Lightweight crypto portfolio optimizer. Efficient frontier, HRP, Risk Parity — with real risk metrics and interactive charts.

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Project description

Lightweight, open-source crypto portfolio optimizer.

10 optimization strategies, 8 risk metrics, AI-powered views, DeFi yields, sentiment analysis — all from a single CLI or interactive dashboard.

Installation • Who Is This For • Quick Start • Dashboard • Strategies • Features • Python API

Why Orbiter?

Most portfolio optimization tools are built for equities. Crypto is different — 24/7 markets, extreme volatility, fat-tailed returns, and correlations that spike during crashes. Orbiter is built specifically for this.

- Fast — Real optimization (not brute-force), results in seconds

- Honest — Walk-forward backtesting to avoid overfitting

- Practical — CLI for quick analysis, dashboard for exploration, Python API for integration

- Comprehensive — From basic mean-variance to regime detection and factor models

Who Is This For

Individual Investors & Traders

You hold multiple crypto assets and want to know the optimal allocation — not just gut feeling, but mathematically optimized weights based on real risk-return tradeoffs. Orbiter tells you exactly how much to put in each coin, shows you the efficient frontier, and validates the strategy with out-of-sample backtesting so you're not just curve-fitting to the past.

What you get:

- Run

orbiter optimize BTC ETH SOL AVAXand get an allocation in seconds - See how your portfolio would have performed with walk-forward backtesting

- Understand your actual risk exposure — max drawdown, CVaR, tail risk

- Compare 7 different strategies side-by-side to find what fits your risk tolerance

Quantitative Researchers & Students

You're studying portfolio theory, crypto markets, or quantitative finance and need a clean, well-tested codebase to experiment with. Every module is independent, documented, and covered by tests.

What you get:

- Factor model with market, momentum, size, and liquidity factors for crypto

- Regime detection (HMM) to study bull/bear/sideways market dynamics

- Monte Carlo stress testing with fat-tailed (Student-t) distributions

- Efficient frontier computation, correlation analysis, covariance estimation

- All code is modular — import just the pieces you need into your own research

Developers & Bot Builders

You're building a trading system, a portfolio dashboard, or an automated rebalancing bot. Orbiter gives you a clean Python API to plug into your stack.

What you get:

pip install orbiter-cryptoand import directly — no API keys needed for price data- Programmatic access to all strategies, metrics, and stress tests

- Rebalancing simulation with transaction cost modeling (maker/taker fees, slippage)

- Calendar, threshold, or hybrid rebalancing triggers

- Works with any exchange supported by ccxt (Binance, Bybit, Kraken, OKX, etc.)

Portfolio Managers & Analysts

You manage crypto allocations for clients or a fund and need institutional-grade analytics without paying for Bloomberg PORT.

What you get:

- Ledoit-Wolf shrinkage covariance — the same estimator used by institutional quant desks

- Risk parity and HRP — strategies used by Bridgewater and other systematic funds

- Correlation stress testing — see how your diversification breaks down during crashes

- Factor decomposition — understand what's driving your portfolio returns

- Interactive Streamlit dashboard for client presentations and exploration

Installation

pip install orbiter-crypto

With the interactive dashboard:

pip install orbiter-crypto[dashboard]

Or install from source:

git clone https://github.com/borghei/orbiter.git

cd orbiter

pip install -e ".[dashboard]"

