Zerodha portfolio analytics: Markowitz efficient frontier reports with optional Fama-French factor-tilted stock selection

Project description

zerodha_portfolio

Zerodha portfolio analytics toolkit for practical equity allocation decisions:

- Markowitz efficient frontier report for your current holdings

- Fama-French factor-tilted stock selection followed by Markowitz optimization

It is built for users who already think in terms of stocks and quantities and want a visual, explainable report they can use for research, review meetings, or resume/project demonstration.

Install

pip install zerodha-portfolio

What You Input

Both workflows start from a dictionary of stocks and quantities:

portfolio = {

"RELIANCE": 18,

"TCS": 24,

"INFY": 32,

"HDFCBANK": 20,

}

You also provide:

start_date(required)end_date(optional)risk_free_rate(optional, default0.06)

What You Get Back

Both APIs return a Python dictionary with key metrics and a saved HTML report path:

output_htmlsymbolsuser_weightstangency_weightsuser_return,user_vol,user_sharpetangency_return,tangency_vol,tangency_sharpe

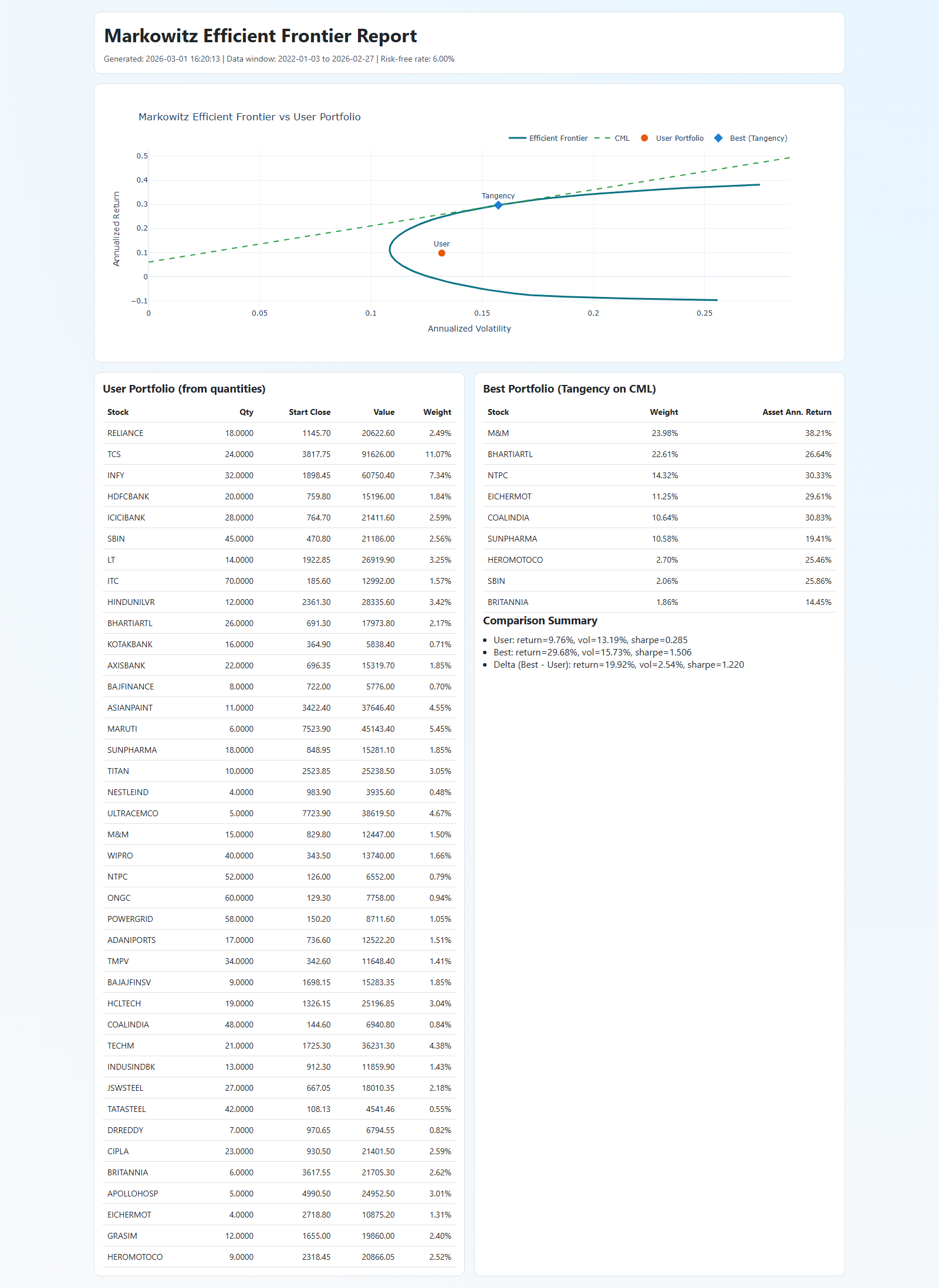

The HTML report includes:

- Efficient Frontier curve

- Capital Market Line (CML)

- Your current portfolio point

- Tangency (max-Sharpe) portfolio point

- Portfolio composition tables

- Comparison summary

Workflow 1: Markowitz Report

Use this when you already have a portfolio and want to compare it against the mathematically optimal long-only allocation from the same stock universe.

Example Code

from kiteconnect import KiteConnect

from zerodha_portfolio import generate_markowitz_report

kite = KiteConnect(api_key="your_api_key")

kite.set_access_token("your_access_token")

result = generate_markowitz_report(

kite=kite,

portfolio_quantities={

"RELIANCE": 18,

"TCS": 24,

"INFY": 32,

"HDFCBANK": 20,

},

start_date="2022-01-01",

end_date="2026-02-28",

output_file_name="markowitz_report",

risk_free_rate=0.06,

)

print(result["output_html"])

Example Script and Sample Report

- Script:

examples/example_report.py - Sample output:

examples/markowitz_report.html

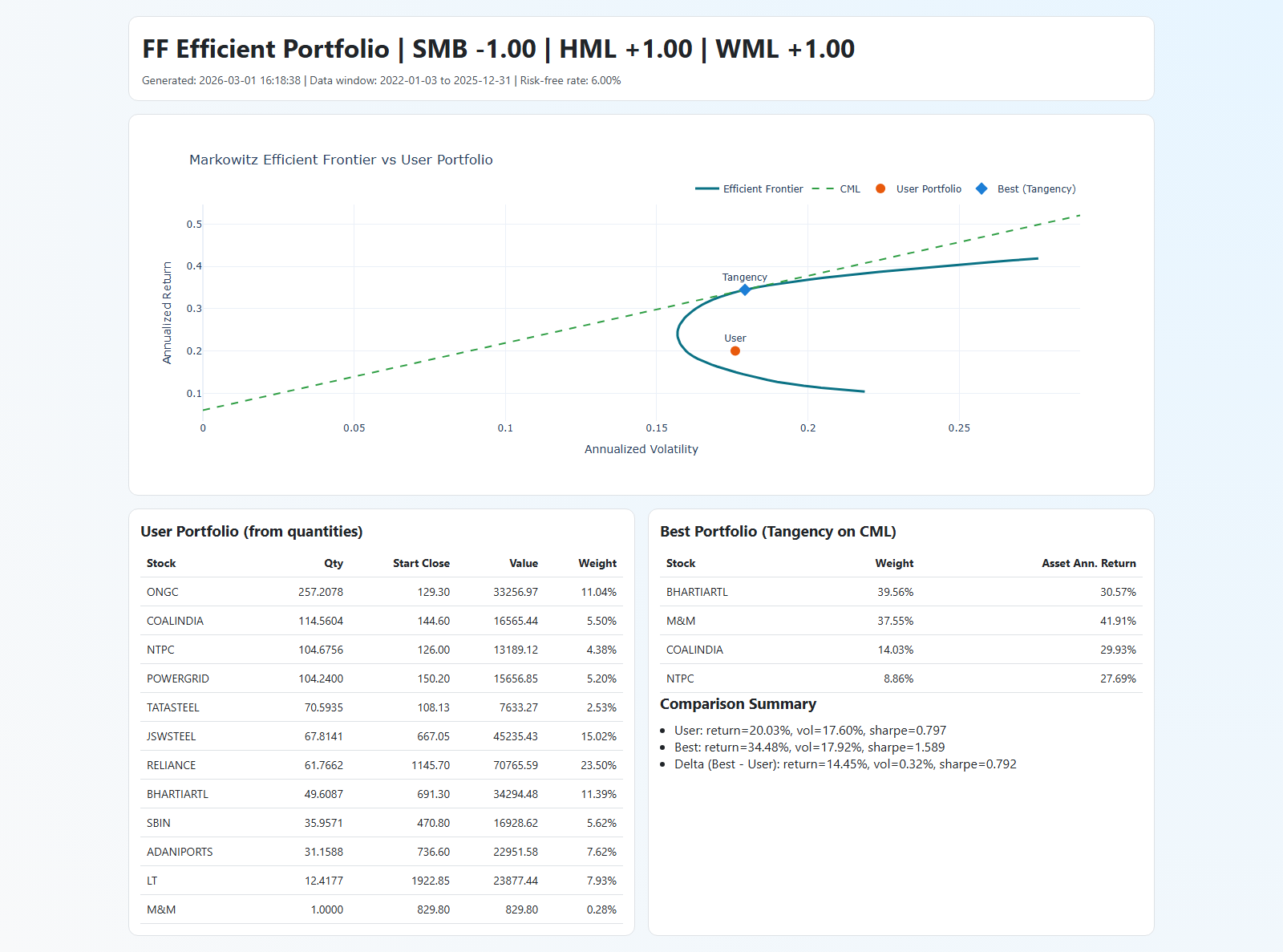

Workflow 2: Fama-French -> Markowitz Report

Use this when you want factor-aware stock selection first, and only then run mean-variance optimization on the selected basket.

This workflow:

- Loads Indian Fama-French + Momentum factors (downloaded or local file)

- Estimates each stock's factor betas

- Scores stocks using your factor preference

- Picks top stocks (

top_n) - Runs Markowitz report on that selected set

SMB, HML, WML Meaning

-

SMB(Small Minus Big): size factor -

Positive means tilt toward small-cap stocks

-

Negative means tilt toward large-cap stocks

-

HML(High Minus Low): value factor -

Positive means tilt toward value stocks (high book-to-market)

-

Negative means tilt toward growth stocks

-

WML(Winners Minus Losers): momentum factor -

Positive means tilt toward recent outperformers

-

Negative means tilt toward anti-momentum / reversal

Preference Input Format

Provide factor preferences using -1 to +1:

preference = {

"beta_smb": 1.0, # small-cap tilt

"beta_hml": 1.0, # value tilt

"beta_wml": 1.0, # momentum tilt

}

Examples:

- Small + Value + Momentum:

{"beta_smb": 1.0, "beta_hml": 1.0, "beta_wml": 1.0} - Large + Growth:

{"beta_smb": -1.0, "beta_hml": -1.0} - Neutral on momentum:

{"beta_smb": 0.5, "beta_hml": 0.5, "beta_wml": 0.0}

Example Code

from kiteconnect import KiteConnect

from zerodha_portfolio import generate_fama_french_markowitz_report

kite = KiteConnect(api_key="your_api_key", timeout=30)

kite.set_access_token("your_access_token")

result = generate_fama_french_markowitz_report(

kite=kite,

candidate_quantities={

"RELIANCE": 18,

"TCS": 24,

"INFY": 32,

"HDFCBANK": 20,

"ICICIBANK": 28,

"SBIN": 45,

},

start_date="2022-01-01",

end_date="2026-02-28",

frequency="daily",

preference={"beta_smb": -1.0, "beta_hml": 1.0, "beta_wml": 1.0},

top_n=12,

output_file_name="ff_markowitz_report",

risk_free_rate=0.06,

# Optional fallback if download URL changes:

# factor_file_path=r"C:\\path\\to\\ff_file.csv",

)

print(result["output_html"])

print(result["ff_selected_weights"])

Example Script and Sample Report

- Script:

examples/example_ff_markowitz.py - Sample output:

examples/ff_markowitz_report.html

API Summary

generate_markowitz_report(...)generate_fama_french_markowitz_report(...)download_ff_factor_files(...)load_ff_factors(...)estimate_stock_factor_betas(...)build_factor_tilt_portfolio(...)

Backward-compatible import is preserved:

from zerodha_markowitz import generate_markowitz_report

Output File Behavior

output_html: full output path (highest priority)output_file_name: file name only (saved in script run directory)- If neither is given, a default name is used:

- Markowitz:

markowitz_report.html - FF-Markowitz:

ff_markowitz_report.html

- Markowitz:

Data Source

- IIMA Indian Fama-French + Momentum dataset: https://faculty.iima.ac.in/iffm/Indian-Fama-French-Momentum/

License

MIT

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file zerodha_portfolio-0.2.1.tar.gz.

File metadata

- Download URL: zerodha_portfolio-0.2.1.tar.gz

- Upload date:

- Size: 833.0 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.14.2

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

729e0d208e374596cf1d931c503da41c6214e5e2135577e0c9d63204a0558332

|

|

| MD5 |

fd1b7159407da5d8e7948e1a4f035162

|

|

| BLAKE2b-256 |

d79bdf69f93c6c1f0f181880a24a8a0f224c69fcaea07ebc43a35ca5a8b4668d

|

File details

Details for the file zerodha_portfolio-0.2.1-py3-none-any.whl.

File metadata

- Download URL: zerodha_portfolio-0.2.1-py3-none-any.whl

- Upload date:

- Size: 26.7 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.14.2

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

a1f26e8c98b778150d38715e76f183c753b6850a3497f45cbabbd0bcbac6d554

|

|

| MD5 |

387a08b6f1c40bfc06b71d5419ef43a2

|

|

| BLAKE2b-256 |

27994c263643ef46047c6f220b988698fc8c88da4e9eab4e26a545cc5596f685

|