Extreme value models for applications in energy procurement

Project description

riskmodels: a library for univariate and bivariate extreme value analysis (and applications to energy procurement)

This library focuses on extreme value models for risk analysis in one and two dimensions. MLE-based and Bayesian generalised Pareto tail models are available for one-dimensional data, while for two-dimensional data, logistic and Gaussian (MLE-based) extremal dependence models are also available. Logistic models are appropriate for data whose extremal occurrences are strongly associated, while a Gaussian model offer an asymptotically independent, but still parametric, copula.

The powersys submodule offers utilities for applications in energy procurement, with functionality to model available conventional generation (ACG) as well as to calculate loss of load expectation (LOLE) and expected energy unserved (EEU) indices on a wide set of models; efficient parallel time series based simulation for univariate and bivariate power surpluses is also available.

Requirements

Python >= 3.7

Installation

pip install riskmodels

API docs

https://nestorsag.github.io/riskmodels/

Quickstart

Because this library grew from research in energy procurement, this example is related to that but the univariate and bivariate modules are quite general and can be applied to any kind of data. The following example analyses the co-occurrence of high demand net of renewables (this is, demand minus intermittent generation such as wind and solar) in Great Britain's and Denmark's power systems. This can be done to value interconnection in the context of security of supply analysis, for example.

Table of contents

Quickstart - extreme value modelling

Quickstart - energy procurement modelling

Getting the data

The data for this example corresponds roughly to peak (winter) season of 2017-2018, and is openly available online but has to be put together from different places, namely Energinet's API, renewables.ninja, and NGESO's website.

from urllib.request import Request, urlopen

import urllib.parse

import requests

from datetime import timedelta

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

def fetch_data() -> pd.DataFrame:

"""Fetch data from different sources to reconstruct demand net of wind time series

in Great Britain and Denmark.

Returns:

pd.DataFrame: Cleaned data

"""

def fetch_gb_data():

rn_prefix = "https://www.renewables.ninja/country_downloads"

wind_url = f"{rn_prefix}/GB/ninja_wind_country_GB_current-merra-2_corrected.csv"

wind_capacity = 13150

#

ngeso_prefix = "https://data.nationalgrideso.com/backend/dataset/8f2fe0af-871c-488d-8bad-960426f24601/resource"

demand_urls = [

f"{ngeso_prefix}/2f0f75b8-39c5-46ff-a914-ae38088ed022/download/demanddata_2017.csv",

f"{ngeso_prefix}/fcb12133-0db0-4f27-a4a5-1669fd9f6d33/download/demanddata_2018.csv"]

proxy_header = 'Mozilla/5.0 (X11; Ubuntu; Linux x86_64; rv:77.0) Gecko/20100101 Firefox/77.0'

#

# function to retrieve reconstructed wind data

def fetch_wind_data() -> pd.DataFrame:

"""Fetches historic wind generation data reconstructed from atmospheric models

Returns:

pd.DataFrame: wind data

"""

print("Fetching GB's wind data..")

req = Request(wind_url)

req.add_header('User-Agent', proxy_header)

content = urlopen(req)

raw = pd.read_csv(content, header=None)

df = pd.DataFrame(np.array(raw.iloc[3::,:]), columns = list(raw.iloc[2,:]))

df["wind_generation"] = wind_capacity * df["national"].astype(np.float32)

df["time"] = pd.to_datetime(df["time"], utc=True)

return df.drop(labels=["national", "offshore", "onshore"], axis=1)

#

def fetch_demand_data() -> pd.DataFrame:

"""Fetches public demand data for 2017-2018 from NGESO's website

Returns:

pd.DataFrame: net demand data

"""

print("Fetching GB's demand data..")

# fetch data from website

demand_df = pd.concat([pd.read_csv(url) for url in demand_urls])

# format time columns

demand_df["date"] = (pd.to_datetime(demand_df["SETTLEMENT_DATE"]

.astype(str)

.str.lower(), utc=True))

timedeltas = [timedelta(days=max((x-1),0.1)/48) for x in demand_df["SETTLEMENT_PERIOD"]]

demand_df["time"] = (demand_df["date"]

+ pd.to_timedelta(timedeltas))

demand_df["demand"] = demand_df["ND"]

return demand_df.filter(items=["time","demand"], axis=1)

#

# merge wind and demand and filter peak season of 2017-2018

df = fetch_demand_data().merge(fetch_wind_data(), on="time")

#

df["net_demand"] = df["demand"] - df["wind_generation"]

#

return df.filter(items=["time", "net_demand"], axis=1)

def fetch_dk_data() -> pd.DataFrame:

