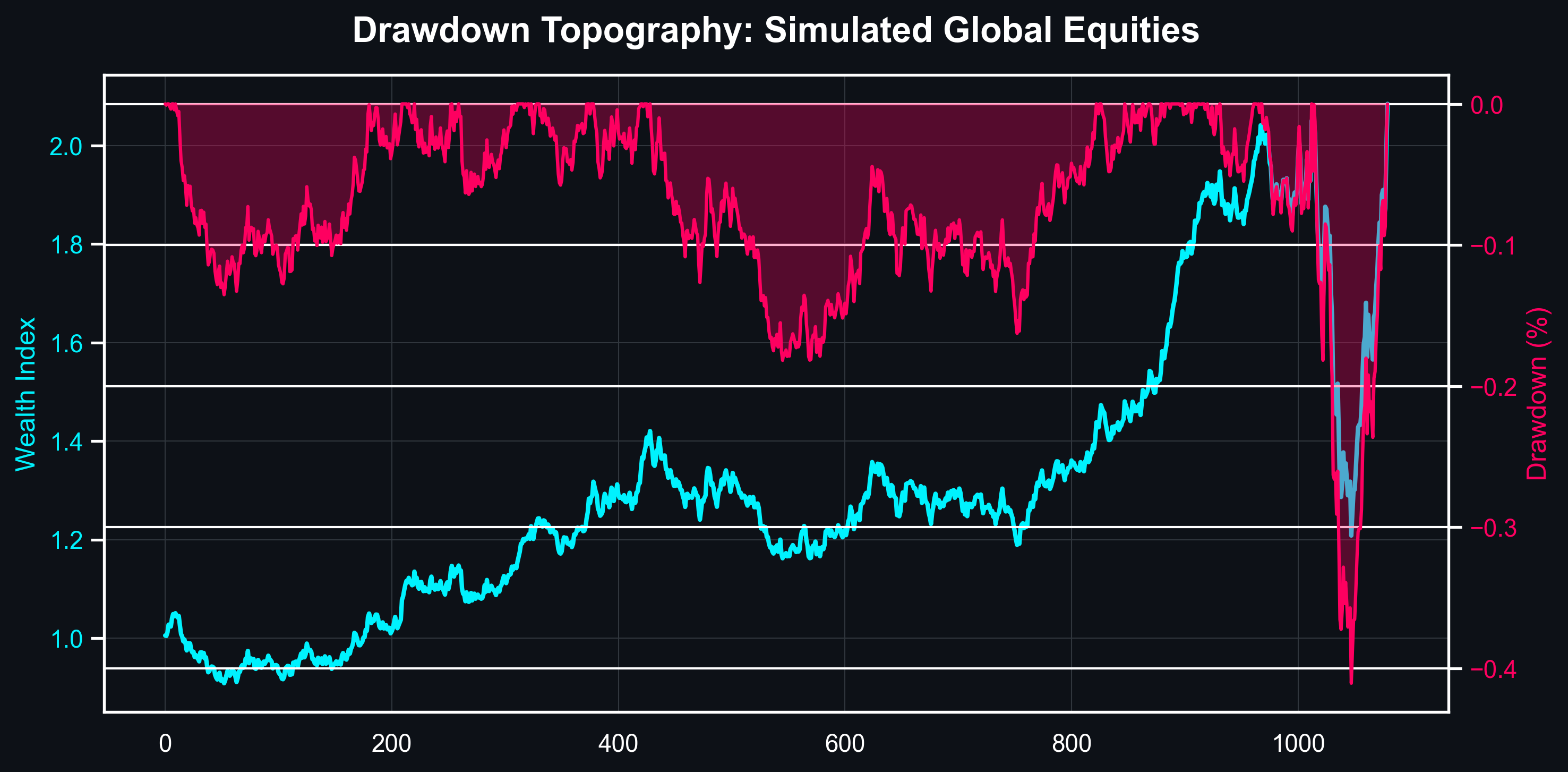

- Path-Dependent Drawdown Cones: Nexus introduces Entropic Drawdown at Risk (EDaR), a revolutionary metric mapping underwater geometric capital erosion onto exponential mathematically-bound cones, rather than just simple peak-to-trough calculations.

