Risk-Neutral Density Estimation Tools

Project description

risk-neutral

Risk-Neutral Density Estimation Tools

A Python library for pricing options under various risk-neutral density assumptions, computing option-implied densities, and extracting model parameters from market data.

Features

- Option Pricers: Black–Scholes–Merton (BSM), Mixture of Log-Normals for American Options (AMLN), Edgeworth Expansion (EW), Shimko Spline Method, and Mixture of Log-Normals (MLN).

- Density Models: Compute risk-neutral probability density functions for priced assets under different distributional assumptions.

- Density Extraction: Calibrate density model parameters to market option prices via optimization (BSM, AM, EW, MLN) or direct implied-volatility inversion (Shimko).

- Utilities: Implied volatility computation (

compute_implied_vol), volatility-curve fitting (fit_iv_curve).

Installation

Simply

pip install riskneutral

or

pip install git+https://github.com/Moe-Dada/risk_neutral.git

Or clone and install locally:

git clone https://github.com/Moe-Dada/risk_neutral.git

cd risk_neutral

pip install .

Quickstart

Option Pricing

from riskneutral.core_pricing import MarketParams, BSMParams, BSMPricer

# Market parameters: spot, risk-free rate, dividend yield

data = MarketParams(s0=100.0, r=0.05, y=0.02)

# BSM parameters: strike, time to expiry, volatility

params = BSMParams(k=100.0, te=1.0, sigma=0.2)

pricer = BSMPricer(market=data, params=params)

prices = pricer.price()

print(prices) # {'d1': ..., 'd2': ..., 'call': ..., 'put': ...}

Switch pricer class for different models:

AMPricer(Mixture of Log-Normals for American Options)EWPricer(Edgeworth Expansion)ShimkoPricer(Shimko Spline Method)MLNPricer(Mixture of Log-Normals)

Density Computation

import numpy as np

from riskneutral.density_computations import EwDensity, EWParams, MarketParams

mp = MarketParams(s0=100.0, r=0.05, y=0.02)

params = EWParams(k=100.0, te=1.0, sigma=0.2, skew=0.0, kurt=3.0)

model = EwDensity(market=mp, params=params)

x = np.linspace(50, 150, 200)

pdf = model.pdf(x)

Other density classes:

ShimkoDensity(local-volatiltity skew)AmDensity(mixture-lognormal)MlnDensity(two-component lognormal mixture)

Density Extraction

import numpy as np

from riskneutral.density_extraction import DensityData, BsmDensityExtractor, BsmExtractConfig

from riskneutral.core_pricing import BSMPricer, BSMParams, MarketParams

# Simulate market option prices under BSM

r, y, te, s0, sigma = 0.03, 0.01, 0.5, 100.0, 0.25

strikes = np.array([90, 100, 110])

market_calls = np.array([

BSMPricer(MarketParams(s0, r, y), BSMParams(K, te, sigma)).price()["call"]

for K in strikes

])

data = DensityData(

r=r, y=y, te=te, s0=s0,

market_calls=market_calls,

call_strikes=strikes

)

extractor = BsmDensityExtractor(data, BsmExtractConfig(lam=0.0))

result = extractor.extract()

print("Estimated mu, zeta:", result.params)

For other extractors, see AmDensityExtractor, EwDensityExtractor, MlnDensityExtractor, or use ShimkoDirectExtractor for implied-volatility-based extraction.

Examples

- See the

examples/folder for complete scripts demonstrating pricing, density computation, and extraction workflows. - See

examples/examples_density_computations_and_plots.pyfor density plots.

