Live Trading and backtesting platform in Python

Project description

backtrader-next

Live Trading and backtesting platform written in Python.

Installation

pip install backtrader-next

History

Package is based on backtrader

Changes:

- Added new Chart plotting using bn-lightweight-charts-python.

- Improved testing performance by using the

PandasDatafeed inrunonce=Truemode. - Added performance statistics in both text format (similar to Backtesting.py) and HTML format (similar to Quantstats).

- Improved support for switching between futures (for testing, etc.).

- Added new indicators implemented with Numba.

- Improved performance — now it runs about 2–3× slower than Backtesting.py in

runonce=Truemode withPandasData. - Detailed results

- Interactive visualizations

Here a snippet of a Simple Moving Average CrossOver.

import pandas as pd

import backtrader_next as bt

from backtrader_next.feeds import PandasData

class SimpleSizer(bt.Sizer):

params = (

('percents', 99),

)

def _getsizing(self, comminfo, cash, data, isbuy):

value = self.broker.getvalue()

price = data.close[0]+comminfo.p.commission

size = value / price * (self.params.percents / 100)

return int(size)

class SmaCross(bt.Strategy):

params = (

('MA1', 20),

('MA2', 50),

)

def __init__(self):

self.Order = None

self.ma1 = bt.nind.SMA(self.data.close, period=self.params.MA1)

self.ma2 = bt.nind.SMA(self.data.close, period=self.params.MA2)

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]: # Order is submitted/accepted

return # Do nothing until the order is completed

elif order.status in [order.Canceled, order.Margin, order.Rejected]: # Canceled, Margin, Rejected

print('Order was Canceled/Margin/Rejected')

self.Order = None # Reset order

def next(self):

# Use ONLY Long Positions

if self.crossover(self.ma1, self.ma2):

pos = self.getposition()

if pos:

self.close(size=pos.size)

self.Order = self.buy()

elif self.crossover(self.ma2, self.ma1):

pos = self.getposition()

if pos:

self.close(size=pos.size)

# self.Order = self.sell()

def crossover(self, ma1, ma2):

try:

return ma1[-1] <= ma2[-1] and ma1[0] > ma2[0]

except IndexError:

return False

if __name__ == '__main__':

cerebro = bt.Cerebro()

cerebro.broker.setcash(1_000_000.0)

cerebro.broker.set_shortcash(False)

cerebro.broker.setcommission(commission=0, margin=1, mult=1)

cerebro.addsizer(SimpleSizer, percents=90)

df = pd.read_csv(f"AAPL_1d.csv.zip", sep=";")

df['Datetime'] = pd.to_datetime(df['Date'].astype(str) , format='%Y-%m-%d')

df.set_index('Datetime', inplace=True)

data = PandasData(dataframe=df, timeframe=bt.TimeFrame.Days, compression=1)

cerebro.adddata(data, name='AAPL')

cerebro.addstrategy(SmaCross, )

print(f'Starting Portfolio Value: {cerebro.broker.getvalue():.2f}\n')

results = cerebro.run()

print(f'\nFinal Portfolio Value: {cerebro.broker.getvalue():.2f}\n')

rc = cerebro.statistics()

print(rc)

