A Python package for Coherent Conformal Prediction.

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Project description

👖 Conformal Tights

Conformal Tights is a Python package for Coherent Conformal Prediction✦ that exports:

- 🍬 a scikit-learn meta-estimator that adds coherent conformal prediction of quantiles and intervals to any scikit-learn regressor

- 🔮 a Darts forecaster that adds coherent conformal probabilistic time series forecasting to any scikit-learn regressor

Features

[!TIP] ✦Coherent Conformal Prediction (CCP): what makes Conformal Tights unique is that it produces so-called coherent conformally calibrated quantile predictions. Without coherence, a model's predicted quantiles may cross each other in practice. For instance, the 25th percentile prediction may be higher than the 75th percentile prediction. With coherence, the predicted quantiles increase monotonically as you would expect.

- 🚦 Coherent: quantiles increase monotonically instead of crossing each other

- 🌡️ Conformal: prediction intervals with reliable coverage and accurate quantile predictions

- 🪜 Dynamic: two-level conformal calibration of both absolute and relative residuals

- 👖 Tight: selects the lowest dispersion that provides the desired coverage

- 🎁 Data efficient: requires only a small number of calibration examples to fit

- 🐼 Pandas support: optionally predict on DataFrames and receive DataFrame output

Using

Quick links

Installing

pip install conformal-tights

Predicting quantiles

Conformal Tights exports a meta-estimator called ConformalCoherentQuantileRegressor that you can use to equip any scikit-learn regressor with a predict_quantiles method that predicts conformally calibrated quantiles. Example usage:

from conformal_tights import ConformalCoherentQuantileRegressor

from sklearn.datasets import fetch_openml

from sklearn.model_selection import train_test_split

from xgboost import XGBRegressor

# Fetch dataset and split in train and test

X, y = fetch_openml("ames_housing", version=1, return_X_y=True, as_frame=True, parser="auto")

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.15, random_state=42)

# Create a regressor, equip it with conformal prediction, and fit on the train set

my_regressor = XGBRegressor(objective="reg:absoluteerror")

conformal_predictor = ConformalCoherentQuantileRegressor(estimator=my_regressor)

conformal_predictor.fit(X_train, y_train)

# Predict with the underlying regressor

ŷ_test = conformal_predictor.predict(X_test)

# Predict quantiles with the conformal predictor

ŷ_test_quantiles = conformal_predictor.predict_quantiles(

X_test, quantiles=(0.025, 0.05, 0.1, 0.5, 0.9, 0.95, 0.975)

)

When the input data is a pandas DataFrame, the output is also a pandas DataFrame. For example, printing the head of ŷ_test_quantiles yields:

| house_id | 0.025 | 0.05 | 0.1 | 0.5 | 0.9 | 0.95 | 0.975 |

|---|---|---|---|---|---|---|---|

| 1357 | 114720.3 | 120910.8 | 131770.3 | 156708.2 | 175907.8 | 187996.1 | 205443.4 |

| 2367 | 67382.7 | 80191.7 | 86871.8 | 105807.1 | 118470.3 | 127582.6 | 142321.1 |

| 2822 | 119068.0 | 131864.8 | 138541.6 | 159447.7 | 179178.5 | 197245.5 | 214206.2 |

| 2126 | 93860.7 | 100048.8 | 111389.7 | 134292.7 | 150557.1 | 164595.8 | 182524.1 |

| 1544 | 68959.8 | 81648.8 | 88364.1 | 108298.3 | 122315.3 | 132425.1 | 147109.3 |

