Pandas implementation of institutional-grade multi-factor risk model (Polars original by 0xfdf/toraniko)

Project description

toraniko-pandas

Pandas implementation of institutional-grade multi-factor risk model (Polars original by 0xfdf/toraniko)

Changelog

New Statistical Functions

The following functions in extras.py are inspired by the techniques described in "The Elements of Quantitative Investing" by Giuseppe A. Paleologo:

-

Covariance Estimation

shrinkage_cov: Implementation of Ledoit & Wolf's optimal shrinkage method for covariance matricesewma_cov: Exponentially Weighted Moving Average for covariance estimationlagged_covs: Calculation of lag-based covariance matrices for time series data

-

Autocorrelation-Consistent Covariance Estimation

autocorr_cov: Autocorrelation-consistent estimator for factor covariancenwest_cov: Newey-West estimator for heteroskedasticity and autocorrelation consistent covariance

-

CVXPY Optimization

estimate_factor_returns_cvxpy: Constrained optimization for factor return estimation_factor_returns_cvxpy: Implementation of the convex optimization approach with sum-zero constraints

These functions provide robust statistical methods for portfolio management, risk modeling, and factor analysis as described in modern quantitative finance literature.

Installation

pip install toraniko_pandas

User Manual

This notebook demonstrates factor analysis using SimFin financial data and custom factor models.

Important

You need free API key from SimFin to run my example. See their Github for more info. Create a .env file and place it like below

# SimFin

SIMFIN_API_KEY = "YOUR_KEY"

Data

import warnings

import matplotlib.pyplot as plt

import statsmodels.api as sm

from simfin_downloader import SimFin

from toraniko_pandas.model import estimate_factor_returns

from toraniko_pandas.styles import factor_mom, factor_sze, factor_val

from toraniko_pandas.utils import top_n_by_group

# Configure warnings

warnings.simplefilter(action="ignore", category=FutureWarning)

warnings.filterwarnings("ignore", message="invalid value encountered in log")

warnings.filterwarnings("ignore", message="divide by zero encountered in log")

simfin = SimFin()

df, sectors, industries = simfin.get_toraniko_data()

# Filter top 3000 companies by market cap

df = top_n_by_group(df.dropna(), 3000, "market_cap", ("date",), True)

# Display sector data

sectors

| sector_basic_materials | sector_business_services | sector_consumer_cyclical | sector_consumer_defensive | sector_energy | sector_financial_services | sector_healthcare | sector_industrials | sector_other | sector_real_estate | sector_technology | sector_utilities | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| symbol | ||||||||||||

| A | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| AA | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| AAC | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 |

| AACI | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 |

| AAC_delisted | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| ZWS | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| ZY | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| ZYME | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| ZYNE | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| ZYXI | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

5766 rows × 12 columns

# Display industry data

industries

| industry_advertising_and_marketing_services | industry_aerospace_and_defense | industry_agriculture | industry_airlines | industry_alternative_energy_sources_and_other | industry_application_software | industry_asset_management | industry_autos | industry_banks | industry_beverages_-_alcoholic | ... | industry_retail_-_defensive | industry_semiconductors | industry_steel | industry_tobacco_products | industry_transportation_and_logistics | industry_travel_and_leisure | industry_truck_manufacturing | industry_utilities_-_independent_power_producers | industry_utilities_-_regulated | industry_waste_management | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| symbol | |||||||||||||||||||||

| A | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| AA | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| AAC | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| AACI | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| AAC_delisted | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |

| ZWS | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| ZY | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| ZYME | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| ZYNE | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| ZYXI | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

5766 rows × 74 columns

# Asset returns was calculated by taking the percentage change of the adjusted close prices

ret_df = df[["symbol", "asset_returns"]]

ret_df

| symbol | asset_returns | |

|---|---|---|

| date | ||

| 2019-04-01 | EOSS | 0.041667 |

| 2019-04-01 | YTEN | 0.017544 |

| 2019-04-01 | GIDYL | 0.000000 |

| 2019-04-01 | VISL | -0.028571 |

| 2019-04-01 | ASLE | -0.001020 |

| ... | ... | ... |

| 2024-02-16 | NLY | -0.012099 |

| 2024-02-16 | AAPL | -0.008461 |

| 2024-02-16 | MSFT | -0.006159 |

| 2024-02-16 | WPC | 0.001669 |

| 2024-02-16 | RENT | -0.045675 |

3406422 rows × 2 columns

# Market cap is used to calculate the size factor and later to select the top N by market cap

cap_df = df[["symbol", "market_cap"]]

cap_df

| symbol | market_cap | |

|---|---|---|

| date | ||

| 2019-04-01 | EOSS | 1.600000e+05 |

| 2019-04-01 | YTEN | 2.939904e+05 |

| 2019-04-01 | GIDYL | 3.113633e+05 |

| 2019-04-01 | VISL | 3.423120e+05 |

| 2019-04-01 | ASLE | 3.623279e+05 |

| ... | ... | ... |

| 2024-02-16 | NLY | 2.291316e+12 |

| 2024-02-16 | AAPL | 2.865508e+12 |

| 2024-02-16 | MSFT | 3.016308e+12 |

| 2024-02-16 | WPC | 3.098176e+12 |

| 2024-02-16 | RENT | 8.506228e+12 |

3406422 rows × 2 columns

# To calculate the sector scores, we merge the sectors dataframe with the main dataframe

sector_scores = (

df.reset_index()