"""Fetches data for 2017-2018 from the Danish system operator's public API

Returns:

pd.DataFrame: net demand data

"""

print("Fetching DK's data..")

api_url = 'https://data-api.energidataservice.dk/v1/graphql'

headers = {'content-type': 'application/json'}

query = """

{

electricitybalancenonv(where:{HourUTC:{_gte:\"2017-11-01\"}}, limit: 10000) {

HourUTC

TotalLoad

SolarPower

OnshoreWindPower

OffshoreWindPower

}

}

"""

request = requests.post(api_url, json={'query': query}, headers=headers)

dk_df = pd.DataFrame(request.json()["data"]["electricitybalancenonv"]).dropna(axis=0)

dk_df["time"] = pd.to_datetime(dk_df["HourUTC"], utc=True)

dk_df["net_demand"] = (dk_df["TotalLoad"]

- dk_df["SolarPower"]

- dk_df["OnshoreWindPower"]

- dk_df["OffshoreWindPower"])

return dk_df.filter(items=["time","net_demand"], axis=1)

#

gb_df = fetch_gb_data()

dk_df = fetch_dk_data()

# leave only peak winter season

query_str = "(time.dt.month >= 11 and time.dt.year == 2017) or (time.dt.month <=3 and time.dt.year == 2018)"

df = gb_df.merge(dk_df, on="time", suffixes=("_gb", "_dk")).query(query_str)

return df

# fetch data from public APIs

df = fetch_data()

Univariate extreme value modelling

Empirical distributions are the base on which the package operates, and the Empirical classes in both univariate and bivariate modules provide the main entrypoints.

import riskmodels.univariate as univar

import riskmodels.bivariate as bivar

# prepare data

gb_nd, dk_nd = np.array(df["net_demand_gb"]), np.array(df["net_demand_dk"])

# Initialise Empirical distribution objects. Round observations to nearest MW

# this will come n handy for energy procurement modelling, and does not affect fitted tail models

gb_nd_dist, dk_nd_dist = (univar.Empirical.from_data(gb_nd).to_integer(),

univar.Empirical.from_data(dk_nd).to_integer())

#look at mean residual life to decide whether threshold values are appropriate

q_th = 0.95

gb_nd_dist.plot_mean_residual_life(threshold = gb_nd_dist.ppf(q_th));plt.show()

dk_nd_dist.plot_mean_residual_life(threshold = dk_nd_dist.ppf(q_th));plt.show()

Mean residual life plot for GB at 95%

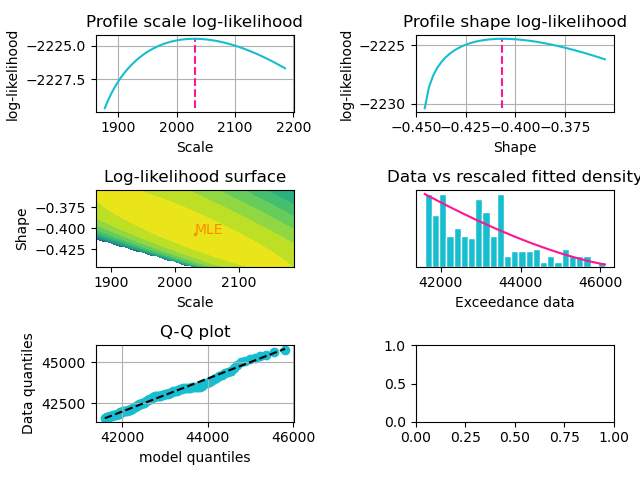

Once we confirm the threshold is appropriate, univariate generalised Pareto models can be fitted using fit_tai_model, and fit diagnostics can be displayed afterwards.

# Fit univariate models for both areas and plot diagnostics

gb_dist_ev = gb_nd_dist.fit_tail_model(threshold=gb_nd_dist.ppf(q_th))

gb_dist_ev.plot_diagnostics();plt.show()

dk_dist_ev = dk_nd_dist.fit_tail_model(threshold=dk_nd_dist.ppf(q_th))

dk_dist_ev.plot_diagnostics();plt.show()

The result is a semi-parametric model with an empirical distribution below the threshold and a generalised Pareto model above. Generated diagnostics for GB's tail models are shown below.