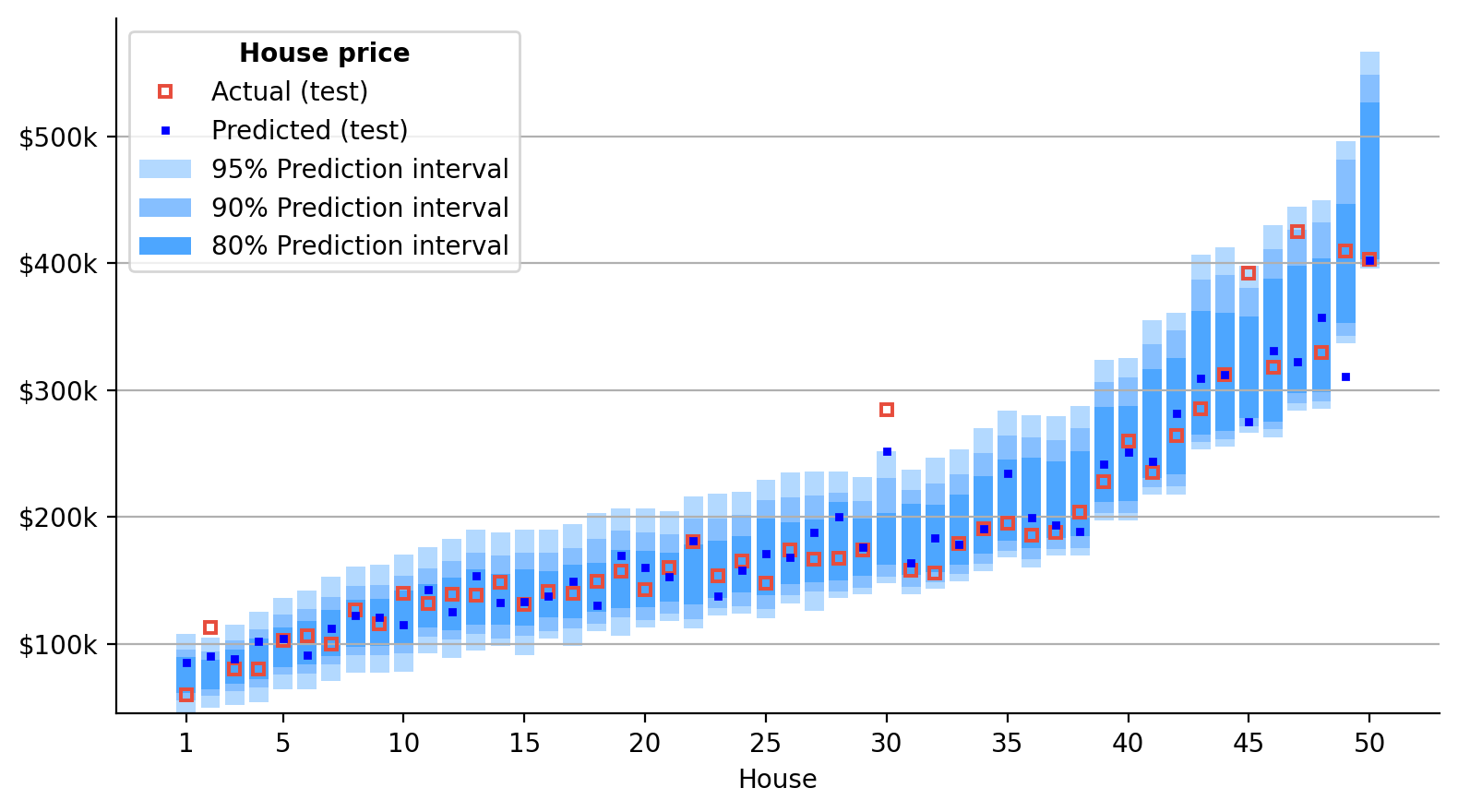

Let's visualize the predicted quantiles on the test set:

Expand to see the code that generated the graph above

import matplotlib.pyplot as plt

import matplotlib.ticker as ticker

%config InlineBackend.figure_format = "retina"

plt.rc("font", family="DejaVu Sans", size=10)

plt.figure(figsize=(8, 4.5))

idx = ŷ_test_quantiles[0.5].sample(50, random_state=42).sort_values().index

x = list(range(1, len(idx) + 1))

x_ticks = [1, *list(range(5, len(idx) + 1, 5))]

for j in range(3):

coverage = round(100 * (ŷ_test_quantiles.columns[-(j + 1)] - ŷ_test_quantiles.columns[j]))