- Dynamic Solver Fallbacks: Nexus detects institutional optimization licenses (MOSEK/GUROBI) and perfectly routes extreme thermodynamics through them via

cvxpy. If licenses are missing, it flawlessly falls back to high-gradescipyoptimizers without crashing your analytical pipeline.

Getting started

Gone are the days of importing disjointed functions. Nexus abstracts the entire mathematical realm into a single NexusAnalyzer object. Here is an example demonstrating how easy it is to fetch real-life stock data and construct an exhaustive mathematical risk report matrix natively.

import numpy as np

from nexus.data.loader import NexusDataLoader

from nexus.analytics.analyzer import NexusAnalyzer

# 1. Effortless Market Ingestion

loader = NexusDataLoader()

asset_names, historical_returns = loader.fetch(

['AAPL', 'MSFT', 'JPM'],

start_date='2020-01-01'

)

# Build an equal-weighted portfolio combination

weights = np.ones(len(asset_names)) / len(asset_names)

portfolio_returns = np.sum(historical_returns * weights, axis=1)

# 2. Institutional Calibration

analyzer = NexusAnalyzer()

analyzer.calibrate(portfolio_returns)

# 3. Exhaustive Mathematical Execution

report_df = analyzer.compute(alpha=0.05, annualization_factor=252)

# Specific Dictionary Retrieval

cvar = analyzer.fetch('Cond VaR (0.05)')

print(report_df)

The Output

Asset_0

Volatility (Ann) 0.230763

Mean Abs Dev (MAD) 2.388695

Gini Mean Diff 3.579301

Lower Part Moment (LPM1) 1.096828

Value at Risk (0.05) 0.019100

Cond VaR (0.05) 0.033262

Entropic VaR (0.05) 0.067949

Cond DaR (0.05) -0.232770

Entropic DaR (0.05) 0.259398

Max Drawdown (MDD) -0.344122

Ulcer Index 0.091181

Calmar Ratio 0.884100

...

Features & Mathematical Supremacy

In this section, we detail Nexus' primary architectural pillars. More exhaustive equations can be found in our core modules.

