The RiskOptima toolkit is a comprehensive Python solution designed to assist investors in evaluating, managing, and optimizing the risk of their investment portfolios. This package implements advanced financial metrics and models to compute key risk indicators, including Value at Risk (VaR), Conditional Value at Risk (CVaR), and volatility assessment

Project description

RiskOptima

RiskOptima is a comprehensive Python toolkit for evaluating, managing, and optimizing investment portfolios. This package is designed to empower investors and data scientists by combining financial risk analysis, backtesting, mean-variance optimization, and machine learning capabilities into a single, cohesive package.

Stats

https://pypistats.org/packages/riskoptima

Key Features

- Portfolio Optimization: Includes mean-variance optimization, efficient frontier calculation, and maximum Sharpe ratio portfolio construction.

- Risk Management: Compute key financial risk metrics such as Value at Risk (VaR), Conditional Value at Risk (CVaR), volatility, and drawdowns.

- Backtesting Framework: Simulate historical performance of investment strategies and analyze portfolio dynamics over time.

- Machine Learning Integration: Future-ready for implementing machine learning models for predictive analytics and advanced portfolio insights.

- Monte Carlo Simulations: Perform extensive simulations to analyze potential portfolio outcomes. See example here https://github.com/JordiCorbilla/efficient-frontier-monte-carlo-portfolio-optimization

- Comprehensive Financial Metrics: Calculate returns, Sharpe ratios, covariance matrices, and more.

Installation

See the project here: https://pypi.org/project/riskoptima/

pip install riskoptima

Usage

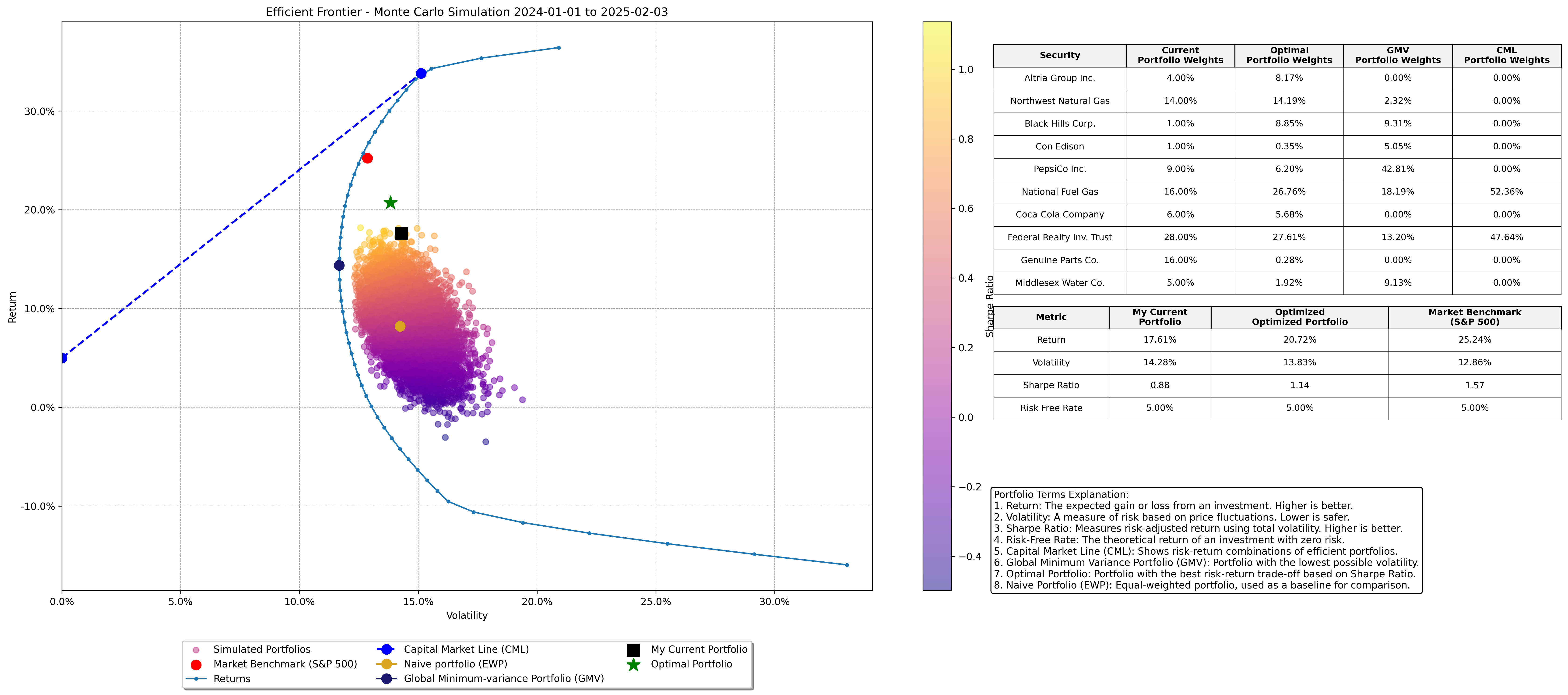

Example 1: Efficient Frontier - Monte Carlo Portfolio Optimization

import pandas as pd

from riskoptima import RiskOptima

# Define your current porfolio with your weights and company names

asset_data = [

{"Asset": "MO", "Weight": 0.04, "Label": "Altria Group Inc.", "MarketCap": 110.0e9},

{"Asset": "NWN", "Weight": 0.14, "Label": "Northwest Natural Gas", "MarketCap": 1.8e9},

{"Asset": "BKH", "Weight": 0.01, "Label": "Black Hills Corp.", "MarketCap": 4.5e9},

{"Asset": "ED", "Weight": 0.01, "Label": "Con Edison", "MarketCap": 30.0e9},

{"Asset": "PEP", "Weight": 0.09, "Label": "PepsiCo Inc.", "MarketCap": 255.0e9},

{"Asset": "NFG", "Weight": 0.16, "Label": "National Fuel Gas", "MarketCap": 5.6e9},

{"Asset": "KO", "Weight": 0.06, "Label": "Coca-Cola Company", "MarketCap": 275.0e9},

{"Asset": "FRT", "Weight": 0.28, "Label": "Federal Realty Inv. Trust", "MarketCap": 9.8e9},

{"Asset": "GPC", "Weight": 0.16, "Label": "Genuine Parts Co.", "MarketCap": 25.3e9},

{"Asset": "MSEX", "Weight": 0.05, "Label": "Middlesex Water Co.", "MarketCap": 2.4e9}

]

asset_table = pd.DataFrame(asset_data)

capital = 100_000

asset_table['Portfolio'] = asset_table['Weight'] * capital

start_date = '2024-01-01'

end_date = RiskOptima.get_previous_working_day()

RiskOptima.plot_efficient_frontier_monte_carlo(

asset_table,

start_date=start_date,

end_date=end_date,

risk_free_rate=0.05,

num_portfolios=10000,

market_benchmark='SPY',

set_ticks=False,

x_pos_table=1.15, # Position for the weight table on the plot

y_pos_table=0.52, # Position for the weight table on the plot

title=f'Efficient Frontier - Monte Carlo Simulation {start_date} to {end_date}'

)

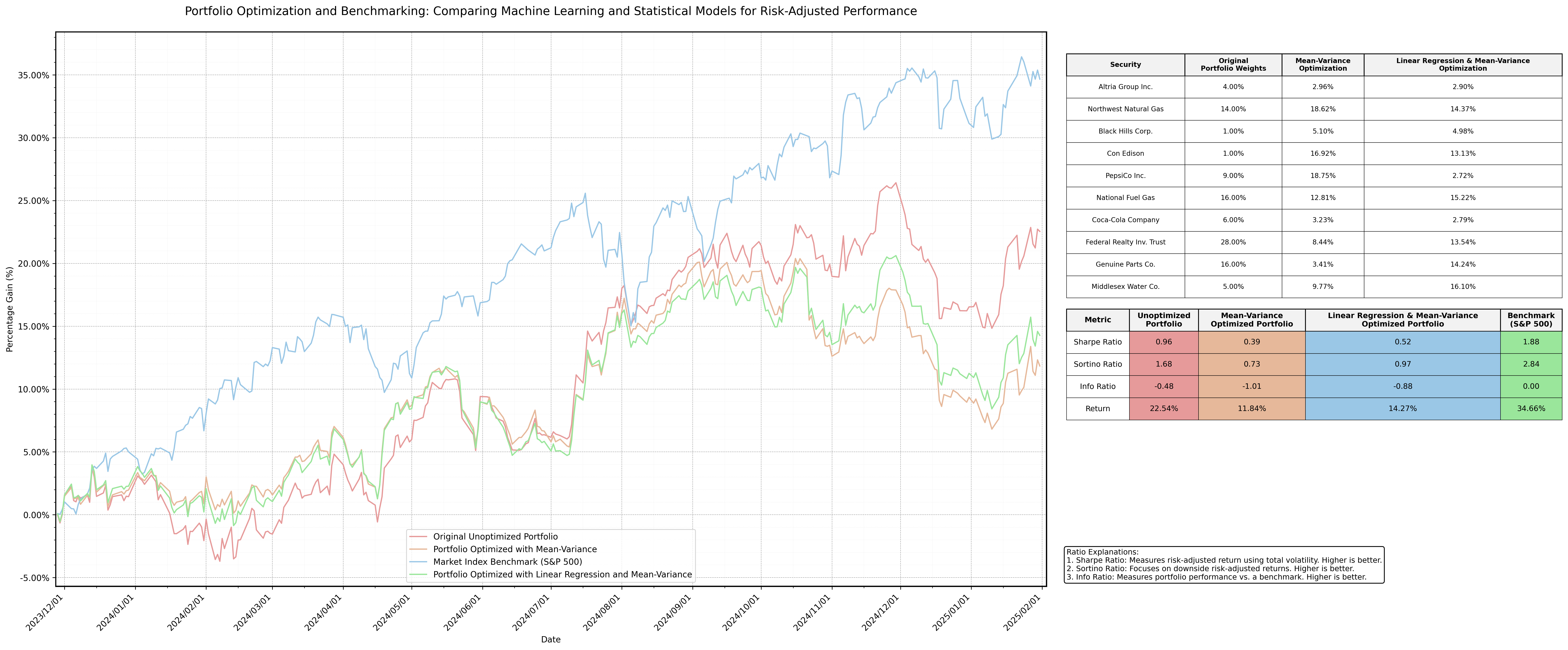

Example 2: Portfolio Optimization using Mean Variance and Machine Learning

RiskOptima.run_portfolio_optimization_mv_ml(

asset_table=asset_table,

training_start_date='2022-01-01',

training_end_date='2023-11-27',

model_type='Linear Regression',

risk_free_rate=0.05,

num_portfolios=100000,

market_benchmark=['SPY'],

max_volatility=0.15,

min_weight=0.03,

max_weight=0.2

)

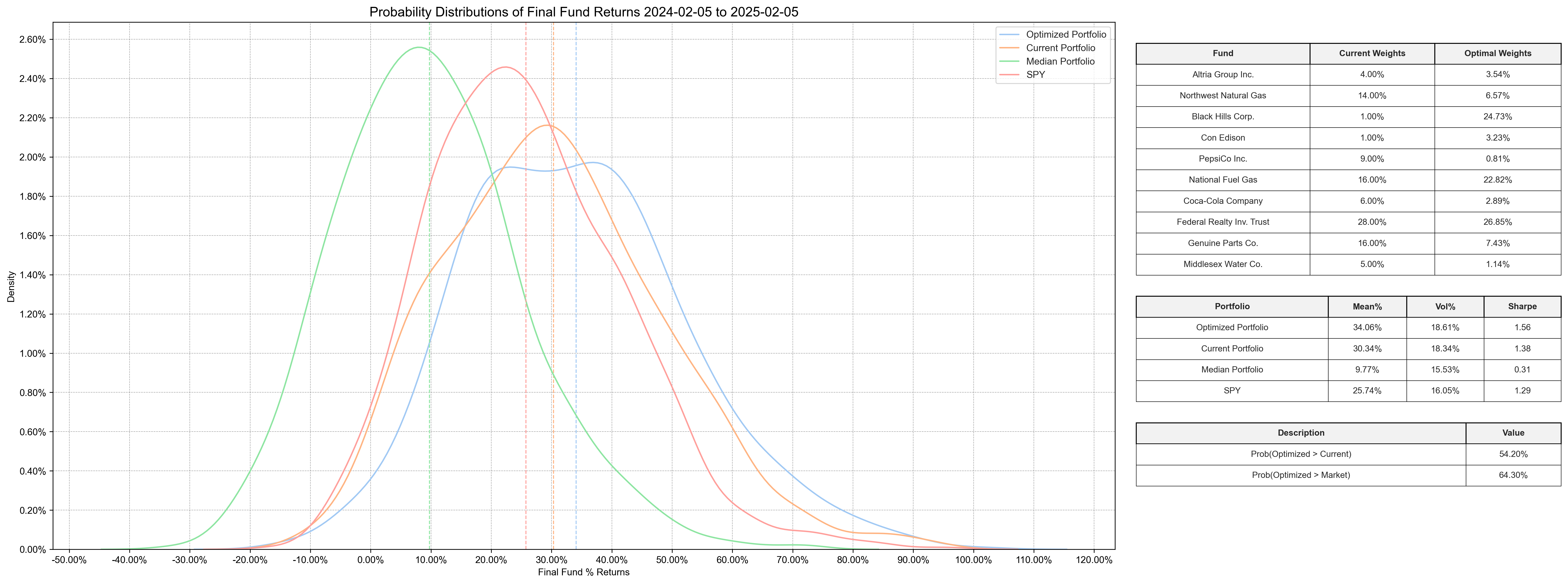

Example 3: Portfolio Optimization using Probability Analysis

ANALYSIS_START_DATE = RiskOptima.get_previous_year_date(RiskOptima.get_previous_working_day(), 1)

ANALYSIS_END_DATE = RiskOptima.get_previous_working_day()

BENCHMARK_INDEX = 'SPY'

RISK_FREE_RATE = 0.05

NUMBER_OF_WEIGHTS = 10_000

NUMBER_OF_MC_RUNS = 1_000

RiskOptima.run_portfolio_probability_analysis(

asset_table=asset_table,

analysis_start_date=ANALYSIS_START_DATE,

analysis_end_date=ANALYSIS_END_DATE,

benchmark_index=BENCHMARK_INDEX,

risk_free_rate=RISK_FREE_RATE,

number_of_portfolio_weights=NUMBER_OF_WEIGHTS,

trading_days_per_year=RiskOptima.get_trading_days(),

number_of_monte_carlo_runs=NUMBER_OF_MC_RUNS

)

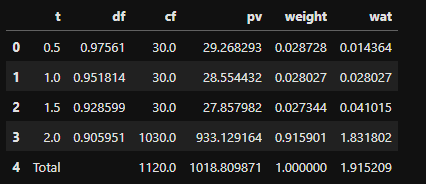

Example 4: Macaulay Duration

from riskoptima import RiskOptima

cf = RiskOptima.bond_cash_flows_v2(4, 1000, 0.06, 2) # 2 years, semi-annual, hence 4 periods

md_2 = RiskOptima.macaulay_duration_v3(cf, 0.05, 2)

md_2

Documentation

For complete documentation and usage examples, visit the GitHub repository:

Contributing

We welcome contributions! If you'd like to improve the package or report issues, please visit the GitHub repository.

License

RiskOptima is licensed under the MIT License.

Support me

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file riskoptima-1.17.0.tar.gz.

File metadata

- Download URL: riskoptima-1.17.0.tar.gz

- Upload date:

- Size: 33.8 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: poetry/1.8.5 CPython/3.12.7 Windows/10

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

cafa9422143e5cee5a8e0f58b27e27af4eaa891434f48456cc35b061f3b80b86

|

|

| MD5 |

f848fbfcddbaec73d945e89e3f55cbc8

|

|

| BLAKE2b-256 |

e357fff0690c4e53d0c7860b27afa79a317fe3f626b7228f38b1c8fe05363bc5

|

File details

Details for the file riskoptima-1.17.0-py3-none-any.whl.

File metadata

- Download URL: riskoptima-1.17.0-py3-none-any.whl

- Upload date:

- Size: 32.5 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: poetry/1.8.5 CPython/3.12.7 Windows/10

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

97d795b54a0b62cb70b3416e842416a2a017c951a7a30981110d992795d6bb2b

|

|

| MD5 |

a26991742fa07fc7c7a26387d7ce5816

|

|

| BLAKE2b-256 |

d1878d774df826ee113076091bf2064eb67d999770710d5bdc10749897185678

|