plt.bar(

x,

ŷ_test_quantiles.loc[idx].iloc[:, -(j + 1)] - ŷ_test_quantiles.loc[idx].iloc[:, j],

bottom=ŷ_test_quantiles.loc[idx].iloc[:, j],

color=["#b3d9ff", "#86bfff", "#4da6ff"][j],

label=f"{coverage}% Prediction interval",

)

plt.plot(

x,

y_test.loc[idx],

"s",

label="Actual (test)",

markeredgecolor="#e74c3c",

markeredgewidth=1.414,

markerfacecolor="none",

markersize=4,

)

plt.plot(x, ŷ_test.loc[idx], "s", color="blue", label="Predicted (test)", markersize=2)

plt.xlabel("House")

plt.xticks(x_ticks, x_ticks)

plt.gca().yaxis.set_major_formatter(ticker.FuncFormatter(lambda x, _: f"${x/1000:,.0f}k"))

plt.gca().tick_params(axis="both", labelsize=10)

plt.gca().spines["top"].set_visible(False)

plt.gca().spines["right"].set_visible(False)

plt.grid(False)

plt.grid(axis="y")

plt.legend(loc="upper left", title="House price", title_fontproperties={"weight": "bold"})

plt.tight_layout()

Predicting intervals

In addition to quantile prediction, you can use predict_interval to predict conformally calibrated prediction intervals. Compared to quantiles, these focus on reliable coverage over quantile accuracy. Example usage:

# Predict an interval for each example with the conformal predictor

ŷ_test_interval = conformal_predictor.predict_interval(X_test, coverage=0.95)

# Measure the coverage of the prediction intervals on the test set

coverage = ((ŷ_test_interval.iloc[:, 0] <= y_test) & (y_test <= ŷ_test_interval.iloc[:, 1])).mean()

print(coverage) # 96.6%

When the input data is a pandas DataFrame, the output is also a pandas DataFrame. For example, printing the head of ŷ_test_interval yields:

| house_id | 0.025 | 0.975 |

|---|---|---|

| 1357 | 107202.8 | 206290.4 |

| 2367 | 66665.1 | 146004.8 |

| 2822 | 115591.8 | 220314.8 |

| 2126 | 85288.1 | 183037.8 |

| 1544 | 67889.9 | 150646.2 |

Forecasting time series

Conformal Tights also exports a Darts forecaster called DartsForecaster that uses a ConformalCoherentQuantileRegressor to make conformally calibrated probabilistic time series forecasts. To demonstrate its usage, let's begin by loading a time series dataset:

from darts.datasets import ElectricityConsumptionZurichDataset

# Load a forecasting dataset

ts = ElectricityConsumptionZurichDataset().load()

ts = ts.resample("h")

# Split the dataset into covariates X and target y

X = ts.drop_columns(["Value_NE5", "Value_NE7"])

y = ts["Value_NE5"] # NE5 = Household energy consumption

# Add categorical covariates to X

X = X.add_holidays(country_code="CH")

X = X.add_datetime_attribute("month")

X = X.add_datetime_attribute("dayofweek")

X = X.add_datetime_attribute("hour")

X_categoricals = ["holidays", "month", "dayofweek", "hour"]

Printing the tail of the covariates time series X.pd_dataframe() yields:

| Timestamp | Hr [%Hr] | RainDur [min] | StrGlo [W/m2] | T [°C] | WD [°] | WVs [m/s] | WVv [m/s] | p [hPa] | holidays | month | dayofweek | hour |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2022‑08‑30 20h | 70.2 | 0.0 | 0.0 | 19.9 | 290.2 | 1.7 | 1.5 | 968.5 | 0.0 | 7.0 | 1.0 | 20.0 |

| 2022‑08‑30 21h | 70.1 | 0.0 | 0.0 | 19.5 | 239.2 | 1.0 | 0.7 | 968.1 | 0.0 | 7.0 | 1.0 | 21.0 |

| 2022‑08‑30 22h | 71.3 | 0.0 | 0.0 | 19.5 | 28.9 | 1.5 | 1.3 | 967.9 | 0.0 | 7.0 | 1.0 | 22.0 |

| 2022‑08‑30 23h | 80.4 | 0.0 | 0.0 | 18.9 | 24.3 | 1.6 | 1.1 | 967.9 | 0.0 | 7.0 | 1.0 | 23.0 |

| 2022‑08‑31 00h | 81.6 | 1.0 | 0.0 | 18.7 | 293.5 | 0.9 | 0.3 | 967.8 | 0.0 | 7.0 | 2.0 | 0.0 |