Return Regimes & Asset Efficiency

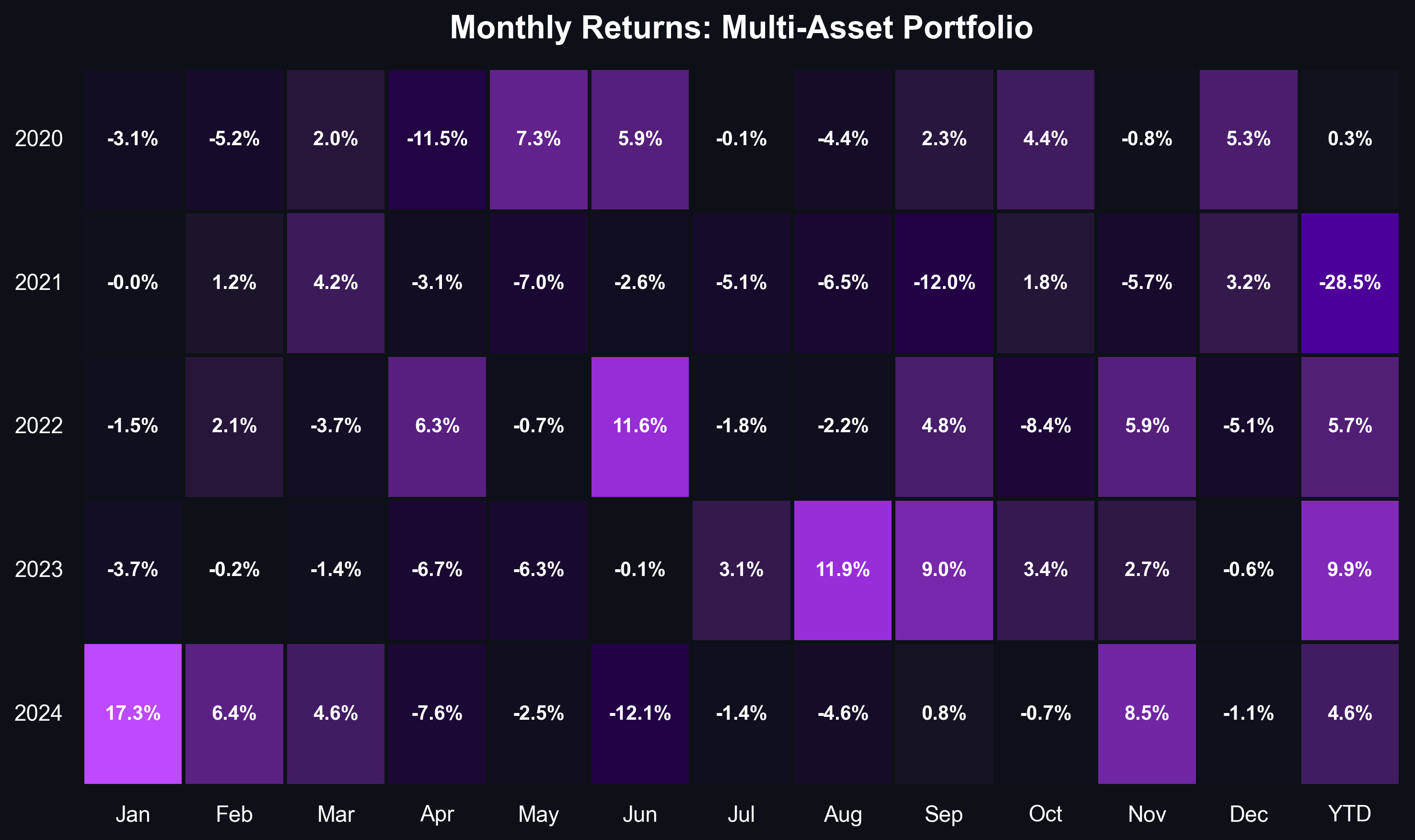

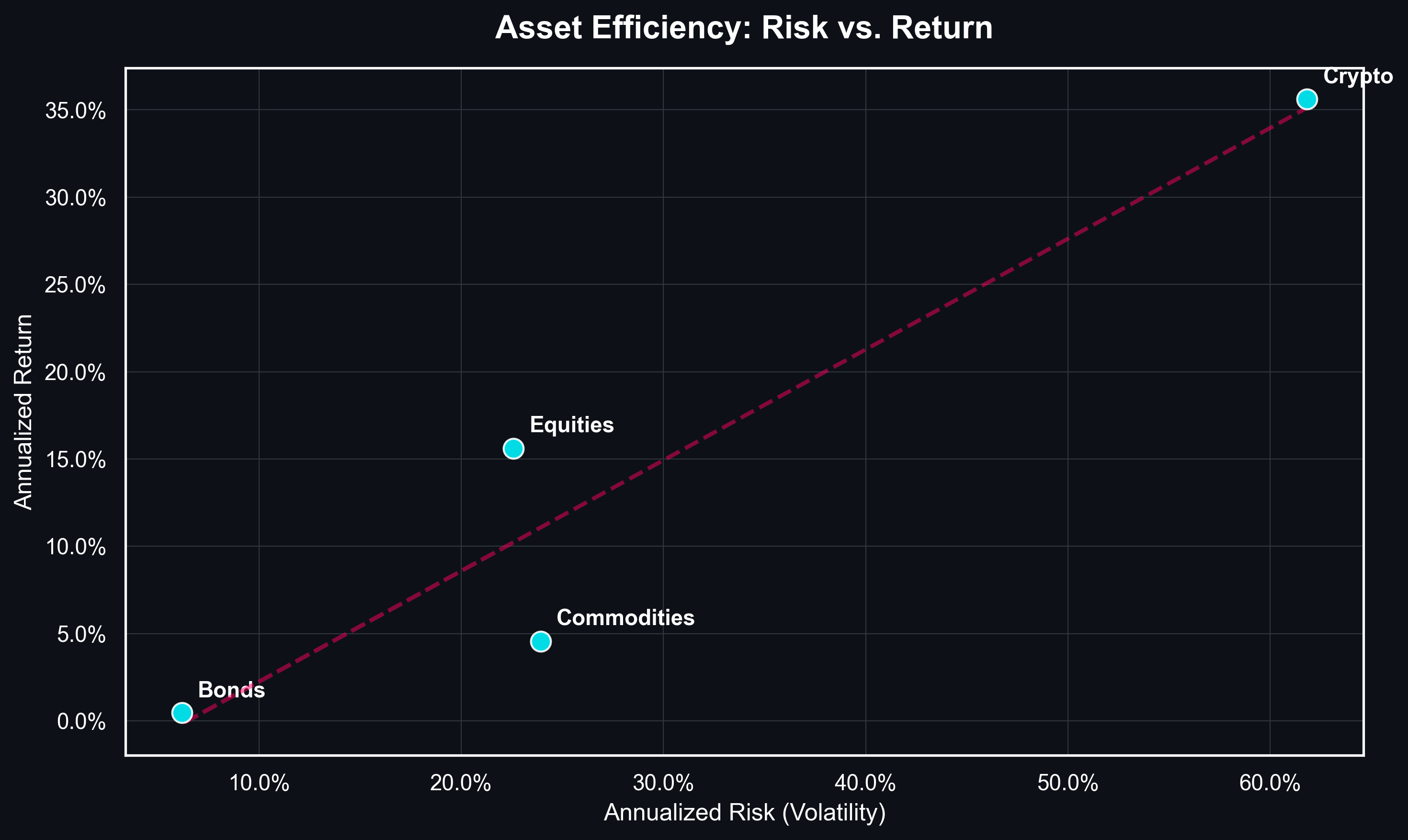

Institutional portfolio management relies on hierarchical clustering of temporal returns and risk-adjusted efficiency plotting.

- Chronological Return Clustering: QuantStats-style Y/M grids isolating momentum drifts, tax-loss harvesting impacts, and macro-regime seasonality across annual structures.

- Asset Efficiency Hierarchies: Volatility vs. Return distributions mapping exactly which singular assets dominate the local efficient frontier.