Diagnostic plots for GB model

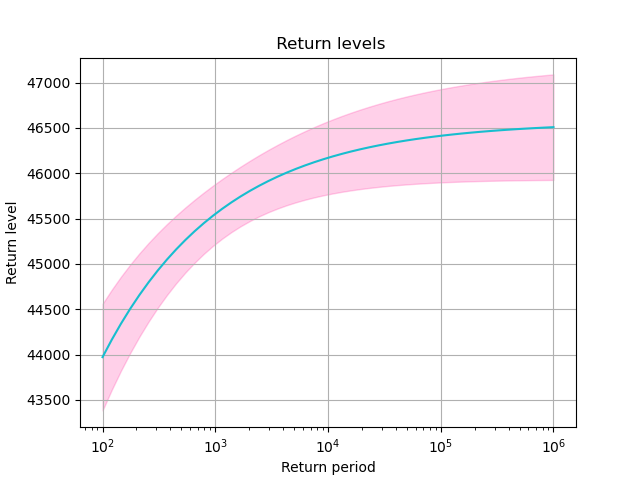

Return levels for GB

Bivariate extreme value modelling

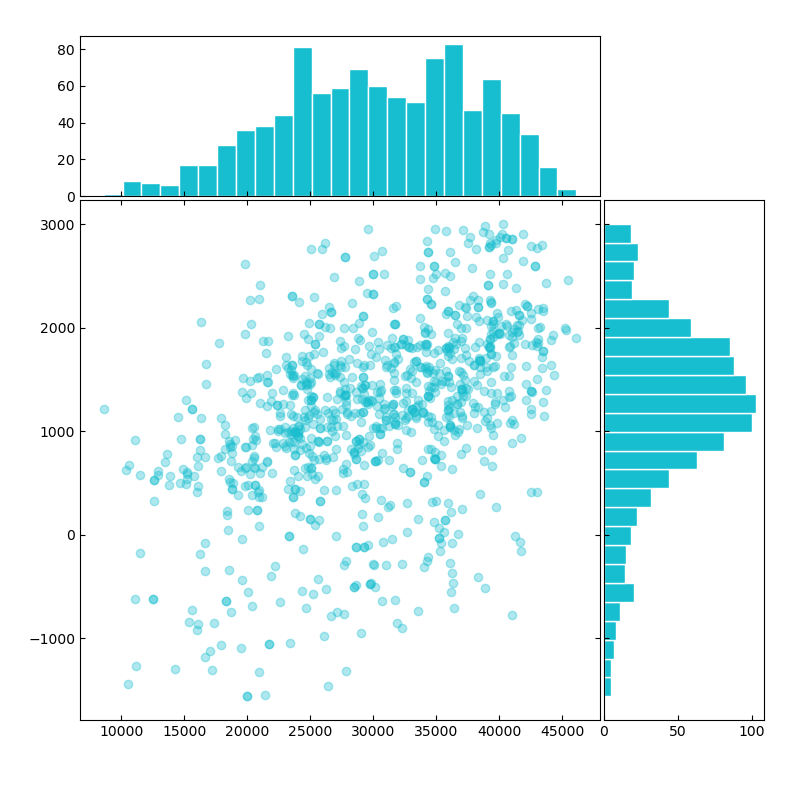

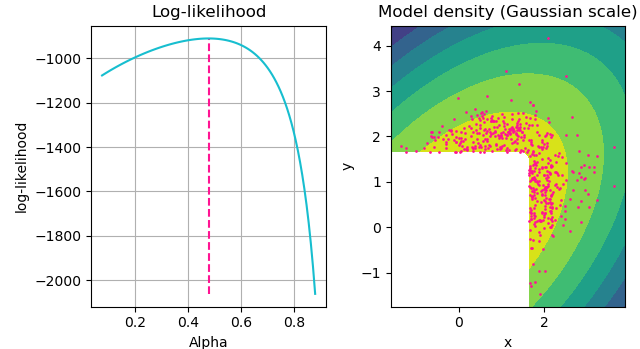

Bivariate EV models are built analogously to univariate models. When fitting a bivarate tail model there is a choice between assuming "strong" or "weak" association between extreme co-occurrences across components 1. The package implements a Bayesian factor test, shown below, to help justify this decision. In addition, marginal distributions can be passed to be used for quantile estimation in the fitting procedure.