We can now equip a scikit-learn regressor with conformal prediction using ConformalCoherentQuantileRegressor as before, and then equip that conformal predictor with probabilistic time series forecasting using DartsForecaster:

from conformal_tights import DartsForecaster, ConformalCoherentQuantileRegressor

from pandas import Timestamp

from xgboost import XGBRegressor

# Split the dataset into train and test

test_cutoff = Timestamp("2022-06-01")

y_train, y_test = y.split_after(test_cutoff)

X_train, X_test = X.split_after(test_cutoff)

# Now let's:

# 1. Create an sklearn regressor of our choosing, in this case `XGBRegressor`

# 2. Add conformal quantile prediction to the regressor with `ConformalCoherentQuantileRegressor`

# 3. Add probabilistic forecasting to the conformal predictor with `DartsForecaster`

my_regressor = XGBRegressor()

conformal_predictor = ConformalCoherentQuantileRegressor(estimator=my_regressor)

forecaster = DartsForecaster(

model=conformal_predictor,

lags=5 * 24, # Add the last 5 days of the target to the prediction features

lags_future_covariates=[0], # Add the current timestamp's covariates to the prediction features

categorical_future_covariates=X_categoricals, # Convert these covariates to pd.Categorical

)

# Fit the forecaster

forecaster.fit(y_train, future_covariates=X_train)

# Make a probabilistic forecast 5 days into the future by generating 500 forecast paths, where each

# step is sampled from the point-in-time quantiles predicted by the conformal model

quantiles = (0.025, 0.05, 0.1, 0.25, 0.5, 0.75, 0.9, 0.95, 0.975)

forecast = forecaster.predict(

n=5 * 24, future_covariates=X_test, num_samples=500, quantiles=quantiles

)

Printing the head of the forecast quantiles time series forecast.quantile(quantiles).to_dataframe() yields:

| Timestamp | Value_NE5_q0.025 | Value_NE5_q0.050 | Value_NE5_q0.100 | Value_NE5_q0.250 | Value_NE5_q0.500 | Value_NE5_q0.750 | Value_NE5_q0.900 | Value_NE5_q0.950 | Value_NE5_q0.975 |

|---|---|---|---|---|---|---|---|---|---|

| 2022‑06‑01 01h | 19274.5 | 19394.9 | 19516.3 | 19756.8 | 19983.2 | 20185.9 | 20392.7 | 20497.1 | 20591.7 |

| 2022‑06‑01 02h | 19147.0 | 19252.3 | 19396.7 | 19624.3 | 19895.0 | 20130.5 | 20334.6 | 20445.2 | 20582.1 |

| 2022‑06‑01 03h | 19332.1 | 19448.3 | 19632.1 | 19931.0 | 20231.7 | 20486.7 | 20689.0 | 20876.7 | 20999.2 |

| 2022‑06‑01 04h | 21649.3 | 21827.0 | 22195.7 | 22619.9 | 23158.6 | 23470.7 | 23802.8 | 24026.9 | 24246.9 |

| 2022‑06‑01 05h | 24669.7 | 25045.8 | 25279.7 | 25624.5 | 26153.4 | 26797.1 | 27147.0 | 27318.5 | 27487.5 |