Quick Start

CLI

# Find the optimal allocation for a portfolio

orbiter optimize BTC ETH SOL AVAX --strategy max-sharpe

# Try different strategies

orbiter optimize BTC ETH SOL AVAX BNB --strategy hrp

orbiter optimize BTC ETH SOL --strategy risk-parity

# Regime-aware: auto-detects bull/bear/sideways and picks the best strategy

orbiter optimize BTC ETH SOL AVAX --strategy regime-aware

# Walk-forward backtest with out-of-sample validation

orbiter backtest BTC ETH SOL AVAX --strategy hrp --train-days 180 --test-days 30

# Stress test your portfolio (Monte Carlo + correlation stress)

orbiter stress BTC ETH SOL AVAX --distribution student-t --horizon 30

# Discover top coins by market cap

orbiter discover --top 30

# Launch the interactive dashboard

orbiter dashboard

Example Output

Strategy: Hierarchical Risk Parity

Optimal Allocation

┏━━━━━━━┳━━━━━━━━┳━━━━━━━━━━━━━━━━━━━━━━━┓

┃ Asset ┃ Weight ┃ ┃

┡━━━━━━━╇━━━━━━━━╇━━━━━━━━━━━━━━━━━━━━━━━┩

│ BTC │ 53.3% │ █████████████████████ │

│ ETH │ 17.0% │ ██████ │

│ SOL │ 15.5% │ ██████ │

│ AVAX │ 14.2% │ █████ │

└───────┴────────┴───────────────────────┘

Portfolio Metrics

┏━━━━━━━━━━━━━━━━━┳━━━━━━━━┓

┃ Metric ┃ Value ┃

┡━━━━━━━━━━━━━━━━━╇━━━━━━━━┩

│ Ann. Return │ -18.8% │

│ Ann. Volatility │ 56.7% │

│ Sharpe Ratio │ -0.33 │

│ Sortino Ratio │ -0.46 │

│ Max Drawdown │ -58.4% │

│ Calmar Ratio │ -0.32 │

│ CVaR (95%) │ -6.72% │

│ Omega Ratio │ 0.95 │

└─────────────────┴────────┘

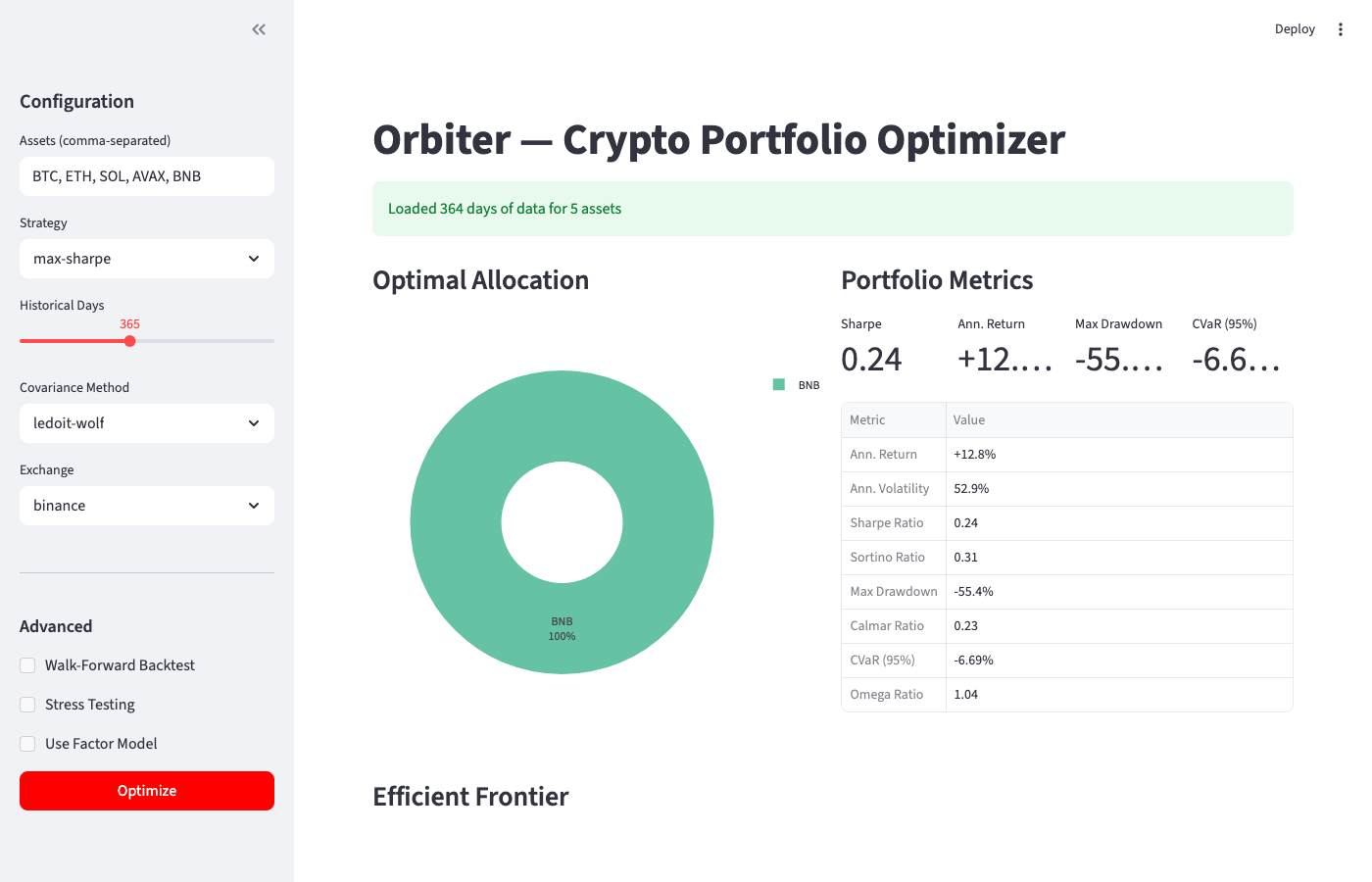

Dashboard

Launch with orbiter dashboard and open http://localhost:8501.