Multivariate Dynamics & Temporal Regimes

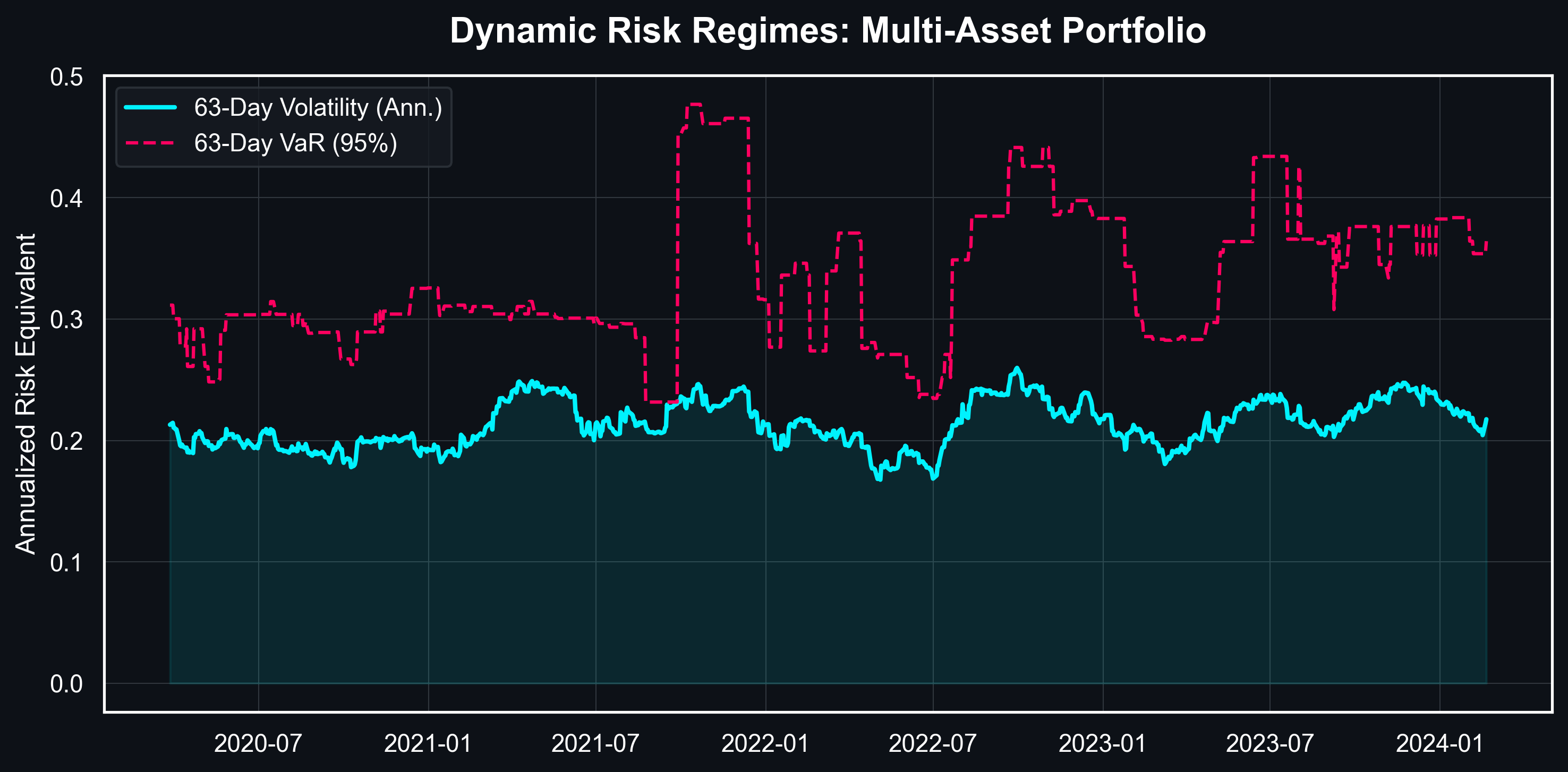

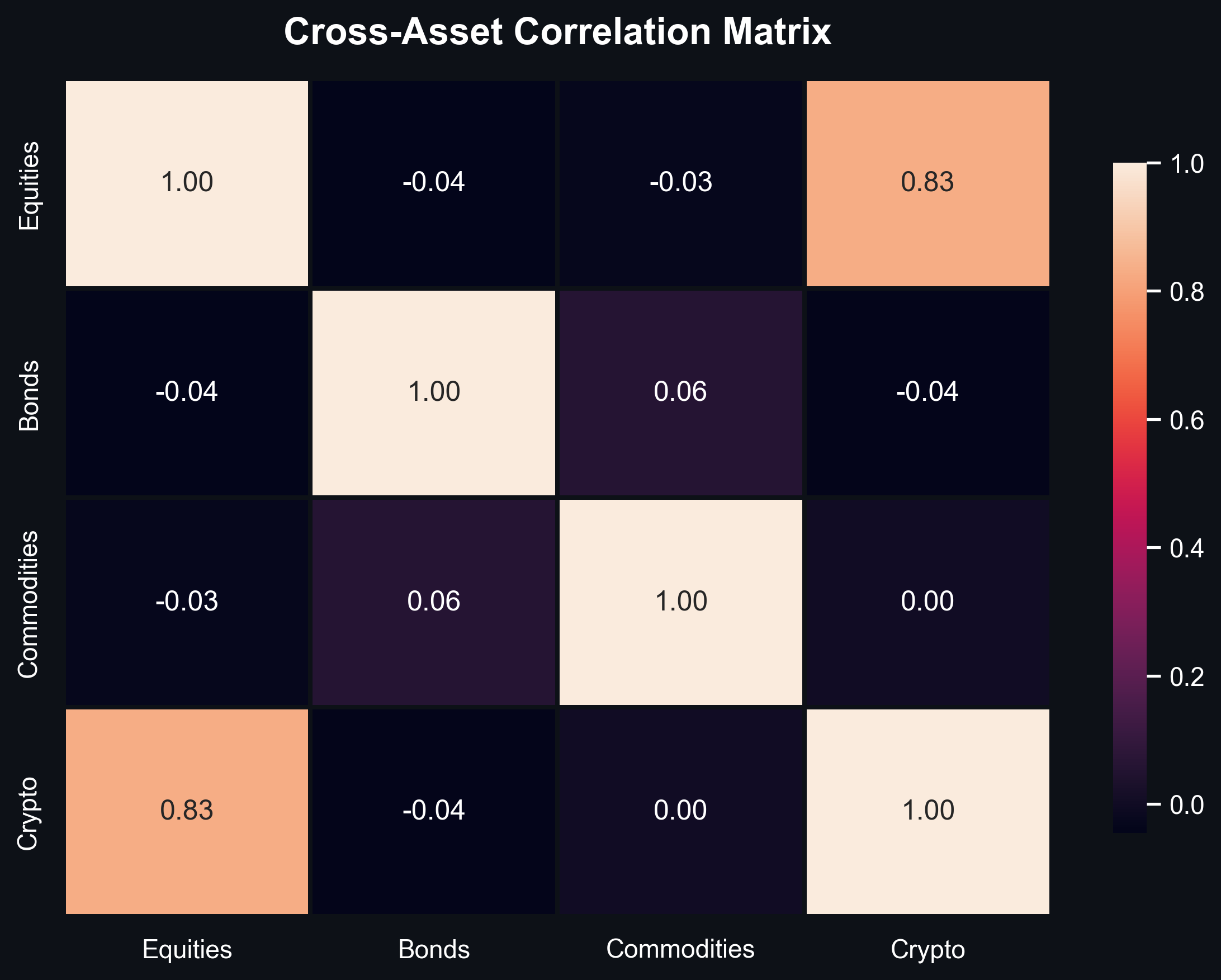

Understanding how risks evolve over time and across asset classes is paramount. Nexus natively maps high-dimensional data flows into temporal matrices, detecting structural regime shifts before they breach limits.

- Rolling Structural Volatility: Maps moving-window variance structures directly against overlapping 95% Historical VaR clusters, instantly revealing structural macro-regime changes.

- Cross-Asset Covariance & Pearson Dependencies: Instantly maps deep empirical correlation heatmaps to guarantee zero concentration overlaps across distinct asset silos (Equities, Bonds, Crypto, Commodities).

Dispersion & Volatility

- Standard Deviation & Variance: The classical unbiased measures of historical risk.

- Mean Absolute Deviation (MAD): A perfectly robust scale metric lacking the extreme parabolic sensitivity of squared variance.

- Gini Mean Difference: A powerful absolute deviation measurement utilized in modern asset allocation.

- L-Scale: The second L-Moment representing linear combinations of order statistics.

Downside Asymmetry

- Semi-Deviation: A measure of risk that focuses purely on downside variation heavily penalized by investors.

- Lower Partial Moments (LPM): Generalized objective functions for asymmetric downside measurements parameterized by target acceptable return (

MAR).

Tail Exceedance

- Value at Risk (VaR): The industry-standard empirical percentile of the maximum loss over a targeted confidence interval $\alpha$.

- Conditional VaR (CVaR/Expected Shortfall): The expected loss given that the VaR threshold has been breached. Structurally coherent.

- Tail Gini: A unique generalized formulation merging CVaR with Gini mean difference within extreme domains.

Convex Entropic Bounds

- Entropic Value at Risk (EVaR): The tightest coherent upper bound on VaR historically derived strictly from the Chernoff inequality. Extremely responsive to extreme market shocks.

- Relativistic VaR (RLVaR): A massive 3D power-cone deformation scaling Entropic bounds to asymmetric generalized logarithmic divergences.

- Entropic Drawdown at Risk (EDaR): A revolutionary path-dependent risk metric combining geometric Chernoff bounds with historical peak-to-trough waterfall drawdowns.

Unparalleled Solver Routing

Nexus was built to scale from individual traders directly to high-frequency servers natively.

Its generalized convex penalty equations computationally detect commercial optimization licenses (like MOSEK or GUROBI via CVXPY).

- If found, it natively routes extreme computations (EVaR, EDaR, RLVaR) through absolute mathematical exponential cones, achieving millisecond precision over millions of market datapoints.

- If not found, it miraculously falls back to high-grade

scipy.optimize.minimizeopen-source algorithmic optimization without crashing.

Project principles and design decisions

- Modularity: It should be easy to swap out individual components of the analytical process with the user's proprietary improvements.

- Mathematical Transparency: All functions are internally documented with strict $\LaTeX$ formulations.

- Object-Oriented Supremacy: There is no point in portfolio optimization unless it can be practically applied to real asset matrices easily. The Facade pattern rules.

- Robustness: Extensively guarded against arrays of

NaNfragments and disjointed dimensions.

🚀 Installation

Using pip

The primary stable architecture.

pip install nexus-quant

For institutional scaling (which enforces CVXPY tensor integrations; optimally paired with a local MOSEK license instance):

pip install "nexus-quant[enterprise]"

From source

Clone the repository, navigate to the folder, and install directly using pip:

git clone https://github.com/Anagatam/Nexus.git

cd Nexus

pip install -e .

Testing & Developer Setup

Tests are written natively in pytest utilizing deterministic NumPy architectures to completely bypass yfinance REST rate limits.

Run the native Makefile to instantly configure the repository for contributing:

make install

make format

make test

License

Nexus is distributed freely under the standard MIT License. Open-source rules quantitative finance.

Disclaimer: Nothing about this project constitutes investment advice, and the author bears no responsibility for your subsequent investment decisions. Please rigorously validate all models statistically in out-of-sample data before committing live capital.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file nexus_quant-2.0.1.tar.gz.

File metadata

- Download URL: nexus_quant-2.0.1.tar.gz

- Upload date:

- Size: 20.0 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.13.5

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

dd3117b100415faba2a183476b70c64421e3d232bb88cb342af91dd19b537583

|

|

| MD5 |

66f865506cfa32382c9f3ff3ba23056b

|

|

| BLAKE2b-256 |

3aabc7d04c3b4039202bdeda514c55c788cffd9ff63bb32365f5ad00f7348038

|

File details

Details for the file nexus_quant-2.0.1-py3-none-any.whl.

File metadata

- Download URL: nexus_quant-2.0.1-py3-none-any.whl

- Upload date:

- Size: 15.6 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.13.5

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

3ca9a09bb31ef4d2ec82ae79f78f30902a28cf2975a37b5beb4fbb721a454903

|

|

| MD5 |

796fe7db7faa00092248ab3482b741e0

|

|

| BLAKE2b-256 |

dc5aa802229b60cf7966746384a11c83ba4b201f9253e5e23a0a3c56bbc011fe

|