Tool to help find an optimal portfolio allocation

Project description

Porfolio Finder

A Python library, based primarily around pandas, to identify an optimal portfolio allocation through back-testing.

API Documentation is available on Read the Docs.

Example Usage

Each of these examples make use of data.csv which provides returns for a handful of funds over 1970-2019.

Find best portfolio allocation to minimize the required timeframe to achieve a target value

from portfoliofinder import Allocations

Allocations(0.05, ['USA_TSM', 'WLDx_TSM', 'USA_INT', 'EM'])\

.filter('USA_TSM>=0.6 & WLDx_TSM<=0.2 & USA_INT>=0.3')\

.with_returns("data.csv")\

.with_regular_contributions(100000, 10000)\

.get_backtested_timeframes(target_value=1000000)\

.get_statistics(['min', 'max', 'mean', 'std'])\

.filter_by_min_of('max')\

.filter_by_max_of('min')\

.get_allocation_which_min_statistic('std')

Output

Statistic

min 14.000000

max 22.000000

mean 16.965517

std 2.809204

Name: Allocation(USA_TSM=0.65, WLDx_TSM=0.0, USA_INT=0.3, EM=0.05), dtype: float64

Find best portfolio allocation to maximize value with minimal risk over a fixed timeframe

from portfoliofinder import Allocations

Allocations(0.05, ['USA_TSM', 'WLDx_TSM', 'USA_INT', 'EM'])\

.filter('USA_TSM>=0.6 & WLDx_TSM<=0.2 & USA_INT>=0.3')\

.with_returns("data.csv")\

.with_regular_contributions(100000, 10000)\

.get_backtested_values(timeframe=10)\

.get_statistics(['mean', 'std'])\

.filter_by_gte_percentile_of(90, 'mean')\

.get_allocation_which_min_statistic('std')

Output

Statistic

mean 446560.590088

std 117448.007302

Name: Allocation(USA_TSM=0.6, WLDx_TSM=0.0, USA_INT=0.3, EM=0.1), dtype: float64

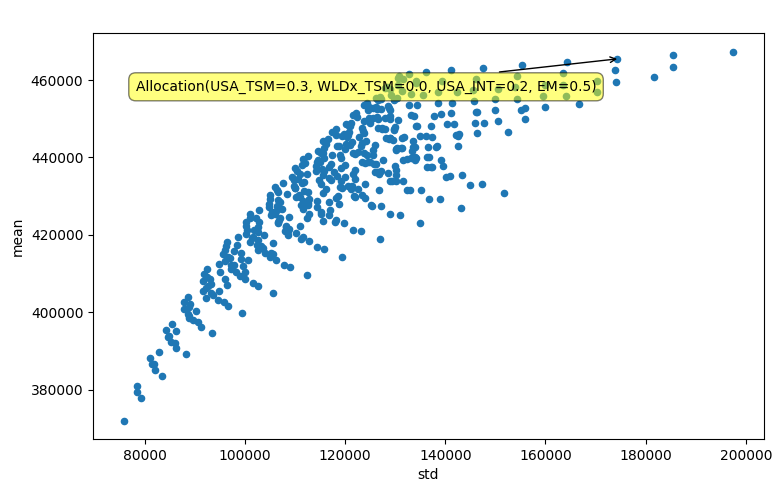

Graph statistics from multiple portfolio allocations to visualize their efficient frontier

from portfoliofinder import Allocations

Allocations(0.05, ['USA_TSM', 'WLDx_TSM', 'USA_INT', 'EM'])\

.filter('USA_TSM>=0.2 & USA_INT>=0.2')\

.with_returns("data.csv")\

.with_regular_contributions(100000, 10000)\

.get_backtested_values(timeframe=10)\

.get_statistics()\

.graph('std', 'mean')

Output

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file portfoliofinder-0.2.4.tar.gz.

File metadata

- Download URL: portfoliofinder-0.2.4.tar.gz

- Upload date:

- Size: 2.8 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/3.1.1 pkginfo/1.5.0.1 requests/2.24.0 setuptools/40.8.0 requests-toolbelt/0.9.1 tqdm/4.46.1 CPython/3.7.1

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

a2bc10be9a73d4a318a7d90f6dcfd61b407e3cb86a5ffa3ffc403ce31c4e5829

|

|

| MD5 |

8b634803e0494e5864f8e71ba6ccacb9

|

|

| BLAKE2b-256 |

b354868d2580a957bcbc8b67c69481c7575d1ccd3a538bceaf67d3385fb30af8

|

File details

Details for the file portfoliofinder-0.2.4-py3-none-any.whl.

File metadata

- Download URL: portfoliofinder-0.2.4-py3-none-any.whl

- Upload date:

- Size: 3.6 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/3.1.1 pkginfo/1.5.0.1 requests/2.24.0 setuptools/40.8.0 requests-toolbelt/0.9.1 tqdm/4.46.1 CPython/3.7.1

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

058237b9a8e9a4974fb071385c9778d1563a5f90d664451c24990b206f6096ce

|

|

| MD5 |

3c9dd5a9bdbf9c04537109d22964930f

|

|

| BLAKE2b-256 |

ae136a2fe037b07f96118cb8624b1b6259cb9f9f567e4f2b0985eb1b2b911f33

|