The dashboard provides:

- Sidebar configuration — pick assets, strategy, covariance method, exchange, lookback period

- Allocation pie chart — see how your portfolio is weighted

- Metrics overview — Sharpe, return, drawdown, CVaR at a glance

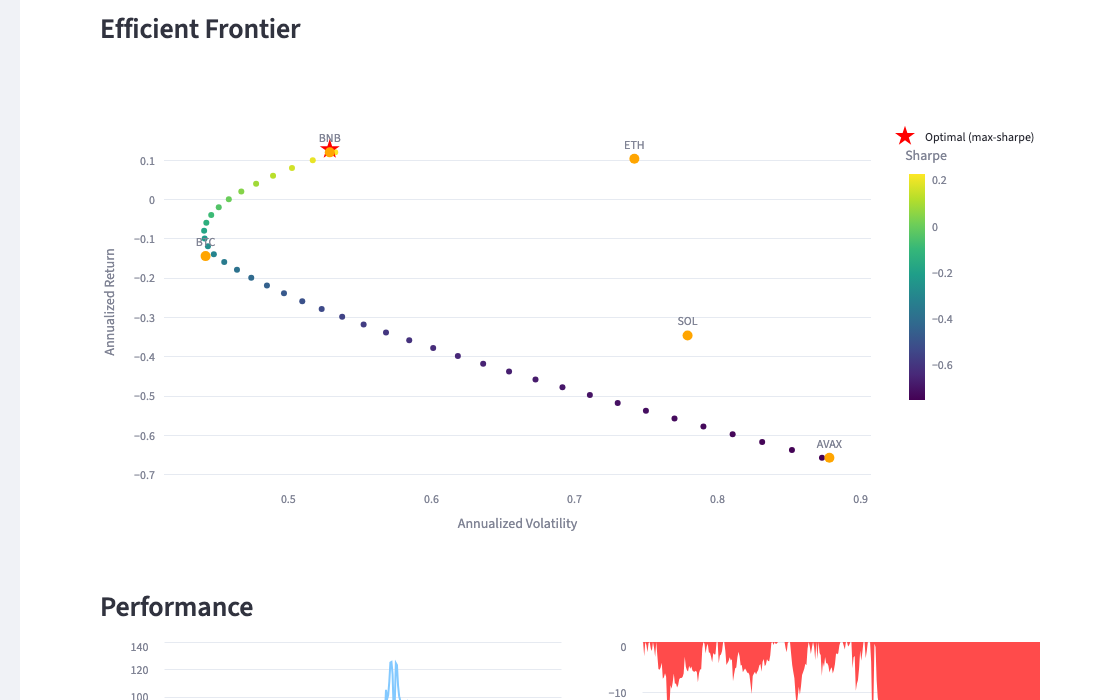

- Efficient frontier — interactive scatter plot showing the risk-return tradeoff

- Performance chart — cumulative returns vs equal-weight benchmark

- Drawdown chart — visualize peak-to-trough declines

- Correlation heatmap — understand how your assets move together

Toggle advanced features in the sidebar:

- Walk-Forward Backtest — out-of-sample validation with weight history

- Stress Testing — Monte Carlo VaR/CVaR + correlation stress

- Factor Model — factor loadings heatmap and R-squared per asset

Strategies

| Strategy | Description | Best For |

|---|---|---|

max-sharpe |

Maximize risk-adjusted return (Sharpe ratio) | Aggressive growth |

min-vol |

Minimize portfolio volatility | Capital preservation |

min-cvar |

Minimize tail risk (Conditional Value-at-Risk) | Downside protection |

risk-parity |

Equal risk contribution from each asset | Balanced exposure |

hrp |

Hierarchical Risk Parity — correlation-based, no return estimates | Robust diversification |

regime-aware |

HMM detects bull/bear/sideways, auto-switches strategy | Adaptive allocation |

factor-max-sharpe |

Max Sharpe using factor-model implied returns | Data-driven views |

black-litterman |

Black-Litterman model with investor views (manual or AI-generated) | Subjective + quantitative |

sentiment-regime |

HMM + Fear & Greed, funding rates, exchange flows | Early regime detection |

yield-adjusted |

Max Sharpe with DeFi staking/lending yields factored in | Yield-aware allocation |