For example:

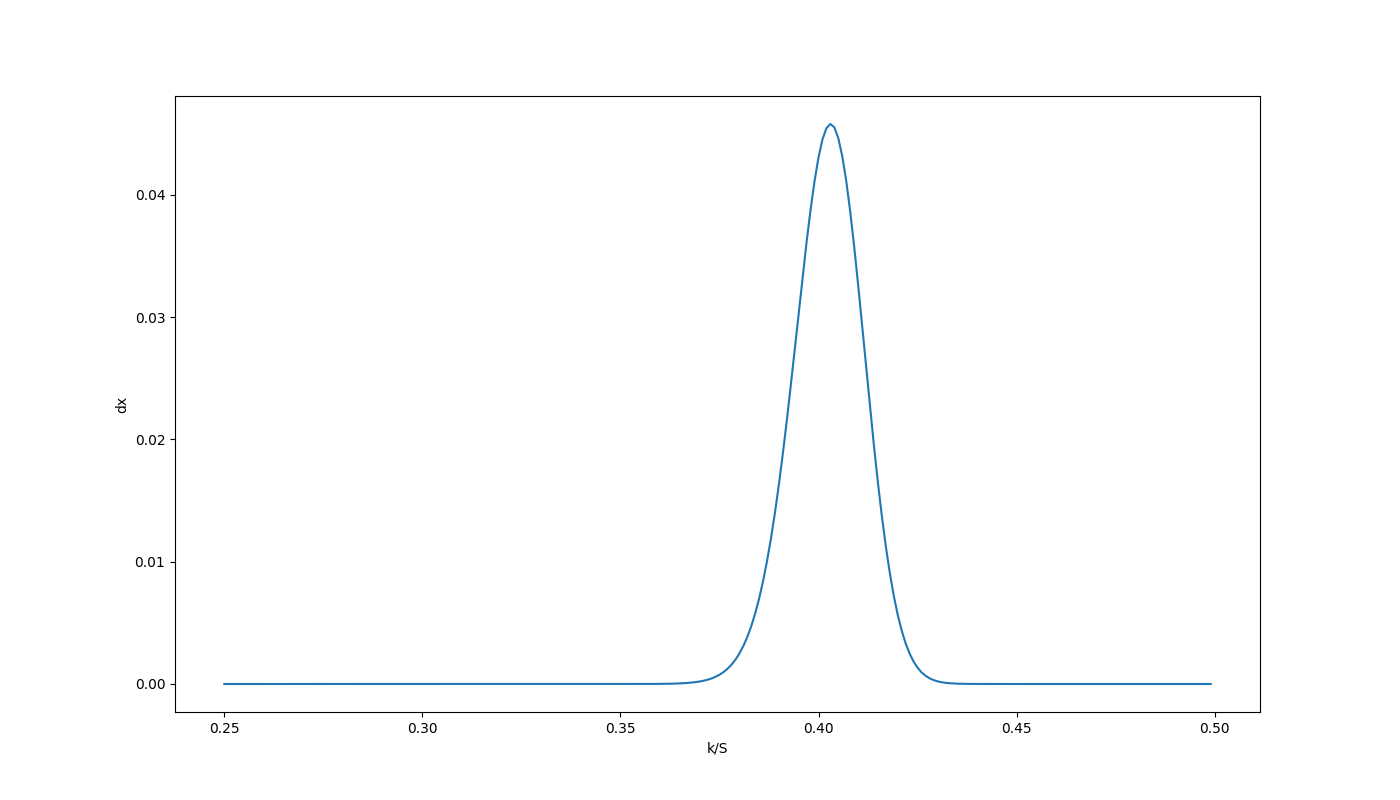

- Shimko's Spline Method:

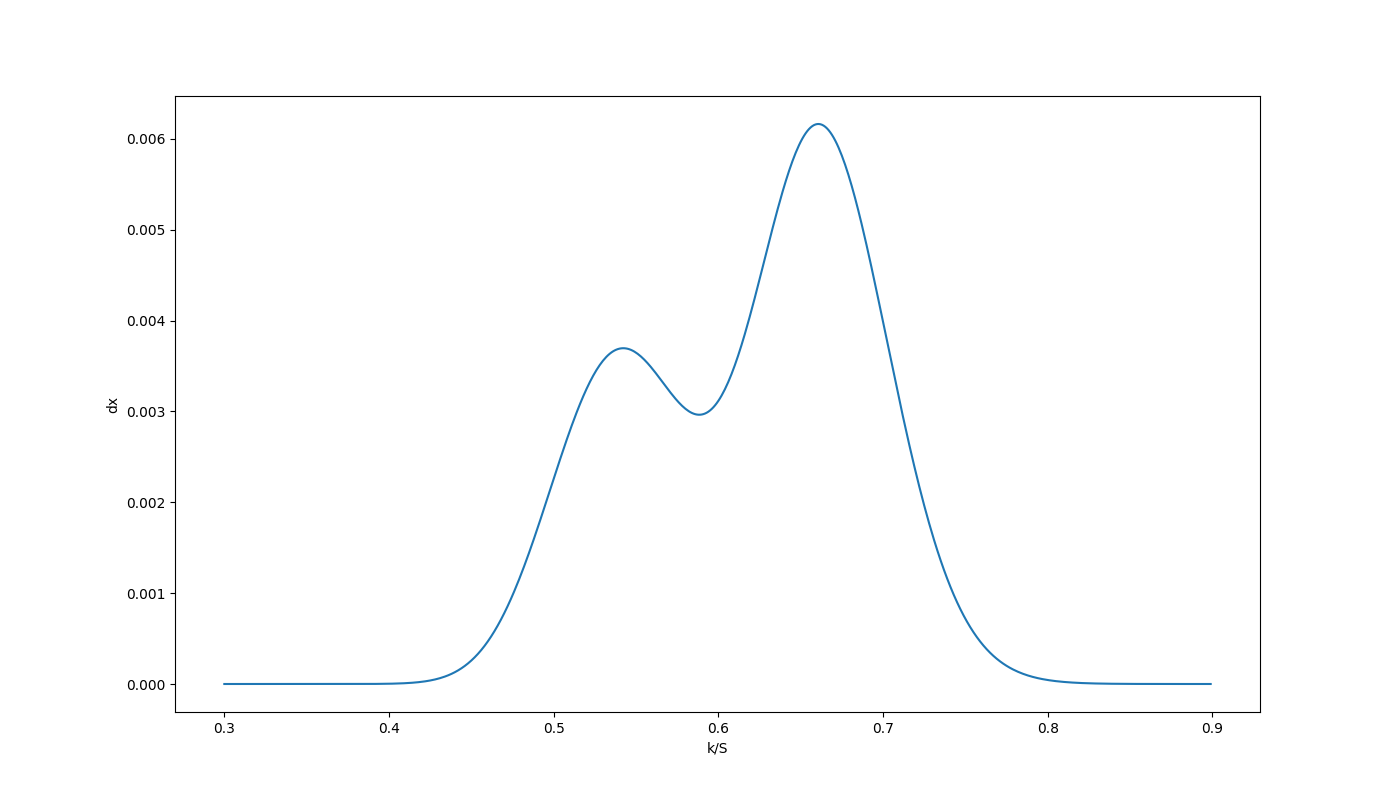

- Mixture of Log-Normals:

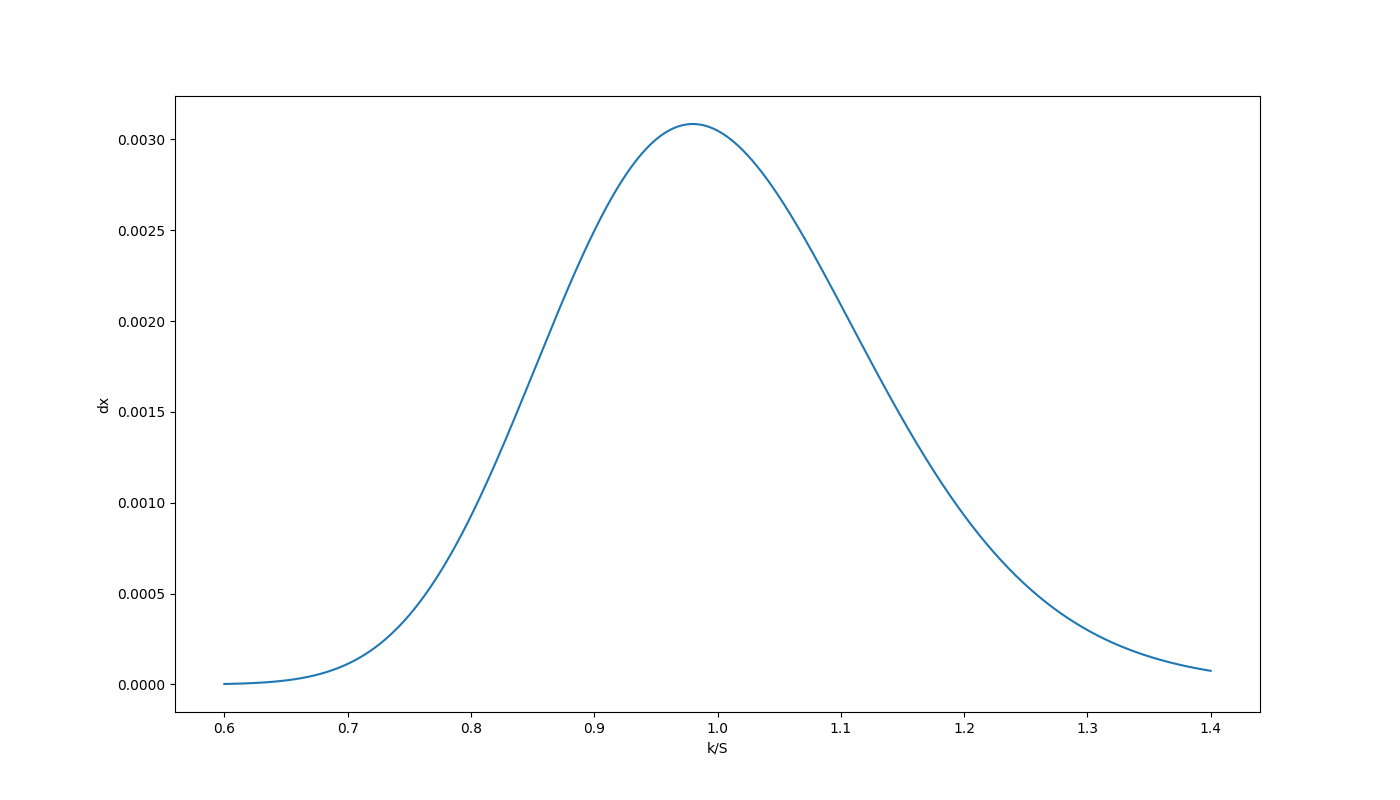

- Edgeworth's Expansion:

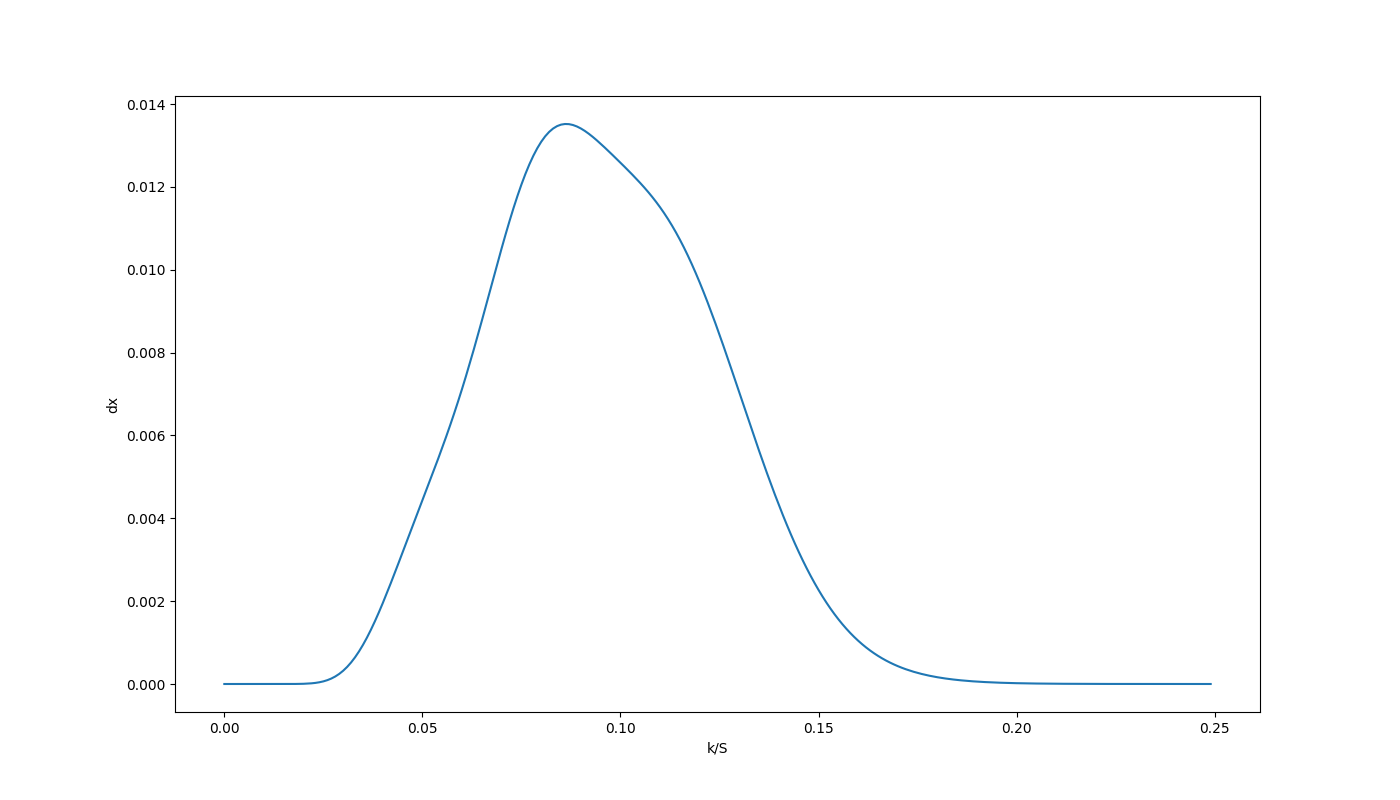

- Mixture of Log-Normals for American Option

Testing

Run the full test suite with:

pytest

Contributing

Contributions and issues are welcome! Please open an issue or submit a pull request on GitHub.

License

This project is licensed under the MIT License. See the LICENSE file for details.

References

- Prof. Kam Hamdieh @ [https://profiles.rice.edu/faculty/kam-hamidieh], Hamidieh, K., 2014. Estimating the tail shape parameter from option prices. Available at SSRN 1940117.

- Dada, Moses O (2025) Three essays on volatility and tail-risk. Doctoral thesis, University of Essex. DOI [https://doi.org/10.5526/ERR-00040865]

- E. Jondeau and S. Poon and M. Rockinger (2007): Financial Modeling Under Non-Gaussian Distributions Springer-Verlag, London

- R. Jarrow and A. Rudd (1982) Approximate valuation for arbitrary stochastic processes. Journal of Finanical Economics, 10, 347-369

- C.J. Corrado and T. Su (1996) S&P 500 index option tests of Jarrow and Rudd’s approximate option valuation formula. Journal of Futures Markets, 6, 611-629

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file riskneutral-0.1.1.tar.gz.

File metadata

- Download URL: riskneutral-0.1.1.tar.gz

- Upload date:

- Size: 3.6 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.10.14

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

7486d196e228217ebb71bd89601955b0317b3521918aac72acef66a8254b2823

|

|

| MD5 |

2037c6bfca0fa8e8be5861d10e65ab15

|

|

| BLAKE2b-256 |

58d3a9b82fe0e3527b3b88654b000da48af6cb1d0440175fabb6d50b59233e9d

|

File details

Details for the file riskneutral-0.1.1-py3-none-any.whl.

File metadata

- Download URL: riskneutral-0.1.1-py3-none-any.whl

- Upload date:

- Size: 3.5 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.10.14

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

816ad485363bcfb02529377ee066f07a751697098a5276f0dc5388f0803c559a

|

|

| MD5 |

5f780dead6aa410d4f29cf201d3298d6

|

|

| BLAKE2b-256 |

3832bbca830da0a20fc71d31728f77d24686b9a7773048ec33979bb29bd383c9

|