.merge(sectors, on="symbol")

.set_index("date")[["symbol"] + sectors.columns.tolist()]

)

sector_scores

| symbol | sector_basic_materials | sector_business_services | sector_consumer_cyclical | sector_consumer_defensive | sector_energy | sector_financial_services | sector_healthcare | sector_industrials | sector_other | sector_real_estate | sector_technology | sector_utilities | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| date | |||||||||||||

| 2019-04-01 | EOSS | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 2019-04-01 | YTEN | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 2019-04-01 | VISL | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 2019-04-01 | ASLE | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| 2019-04-01 | ALBO | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-02-16 | NLY | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 |

| 2024-02-16 | AAPL | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 2024-02-16 | MSFT | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 2024-02-16 | WPC | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 |

| 2024-02-16 | RENT | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

3393141 rows × 13 columns

# Size factor calculation

size_df = factor_sze(df, lower_decile=0.2, upper_decile=0.8)

# Momentum factor calculation

mom_df = factor_mom(df, trailing_days=252, winsor_factor=0.01)

# Value factor calculation

value_df = factor_val(df, winsor_factor=0.05)

# Momentum distribution

mom_df["mom_score"].hist(bins=100)

plt.title("Momentum Factor Distribution")

plt.show()

# Value distribution

value_df["val_score"].hist(bins=100)

plt.title("Value Factor Distribution")

plt.show()

# %% All of which we merge to get the style scores

style_scores = (

value_df.merge(mom_df, on=["symbol", "date"])

.merge(size_df, on=["symbol", "date"])

.dropna()

)

style_scores

| symbol | val_score | mom_score | sze_score | |

|---|---|---|---|---|

| date | ||||

| 2020-04-28 | ALBO | 2.732799 | -0.308748 | 3.418444 |

| 2020-04-28 | HSDT | 2.441402 | -1.777434 | 3.316239 |

| 2020-04-28 | ASLE | 1.547939 | 0.836804 | 3.259800 |

| 2020-04-28 | VISL | 2.732799 | -1.571045 | 3.042578 |

| 2020-04-28 | KNWN | 1.570320 | -0.325302 | 2.970678 |

| ... | ... | ... | ... | ... |

| 2024-02-16 | NLY | -2.076270 | 0.015212 | -2.906904 |

| 2024-02-16 | AAPL | -1.156765 | 0.344759 | -2.996094 |

| 2024-02-16 | MSFT | -0.963887 | 0.876672 | -3.016549 |

| 2024-02-16 | WPC | -2.877029 | -0.090848 | -3.027231 |

| 2024-02-16 | RENT | -2.327684 | -2.079591 | -3.430058 |

2479098 rows × 4 columns

ddf = (

ret_df.merge(cap_df, on=["date", "symbol"])

.merge(sector_scores, on=["date", "symbol"])

.merge(style_scores, on=["date", "symbol"])

.dropna()

.astype({"symbol": "category"})

)

returns_df = ddf[["symbol", "asset_returns"]]

mkt_cap_df = ddf[["symbol", "market_cap"]]

sector_df = ddf[["symbol"] + sectors.columns.tolist()]

style_df = ddf[style_scores.columns]

fac_df, eps_df = estimate_factor_returns(

returns_df,

mkt_cap_df,

sector_df,

style_df,

winsor_factor=0.1,

residualize_styles=False,

)

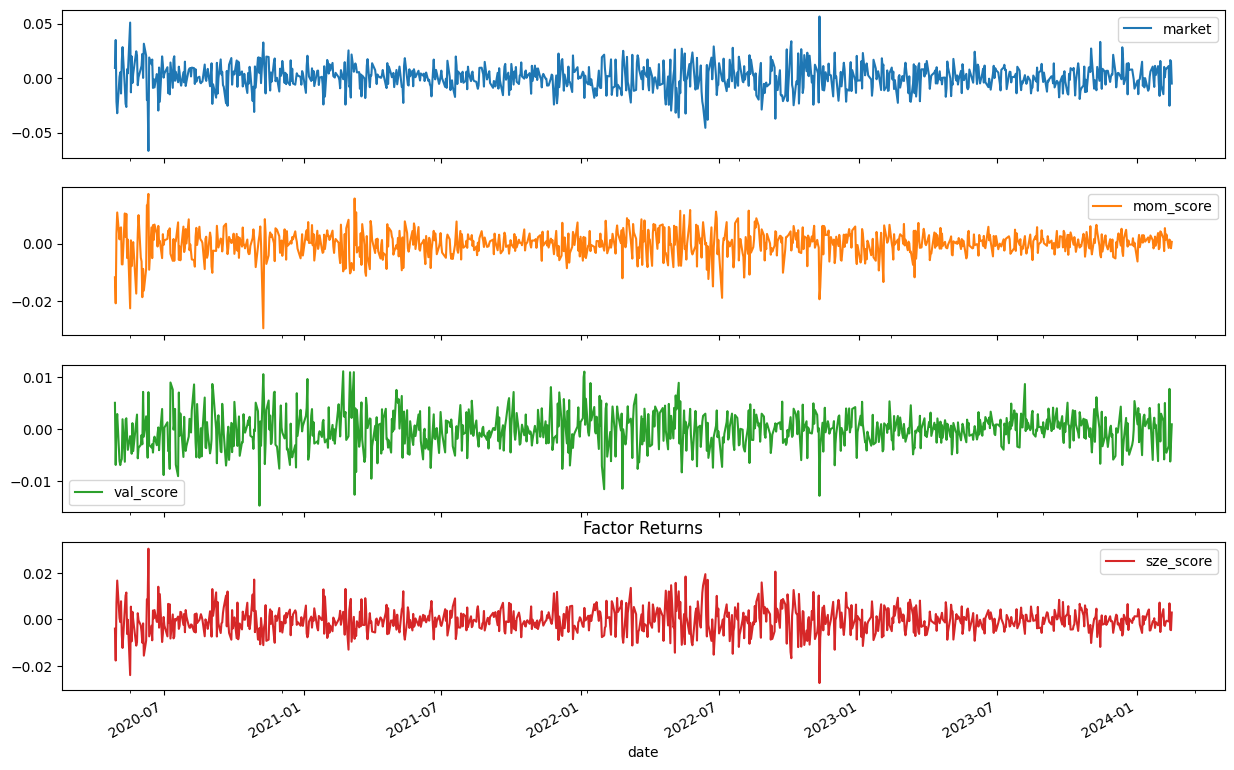

factor_cols = ["market","mom_score", "val_score", "sze_score"]

fac_df[factor_cols].plot(subplots=True, figsize=(15, 10))

plt.title("Factor Returns")

plt.show()

(fac_df[factor_cols] + 1).cumprod().plot(figsize=(15, 10))

plt.title("Factor Returns Cumulative")

plt.show()

y = returns_df.query("symbol == 'AAPL'")["asset_returns"]

X = fac_df[["market", "sector_technology", "mom_score", "val_score", "sze_score"]]

X = sm.add_constant(X)

model = sm.OLS(y, X)

results = model.fit().get_robustcov_results()

results.summary()

| Dep. Variable: | asset_returns | R-squared: | 0.610 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.608 |

| Method: | Least Squares | F-statistic: | 259.8 |

| Date: | Fri, 21 Feb 2025 | Prob (F-statistic): | 3.77e-175 |

| Time: | 10:42:32 | Log-Likelihood: | 2914.3 |

| No. Observations: | 959 | AIC: | -5817. |

| Df Residuals: | 953 | BIC: | -5787. |

| Df Model: | 5 | ||

| Covariance Type: | HC1 |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.0004 | 0.000 | 0.955 | 0.340 | -0.000 | 0.001 |

| market | -1.3258 | 0.175 | -7.594 | 0.000 | -1.668 | -0.983 |

| sector_technology | 0.3238 | 0.087 | 3.738 | 0.000 | 0.154 | 0.494 |

| mom_score | 0.4925 | 0.095 | 5.211 | 0.000 | 0.307 | 0.678 |

| val_score | -1.4278 | 0.233 | -6.140 | 0.000 | -1.884 | -0.971 |

| sze_score | -4.6804 | 0.389 | -12.030 | 0.000 | -5.444 | -3.917 |

| Omnibus: | 241.840 | Durbin-Watson: | 1.897 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 2493.520 |

| Skew: | 0.841 | Prob(JB): | 0.00 |

| Kurtosis: | 10.718 | Cond. No. | 1.14e+03 |

Notes:

[1] Standard Errors are heteroscedasticity robust (HC1)

[2] The condition number is large, 1.14e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

The strong multicollinearity is due to the estimated market factor derived from the sectors is almost correlated 1:1 with the sze factor.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file toraniko_pandas-0.1.2.tar.gz.

File metadata

- Download URL: toraniko_pandas-0.1.2.tar.gz

- Upload date:

- Size: 139.9 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.6.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d8f54be008d6cd45f39451bc54c9fe631fc07ecdf3c41507f8c63dc2a167ca08

|

|

| MD5 |

1909d3fcbda206e21562a7579c3bf207

|

|

| BLAKE2b-256 |

2bc43390770a9390a83ba36c0fe201ad0290158bc26a5e9aa9781ebf73e536af

|

File details

Details for the file toraniko_pandas-0.1.2-py3-none-any.whl.

File metadata

- Download URL: toraniko_pandas-0.1.2-py3-none-any.whl

- Upload date:

- Size: 18.1 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: uv/0.6.7

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

98fdf86f8fd5d6b4618ea46ea36d94e18bffa780d2b7466a34718c7eec859e1a

|

|

| MD5 |

2fc7cb0bdf5ffb2fe4aa6318979dc076

|

|

| BLAKE2b-256 |

beea7cb2d533ae6d52fb6ac97798a6a5bf8822e187a4c6474fcfd94b7f2dc1c9

|