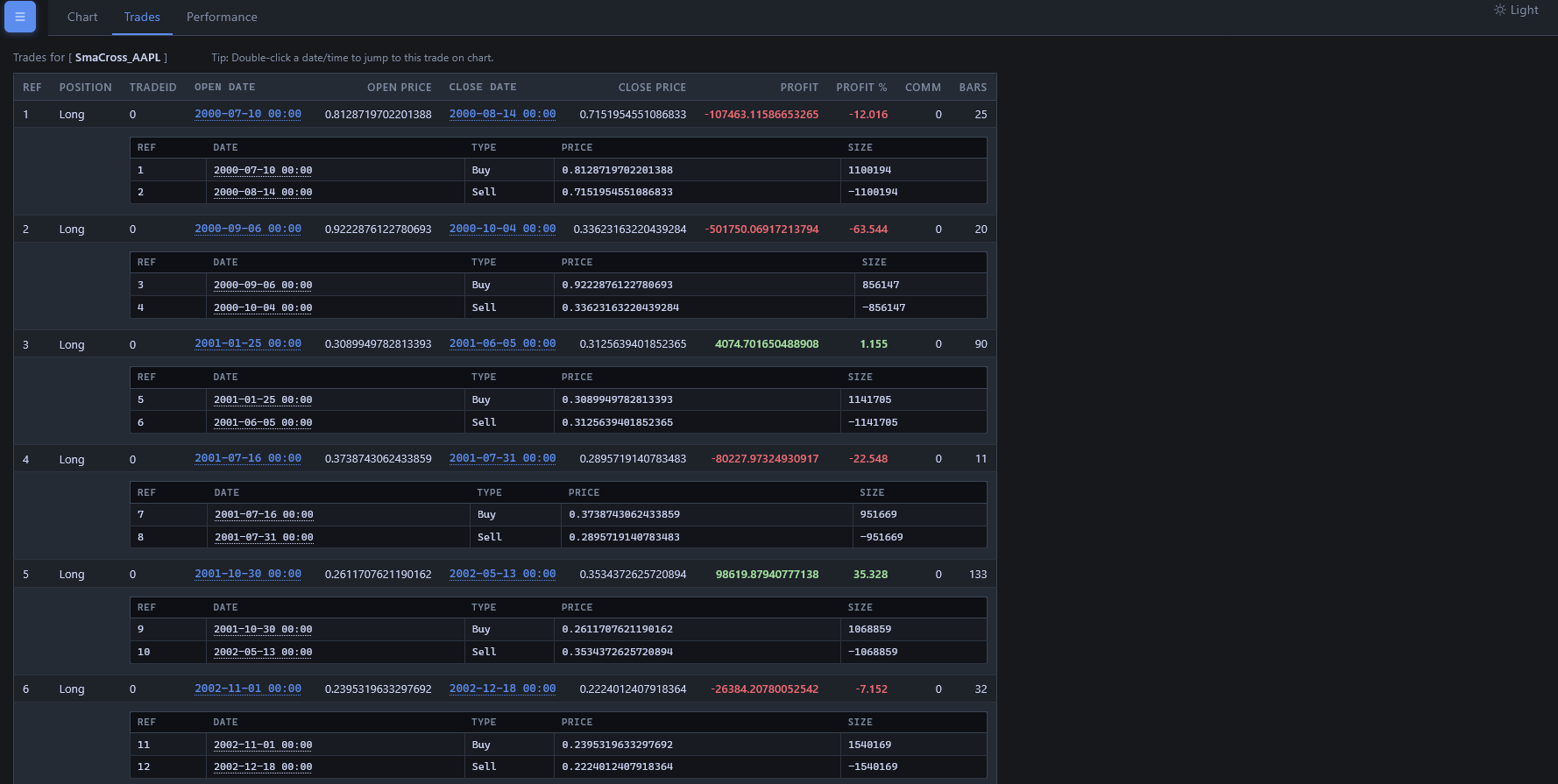

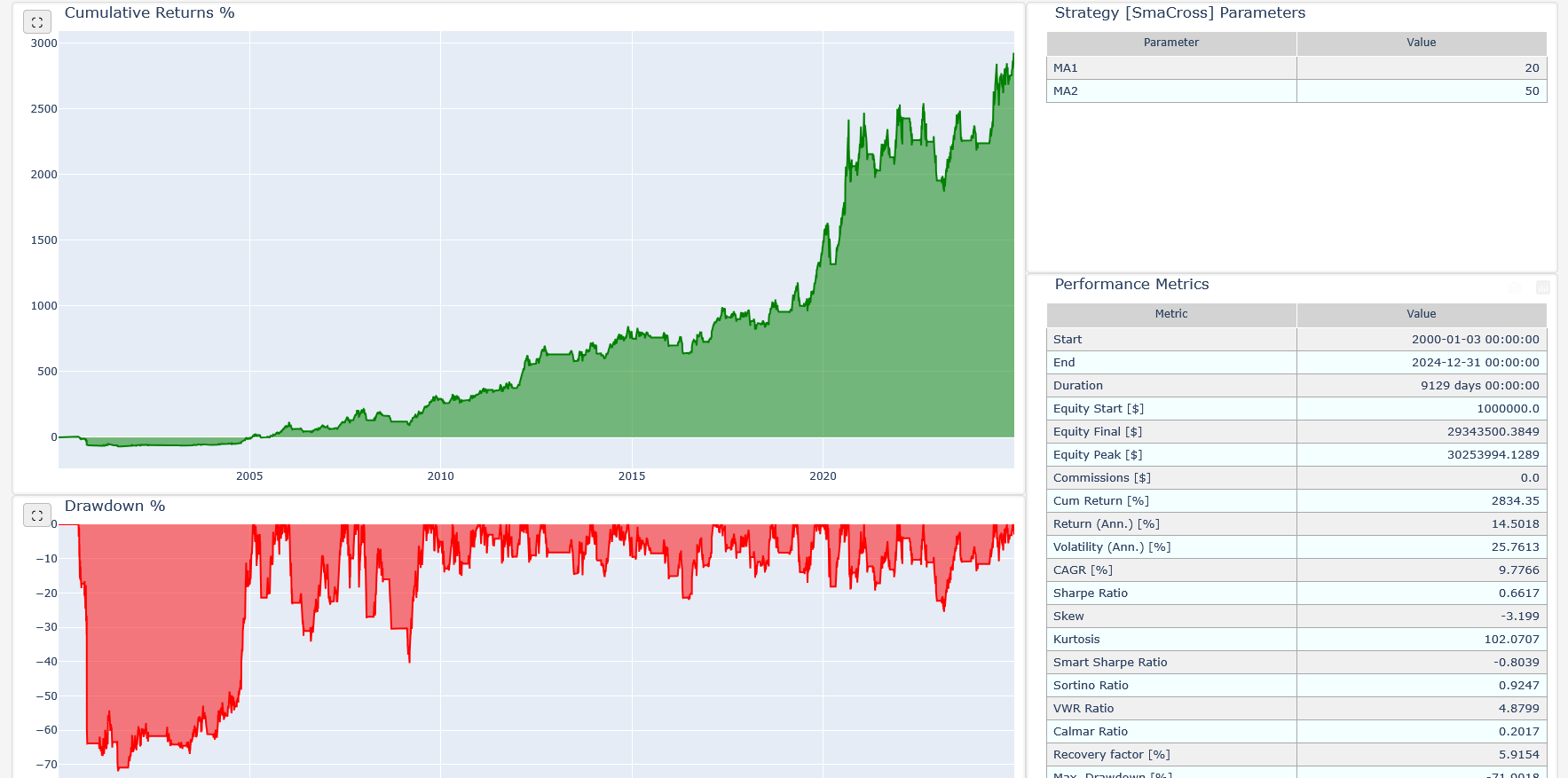

cerebro.plot(filename="smacross.html")

cerebro.show_report(filename="smacross_stats.html")

print("end")

Output log

Starting Portfolio Value: 1000000.00

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Order was Canceled/Margin/Rejected

Final Portfolio Value: 13125987.48

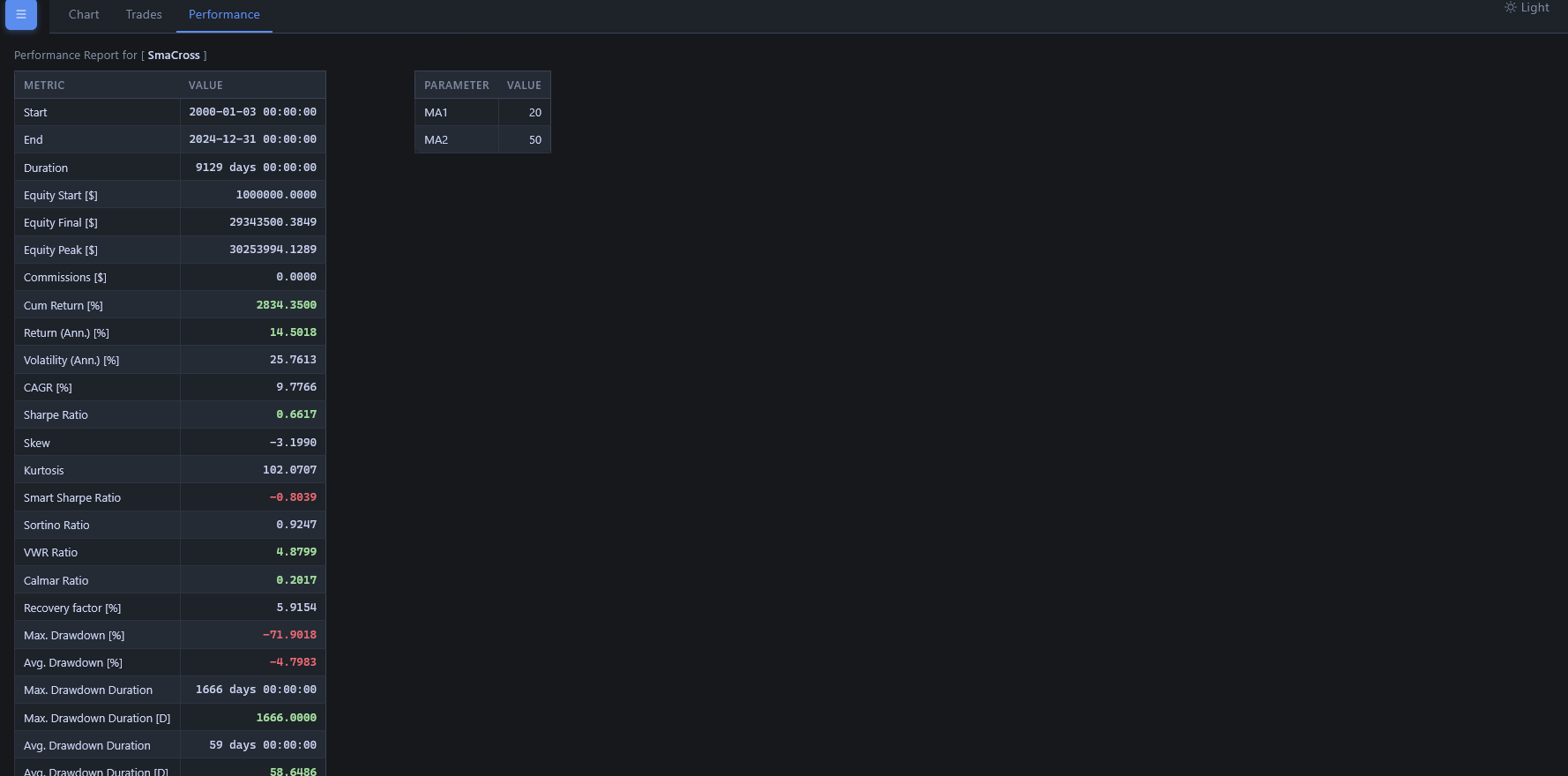

Strategy SmaCross

MA1 20

MA2 50

Start 2000-01-03 00:00:00

End 2024-12-31 00:00:00

Duration 9129 days 00:00:00

Equity Start [$] 1000000.0

Equity Final [$] 13125987.479046

Equity Peak [$] 13533263.280804

Commissions [$] 0.0

Cum Return [%] 1212.5987

Return (Ann.) [%] 10.8691

Volatility (Ann.) [%] 21.0469

CAGR [%] 7.3656

Sharpe Ratio 0.6044

Skew -6.1434

Kurtosis 219.8529

Smart Sharpe Ratio -1.7922

Sortino Ratio 0.812

VWR Ratio 3.6777

Calmar Ratio 0.1917

Recovery factor [%] 5.5986

Max. Drawdown [%] -56.6963

Avg. Drawdown [%] -4.674

Max. Drawdown Duration 2492 days 00:00:00

Avg. Drawdown Duration 69 days 00:00:00

Drawdown Peak 2000-10-03 00:00:00

# Trades 56

Win Rate [%] 55.3571

Best Trade [%] 92.0365

Worst Trade [%] -63.5437

Avg. Trade [%] 4.8655

Max. Trade Duration 276 days 00:00:00

Avg. Trade Duration 85 days 00:00:00

Profit Factor 1.1756

Expectancy [%] 0.0505

SQN 2.2935

Kelly Criterion [%] 37.6406

dtype: object

end

It will create two HTML files and open it in your current browser.