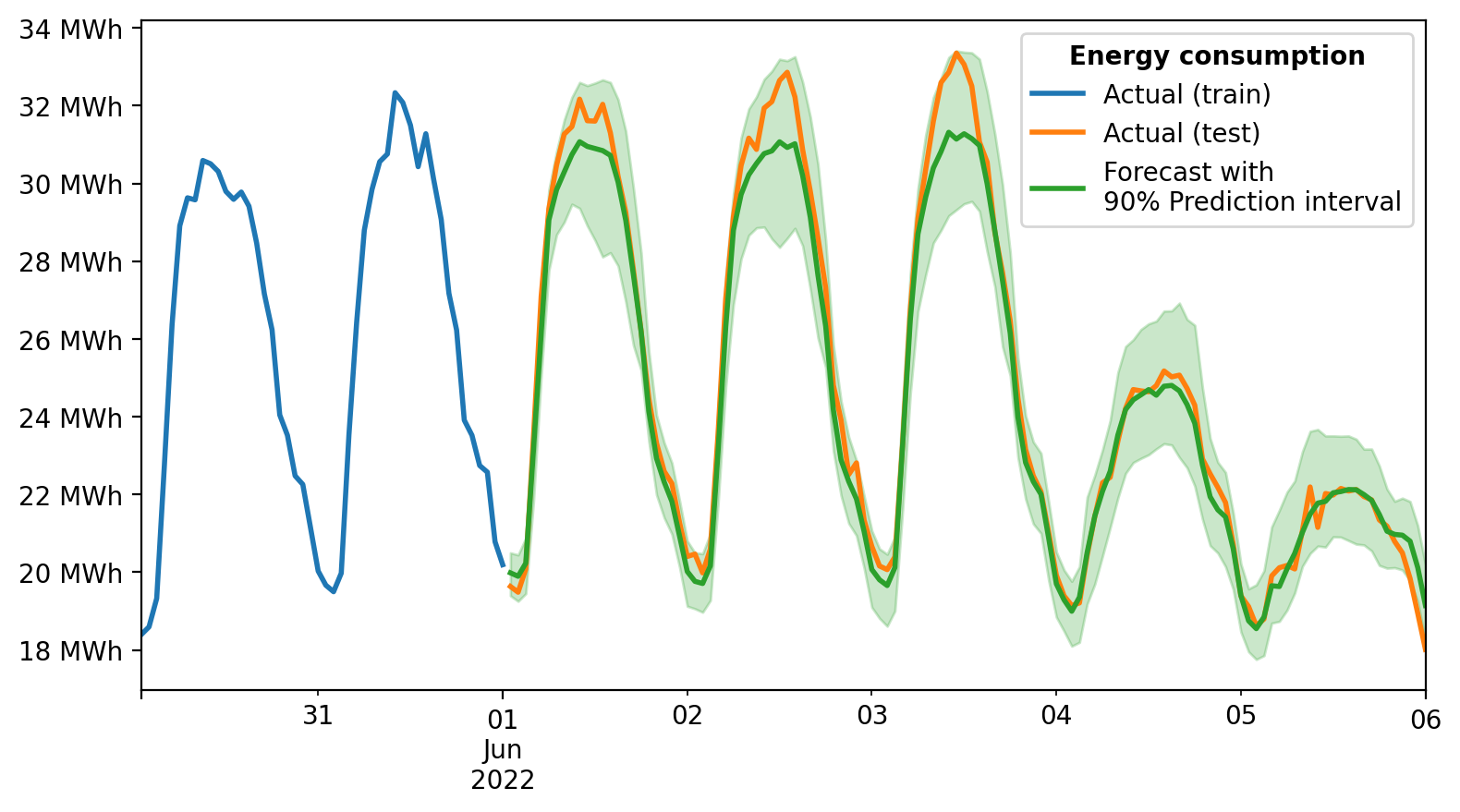

Let's visualize the forecast and its prediction interval on the test set:

Expand to see the code that generated the graph above

import matplotlib.pyplot as plt

import matplotlib.ticker as ticker

%config InlineBackend.figure_format = "retina"

plt.rc("font", family="DejaVu Sans", size=10)

plt.figure(figsize=(8, 4.5))

y_train[-2 * 24 :].plot(label="Actual (train)")

y_test[: len(forecast)].plot(label="Actual (test)")

forecast.plot(label="Forecast with\n90% Prediction interval", low_quantile=0.05, high_quantile=0.95)

plt.gca().set_xlabel("")

plt.gca().yaxis.set_major_formatter(ticker.FuncFormatter(lambda x, _: f"{x/1000:,.0f} MWh"))

plt.gca().tick_params(axis="both", labelsize=10)

plt.legend(loc="upper right", title="Energy consumption", title_fontproperties={"weight": "bold"})

plt.tight_layout()

Contributing

Prerequisites

-

Generate an SSH key and add the SSH key to your GitHub account.

-

Configure SSH to automatically load your SSH keys:

cat << EOF >> ~/.ssh/config Host * AddKeysToAgent yes IgnoreUnknown UseKeychain UseKeychain yes ForwardAgent yes EOF

-

Install VS Code and VS Code's Dev Containers extension. Alternatively, install PyCharm.

-

Optional: install a Nerd Font such as FiraCode Nerd Font and configure VS Code or PyCharm to use it.

Development environments

The following development environments are supported:

-

⭐️ GitHub Codespaces: click on Open in GitHub Codespaces to start developing in your browser.

-

⭐️ VS Code Dev Container (with container volume): click on Open in Dev Containers to clone this repository in a container volume and create a Dev Container with VS Code.

-

⭐️ uv: clone this repository and run the following from root of the repository:

# Create and install a virtual environment uv sync --python 3.10 --all-extras # Activate the virtual environment source .venv/bin/activate # Install the pre-commit hooks pre-commit install --install-hooks

-

VS Code Dev Container: clone this repository, open it with VS Code, and run Ctrl/⌘ + ⇧ + P → Dev Containers: Reopen in Container.

-

PyCharm Dev Container: clone this repository, open it with PyCharm, create a Dev Container with Mount Sources, and configure an existing Python interpreter at

/opt/venv/bin/python.

Developing

- This project follows the Conventional Commits standard to automate Semantic Versioning and Keep A Changelog with Commitizen.

- Run

poefrom within the development environment to print a list of Poe the Poet tasks available to run on this project. - Run

uv add {package}from within the development environment to install a run time dependency and add it topyproject.tomlanduv.lock. Add--devto install a development dependency. - Run

uv sync --upgradefrom within the development environment to upgrade all dependencies to the latest versions allowed bypyproject.toml. Add--only-devto upgrade the development dependencies only. - Run

cz bumpto bump the package's version, update theCHANGELOG.md, and create a git tag. Then push the changes and the git tag withgit push origin main --tags.

Project details

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file conformal_tights-0.5.0.tar.gz.

File metadata

- Download URL: conformal_tights-0.5.0.tar.gz

- Upload date:

- Size: 24.6 kB

- Tags: Source

- Uploaded using Trusted Publishing? Yes

- Uploaded via: uv/0.10.12 {"installer":{"name":"uv","version":"0.10.12","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

346043c85416028bb8af90da239a3ade830fd2343606aff55dc18492558740dd

|

|

| MD5 |

2140072bd9bd3b1130be4c6d6c7a8791

|

|

| BLAKE2b-256 |

402f017bc3d767177e844b5c9a606f52fcc76480df9d84a419430ad6d2689124

|

File details

Details for the file conformal_tights-0.5.0-py3-none-any.whl.

File metadata

- Download URL: conformal_tights-0.5.0-py3-none-any.whl

- Upload date:

- Size: 20.2 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? Yes

- Uploaded via: uv/0.10.12 {"installer":{"name":"uv","version":"0.10.12","subcommand":["publish"]},"python":null,"implementation":{"name":null,"version":null},"distro":{"name":"Ubuntu","version":"24.04","id":"noble","libc":null},"system":{"name":null,"release":null},"cpu":null,"openssl_version":null,"setuptools_version":null,"rustc_version":null,"ci":true}

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

1d0b437b08a52ba0a5012763bb4465052497c0d507a281f8c0fc698484f6e338

|

|

| MD5 |

a12963206644837dbc41bca745622834

|

|

| BLAKE2b-256 |

fe82e0c81d7fb8cb89331d24f5ef0aac85d65a3eba5282beb894f10a9a45d15e

|