Features

Risk Metrics

Every optimization returns 8 risk metrics:

| Metric | Description |

|---|---|

| Annualized Return | Geometric mean return, annualized to 365 days |

| Annualized Volatility | Standard deviation of returns, annualized |

| Sharpe Ratio | Return per unit of risk |

| Sortino Ratio | Return per unit of downside risk |

| Max Drawdown | Largest peak-to-trough decline |

| Calmar Ratio | Return divided by max drawdown |

| CVaR (95%) | Expected loss in the worst 5% of scenarios |

| Omega Ratio | Probability-weighted gains over losses |

Covariance Estimation

| Method | Description |

|---|---|

ledoit-wolf |

Shrinkage estimator — default, most robust for small samples |

sample |

Standard sample covariance |

exponential |

Exponentially weighted — gives more weight to recent data |

Walk-Forward Backtesting

Prevents overfitting by separating training and testing periods:

orbiter backtest BTC ETH SOL AVAX --strategy hrp --train-days 180 --test-days 30

- Train on 180 days of data → find optimal weights

- Test those weights on the next 30 days (out-of-sample)

- Slide forward, repeat

- Report aggregated out-of-sample performance vs equal-weight benchmark

Stress Testing

orbiter stress BTC ETH SOL AVAX --distribution student-t --horizon 30 --corr-stress 2.0

- Monte Carlo simulation — 10,000 paths with normal or Student-t (fat-tailed) distributions

- VaR & CVaR — at 95% and 99% confidence levels

- Correlation stress — see how portfolio risk increases when correlations spike (as they do during crashes)

Regime Detection

Hidden Markov Model identifies three market states:

| Regime | Characteristics | Strategy Used |

|---|---|---|

| Bull | Positive drift, moderate volatility | max-sharpe |

| Sideways | No clear direction, low volatility | risk-parity |

| Bear | Negative drift, high volatility | min-vol |

orbiter optimize BTC ETH SOL AVAX --strategy regime-aware

Factor Model

Crypto-specific four-factor model:

- Market — overall market return (equal or cap-weighted)

- Momentum — long recent winners, short recent losers

- Size — small-cap minus large-cap returns

- Liquidity — high-volume minus low-volume returns

orbiter optimize BTC ETH SOL AVAX --strategy factor-max-sharpe --use-factors

Black-Litterman with AI Views

Combine market equilibrium with your own views — or let AI generate them:

from orbiter import BlackLitterman, View, get_ai

from orbiter.prompts import MARKET_VIEWS_SYSTEM, market_views_prompt

from orbiter.black_litterman import parse_ai_views

# Manual views

views = [

View(asset="SOL", return_view=0.30, confidence=0.7),

View(asset=("ETH", "BTC"), return_view=0.05, confidence=0.6),

]

bl = BlackLitterman(returns)

result = bl.optimize(views)

# Or generate views with AI (Claude, OpenAI, or Perplexity)

ai = get_ai("claude") # reads ANTHROPIC_API_KEY from env

response = ai.generate(MARKET_VIEWS_SYSTEM, market_views_prompt(...))

views = parse_ai_views(response, assets=["BTC", "ETH", "SOL"])

result = bl.optimize(views)

Supports three AI providers with a single middleware:

| Provider | Model | Env Variable |

|---|---|---|

| Claude | claude-sonnet-4-20250514 |

ANTHROPIC_API_KEY |

| OpenAI | gpt-4o |

OPENAI_API_KEY |

| Perplexity | sonar-pro |

PERPLEXITY_API_KEY |

pip install orbiter-crypto[ai] # installs anthropic + openai SDKs

Sentiment-Enhanced Regime Detection

Goes beyond price-only HMM by fusing multiple sentiment signals:

- Fear & Greed Index — free API, updated daily

- Funding rates — crowded leverage detection from perpetual futures

- Exchange net flows — coins moving to exchanges = selling pressure

from orbiter import SentimentCollector

from orbiter.regime import SentimentRegimeModel

collector = SentimentCollector(exchange="binance")

sentiment = collector.collect(["BTC", "ETH", "SOL"])

model = SentimentRegimeModel(n_regimes=3)

model.fit(market_returns, sentiment_features_df)

regime = model.current_regime(market_returns, sentiment_features_df)

DeFi Yield-Adjusted Optimization

Staking ETH at 3.5% APY changes the efficient frontier. Orbiter accounts for this:

from orbiter import YieldCollector

from orbiter.defi import adjust_expected_returns

yields = YieldCollector().collect(["ETH", "SOL", "ATOM"])

adjusted_mu = adjust_expected_returns(daily_returns.mean(), yields)

- Pulls live yields from DeFiLlama (7000+ protocols)

- Falls back to conservative manual estimates if API is down

- Includes yield reliability scoring (higher APY = more smart contract risk)

Transaction Cost Modeling

Built-in fee and slippage models for realistic simulations:

- Maker/taker exchange fees

- Bid-ask spread costs

- Almgren-Chriss square-root market impact model

Rebalancing Simulation

Three rebalancing triggers:

| Trigger | Description |

|---|---|

calendar |

Rebalance every N days |

threshold |

Rebalance when any weight drifts beyond a threshold |

hybrid |

Threshold check on a calendar schedule |

Coin Discovery

orbiter discover --top 20 --min-mcap 1000000000

Fetches top coins from CoinGecko by market cap, with price and volume data.

Python API

Basic Optimization

from orbiter import PriceLoader, PortfolioOptimizer

loader = PriceLoader(exchange="binance")

returns = loader.get_returns(["BTC", "ETH", "SOL", "AVAX"], days=365)

optimizer = PortfolioOptimizer(returns, cov_method="ledoit-wolf")

result = optimizer.optimize("max-sharpe")

print(result.weights)

print(result.metrics)

Efficient Frontier

frontier = optimizer.efficient_frontier(n_points=50)

# DataFrame with columns: return, volatility, sharpe, BTC, ETH, SOL, AVAX

Walk-Forward Backtest

from orbiter.backtest import WalkForwardBacktest

bt = WalkForwardBacktest(returns, train_days=180, test_days=30, strategy="hrp")

result = bt.run()

print(result.metrics) # Out-of-sample performance

print(result.weights_history) # Weights at each rebalance

Stress Testing

from orbiter.stress import monte_carlo_stress, correlation_stress

# Monte Carlo with fat tails

mc = monte_carlo_stress(

weights=result.weights.values,

mu=returns.mean().values,

cov=returns.cov().values,

distribution="student-t",

df=5.0,

horizon_days=30,

)

print(mc["cvar_95"], mc["var_99"])

# Correlation stress

cs = correlation_stress(weights, cov_matrix, stress_factor=2.0)

print(cs["stressed_volatility"])

Factor Model

from orbiter.factors import CryptoFactorModel

model = CryptoFactorModel(returns)

exposures = model.fit()

print(exposures.loadings) # Factor betas per asset

print(exposures.r_squared) # Model fit per asset

print(model.expected_returns()) # Factor-implied expected returns

Regime Detection

from orbiter.regime import RegimeModel

model = RegimeModel(n_regimes=3)

model.fit(returns["BTC"])

regime = model.current_regime(returns["BTC"])

print(regime) # Regime.BULL, Regime.SIDEWAYS, or Regime.BEAR

print(model.get_strategy(regime))

Rebalancing Simulation

from orbiter.rebalance import simulate_rebalancing, RebalanceConfig, RebalanceTrigger

from orbiter.costs import FeeSchedule

config = RebalanceConfig(

trigger=RebalanceTrigger.THRESHOLD,

drift_threshold=0.05,

fee_schedule=FeeSchedule(maker=0.001, taker=0.001),

)

result = simulate_rebalancing(returns, target_weights, config)

print(result.total_turnover)

print(result.total_cost)

print(result.metrics)

Data Sources

| Source | Data | API Key |

|---|---|---|

| Binance (via ccxt) | OHLCV price data | Not required |

| Any ccxt exchange | OHLCV price data | Not required |

| CoinGecko | Market caps, coin discovery | Not required (free tier) |

| Blockchain.com | BTC active addresses, NVT ratio | Not required |

Change the exchange:

orbiter optimize BTC ETH SOL --exchange kraken

orbiter optimize BTC ETH SOL --exchange bybit

CLI Reference

| Command | Description |

|---|---|

orbiter optimize SYMBOLS... |

Optimize portfolio allocation |

orbiter backtest SYMBOLS... |

Walk-forward backtest |

orbiter stress SYMBOLS... |

Monte Carlo + correlation stress test |

orbiter discover |

List top coins by market cap |

orbiter dashboard |

Launch Streamlit dashboard |

Run orbiter COMMAND --help for full options.