- smacross.html - charts and trade stats

- smacross_stats.html - quantstats like strategy report

Features:

Live Trading and backtesting platform written in Python.

-

Live Data Feed and Trading with

- Interactive Brokers (needs

IbPyand benefits greatly from an installedpytz) - Visual Chart (needs a fork of

comtypesuntil a pull request is integrated in the release and benefits frompytz) - Oanda (needs

oandapy) (REST API Only - v20 did not support streaming when implemented)

- Interactive Brokers (needs

-

Data feeds from csv/files, online sources or from pandas and blaze

-

Filters for datas, like breaking a daily bar into chunks to simulate intraday or working with Renko bricks

-

Multiple data feeds and multiple strategies supported

-

Multiple timeframes at once

-

Integrated Resampling and Replaying

-

Step by Step backtesting or at once (except in the evaluation of the Strategy)

-

Integrated battery of indicators

-

TA-Lib indicator support (needs python ta-lib / check the docs)

-

Easy development of custom indicators

-

Analyzers (for example: TimeReturn, Sharpe Ratio, SQN) and

pyfoliointegration (deprecated) -

Flexible definition of commission schemes

-

Integrated broker simulation with Market, Close, Limit, Stop, StopLimit, StopTrail, StopTrailLimitand OCO orders, bracket order, slippage, volume filling strategies and continuous cash adjustmet for future-like instruments

-

Sizers for automated staking

-

Cheat-on-Close and Cheat-on-Open modes

-

Schedulers

-

Trading Calendars

-

Plotting (requires matplotlib)

Documentation

The old blog for backtrader:

Blog <http://www.backtrader.com/blog>_

Read the full old documentation at:

Documentation <http://www.backtrader.com/docu>_

List of built-in Indicators (122)

Indicators Reference <http://www.backtrader.com/docu/indautoref.html>_

An example for IB Data Feeds/Trading:

-

IbPydoesn't seem to be in PyPi. Do either::pip install git+https://github.com/blampe/IbPy.git

or (if

gitis not available in your system)::pip install https://github.com/blampe/IbPy/archive/master.zip

For other functionalities like: Visual Chart, Oanda, TA-Lib, check

the dependencies in the documentation.

From source:

- Place the backtrader_next directory found in the sources inside your project

Version numbering

X.Y.Z

- X: Major version number. Should stay stable unless something big is changed

like an overhaul to use

numpy - Y: Minor version number. To be changed upon adding a complete new feature or (god forbids) an incompatible API change.

- Z: Revision version number. To be changed for documentation updates, small changes, small bug fixes

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file backtrader_next-2.0.0.tar.gz.

File metadata

- Download URL: backtrader_next-2.0.0.tar.gz

- Upload date:

- Size: 6.0 MB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.10.12

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

9b9bb5950347d51d2a30b5fdfed403d560ff489b87e6effae33d9d224be36c40

|

|

| MD5 |

b035e0f98ec9dbf182f4cbf53941cf65

|

|

| BLAKE2b-256 |

080a9185f2623c059cbaacb8e6b866d058bdd5be048cd247f7132fc67d3c0ae8

|

File details

Details for the file backtrader_next-2.0.0-py3-none-any.whl.

File metadata

- Download URL: backtrader_next-2.0.0-py3-none-any.whl

- Upload date:

- Size: 470.3 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.2.0 CPython/3.10.12

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

c2c2f7d1131d96c29d4dd2c6d1b111d9d5fe7acafe4265495f8f1d7215c1ffbb

|

|

| MD5 |

e2c89eba2df1129d060e2306bb531020

|

|

| BLAKE2b-256 |

bd990380685e0292b103848bbb3d7595596a4079a151f24f2760bcc9e97a52a5

|