Data sample scatterplot (x-axis: GB, y-axis: DK)

# set random seed

np.random.seed(1)

# instantiate bivariate empirical object with net demand from both areas

bivar_empirical = bivar.Empirical.from_data(np.stack([gb_nd, dk_nd], axis=1))

bivar_empirical.plot();plt.show()

# test for asymptotic dependence and fit corresponding model

r = bivar_empirical.test_asymptotic_dependence(q_th)

if r > 1: # r > 1 suggests strong association between extremes

model = "logistic"

else: # r <= 1 suggests weak association between extremes

model = "gaussian"

bivar_ev_model = bivar_empirical.fit_tail_model(

model = model,

quantile_threshold = q_th,

margin1 = gb_dist_ev,

margin2 = dk_dist_ev)

bivar_ev_model.plot_diagnostics();plt.show()

Bivariate model's diagnostics plots

Energy procurement modelling

For the sake of this example, synthetic conventional generator fleets are going to be created for both areas in order to compute risk indices for a hypothetical interconnected system.

from riskmodels.adequacy import acg_models

# get number of timesteps in peak season

n = len(gb_nd)

# assume a base fleet of 200 generators with 240 max. capacity and 4% breakdown rate

uk_gen_df = pd.DataFrame([{"capacity": 240, "availability": 0.96} for k in range(200)])

uk_gen = acg_models.NonSequential.from_generator_df(uk_gen_df)

# assume a base fleet of 55 generators with 61 max. capacity and 4% breakdown rate

dk_gen_df = pd.DataFrame([{"capacity": 61, "availability": 0.96} for k in range(55)])

dk_gen = acg_models.NonSequential.from_generator_df(dk_gen_df)

# define LOLE functon

def lole(gen, net_demand, n=n):

#Integer distributions can be convolved with other integer or continuous distributions through the + operator

return n*(1 - (-gen + net_demand).cdf(0))

# compute pre-interconnection LOLEs

lole(dk_gen, dk_dist_ev)

lole(uk_gen, gb_dist_ev)

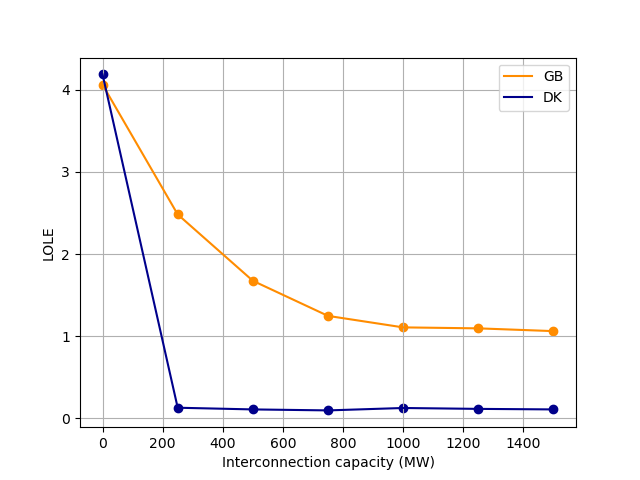

LOLE can be computed exactly for univariate surplus distributions as above, but post-interconnection LOLE requires Monte Carlo estimation. Below, post-interconnection LOLEs are computed for both areas for a range of interconnection capacities up to 1.5 GW.

bivariate_gen = bivar.Independent(x=uk_gen, y=dk_gen)

from riskmodels.adequacy.capacity_models import BivariateNSMonteCarlo

bivariate_surplus = BivariateNSMonteCarlo(

gen_distribution = bivariate_gen,

net_demand = bivar_ev_model,

season_length = n,

size = 5000000)

itc_caps = np.linspace(0, 1500, 7)

gb_post_itc_lole = np.array([bivariate_surplus.lole(area=0, itc_cap = itc_cap) for itc_cap in itc_caps])

dk_post_itc_lole = np.array([bivariate_surplus.lole(area=1, itc_cap = itc_cap) for itc_cap in itc_caps])

plt.plot(itc_caps, gb_post_itc_lole, color="darkorange", label = "GB")

plt.scatter(itc_caps, gb_post_itc_lole, color="darkorange")

plt.plot(itc_caps, dk_post_itc_lole, color="darkblue", label = "DK")

plt.scatter(itc_caps, dk_post_itc_lole, color="darkblue")

plt.xlabel("Interconnection capacity (MW)")

plt.ylabel("LOLE")

plt.grid()

plt.legend()

plt.show()

Post-interconnection LOLE indices

1: A more in-depth explanation of asymptotic dependence vs independence is given in 'Statistics of Extremes: Theory and Applications' by Beirlant et al, page 342.

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

File details

Details for the file riskmodels-2.3.0.tar.gz.

File metadata

- Download URL: riskmodels-2.3.0.tar.gz

- Upload date:

- Size: 107.3 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/4.0.2 CPython/3.9.17

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

b35f05941da15f08ede1c8cda0fb4afbed970c07783a4ef4146b5a2d7b946bac

|

|

| MD5 |

3d6d6aaf9a669f62fa081c19e55c8b44

|

|

| BLAKE2b-256 |

ac33f07dac1c0e22ef94471eee1fbb0561bd654e4482709146acfe3a0d674680

|