Architecture

src/orbiter/

├── data.py # Price fetching via ccxt

├── data_sources.py # CoinGecko, on-chain metrics

├── metrics.py # Risk & performance metrics

├── covariance.py # Covariance estimation (sample, Ledoit-Wolf, exponential)

├── optimize.py # 10 optimization strategies + efficient frontier

├── backtest.py # Walk-forward backtesting engine

├── costs.py # Transaction cost & slippage modeling

├── rebalance.py # Rebalancing simulation (calendar/threshold/hybrid)

├── regime.py # HMM regime detection + sentiment-enhanced regime

├── stress.py # Monte Carlo & correlation stress testing

├── factors.py # Crypto factor model (market, momentum, size, liquidity)

├── black_litterman.py # Black-Litterman model with AI-generated views

├── ai.py # AI middleware (Claude, OpenAI, Perplexity adapters)

├── prompts.py # Prompt templates for AI-powered analysis

├── sentiment.py # Fear & Greed, funding rates, exchange flows

├── defi.py # DeFi yield data from DeFiLlama

├── cli.py # Click CLI

└── dashboard.py # Streamlit interactive dashboard

License

MIT + Commons Clause — Free to use in open-source projects, personal use, education, and internal business workflows. You cannot sell this software or repackage it as a paid product. See LICENSE for full terms.

Project details

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file orbiter_crypto-0.3.0.tar.gz.

File metadata

- Download URL: orbiter_crypto-0.3.0.tar.gz

- Upload date:

- Size: 601.6 kB

- Tags: Source

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d412f6d1ec28d9c8956363d93a4f7e8dd19d42b9a606a1278bddb7850b2182bd

|

|

| MD5 |

d9c6dcc50f41bb356c03abaa91093d5a

|

|

| BLAKE2b-256 |

8f68b4f957806bb0d4534889a9b61a5a133c5b66e5cbbe30c920ee9cbff9c52b

|

Provenance

The following attestation bundles were made for orbiter_crypto-0.3.0.tar.gz:

Publisher:

publish.yml on borghei/orbiter

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

orbiter_crypto-0.3.0.tar.gz -

Subject digest:

d412f6d1ec28d9c8956363d93a4f7e8dd19d42b9a606a1278bddb7850b2182bd - Sigstore transparency entry: 1091440201

- Sigstore integration time:

-

Permalink:

borghei/orbiter@9cab8d0ae348bb61aa98fcee592bc38c5ee42d70 -

Branch / Tag:

refs/tags/v0.3.0 - Owner: https://github.com/borghei

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

publish.yml@9cab8d0ae348bb61aa98fcee592bc38c5ee42d70 -

Trigger Event:

release

-

Statement type:

File details

Details for the file orbiter_crypto-0.3.0-py3-none-any.whl.

File metadata

- Download URL: orbiter_crypto-0.3.0-py3-none-any.whl

- Upload date:

- Size: 54.3 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

1515132e6841ee137c0ad83ab4ffcb587faab642e455e8a2b11bced0730c0aac

|

|

| MD5 |

1ec118f15634cb064bae454dbf9a6010

|

|

| BLAKE2b-256 |

af543ed75dc82680f007c010929c063cbf744320a5edc8775512256cee4c52db

|

Provenance

The following attestation bundles were made for orbiter_crypto-0.3.0-py3-none-any.whl:

Publisher:

publish.yml on borghei/orbiter

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

orbiter_crypto-0.3.0-py3-none-any.whl -

Subject digest:

1515132e6841ee137c0ad83ab4ffcb587faab642e455e8a2b11bced0730c0aac - Sigstore transparency entry: 1091440204

- Sigstore integration time:

-

Permalink:

borghei/orbiter@9cab8d0ae348bb61aa98fcee592bc38c5ee42d70 -

Branch / Tag:

refs/tags/v0.3.0 - Owner: https://github.com/borghei

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

publish.yml@9cab8d0ae348bb61aa98fcee592bc38c5ee42d70 -

Trigger Event:

release

-

Statement type: