Analytics for quants

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Project description

jQuantStats: Portfolio Analytics for Quants

Overview

jQuantStats is a Python library for portfolio analytics that helps quants and portfolio managers understand their strategy performance in depth. It provides two complementary entry points: a Portfolio route that works directly from price and position data, and a Data route for arbitrary return streams. All analytics, visualizations, and HTML reports are available from either entry point.

The library is inspired by QuantStats, but extends it significantly — particularly around position-level analysis that is impossible when you start from a return series alone. Key improvements include:

- Polars-native design with zero pandas runtime dependency

- Modern interactive visualizations using Plotly

- A Portfolio route — the primary entry point — that exposes tools unavailable in QuantStats

- Comprehensive test coverage with pytest

- Clean, fully type-annotated API

The Portfolio Route — Why It Matters

The original QuantStats only accepts a return series. That is convenient but lossy: once you reduce prices and positions to returns, you lose the information needed to answer the questions that matter most in practice.

jQuantStats introduces Portfolio as the primary entry point. You provide the raw

price series and the cash positions your strategy held over time, and the library compiles

the NAV for you. This unlocks a class of analysis tools that simply do not exist in

QuantStats:

Execution-Delay Analysis

Real strategies suffer from execution lag: the signal fires at the close, but the trade

fills the next open, or the next close, or later. A return series hides this completely.

A Portfolio exposes it.

import numpy as np

import polars as pl

from jquantstats import Portfolio

rng = np.random.default_rng(42)

n = 252 # approximately one trading year

prices = pl.DataFrame({

"date": pl.date_range(pl.date(2020, 1, 2), pl.date(2020, 12, 31), interval="1d", eager=True)[:n],

"AAPL": (100.0 * np.cumprod(1 + rng.normal(0.0005, 0.015, n))).tolist(),

"META": (150.0 * np.cumprod(1 + rng.normal(0.0003, 0.018, n))).tolist(),

})

# Allocate $500k to each asset as constant cash positions

positions = prices.select("date").with_columns([

pl.lit(500_000.0).alias("AAPL"),

pl.lit(500_000.0).alias("META"),

])

pf = Portfolio.from_cash_position(prices=prices, cash_position=positions, aum=1_000_000)

# Shift all positions forward by one period — simulate T+1 execution

pf_lagged = pf.lag(1)

sharpe_t0 = pf.stats.sharpe() # ideal (no delay)

sharpe_t1 = pf_lagged.stats.sharpe() # realistic (T+1 fill)

lag(n) returns a new Portfolio with positions shifted by n periods.

Because every downstream accessor — .stats, .plots, .report — recomputes

on the shifted positions, a single call gives you the full analytics picture

under a different execution assumption.

lead_lag_ir_plot() sweeps the entire range at once and renders it as an

interactive Plotly bar chart:

fig = pf.plots.lead_lag_ir_plot(start=-5, end=10)

# fig.show() — Sharpe ratio at each lag, from lead-5 to lag+10

This chart immediately answers: how much does a one-day execution delay cost in Sharpe? At what lag does the signal degrade to noise?

Tilt / Timing Attribution

Even without lag analysis, starting from positions lets you decompose performance into two orthogonal sources:

- Tilt — the portfolio with constant average weights (pure allocation skill)

- Timing — the deviation from average weights (pure timing skill)

tilt_pf = pf.tilt # constant-weight version of the strategy

timing_pf = pf.timing # weight deviations only

tilt_sharpe = tilt_pf.stats.sharpe()

timing_sharpe = timing_pf.stats.sharpe()

decomp = pf.tilt_timing_decomp # DataFrame: portfolio | tilt | timing NAVs side by side

Turnover Analytics

turnover = pf.turnover # daily one-way turnover as fraction of AUM

turnover_weekly = pf.turnover_weekly # weekly aggregate (or 5-period rolling sum)

turnover_summary = pf.turnover_summary() # mean_daily, mean_weekly, turnover_std

turnover = pf.turnover # daily one-way turnover as fraction of AUM

turnover_weekly = pf.turnover_weekly # weekly aggregate (or 5-period rolling sum)

turnover_summary = pf.turnover_summary() # mean_daily, mean_weekly, turnover_std

Cost Modeling

Two independent cost models, never accidentally combined:

from jquantstats import Portfolio, CostModel

# Model A: per-unit cost (equity, futures tick-size costs)

pf_net = Portfolio.from_cash_position(

prices=prices, cash_position=positions, aum=1_000_000,

cost_model=CostModel.per_unit(0.01),

)

net_cost_nav = pf_net.net_cost_nav # NAV path after deducting position-delta costs

# Model B: turnover-bps cost (macro, fund-of-funds)

pf_bps = Portfolio.from_cash_position(

prices=prices, cash_position=positions, aum=1_000_000,

cost_model=CostModel.turnover_bps(5.0),

)

# Sweep Sharpe across 0 → 20 bps in a single call

impact = pf_bps.trading_cost_impact(max_bps=20)

Position Variants

# From unit positions (quantity × price → cash automatically)

units = prices.select("date").with_columns([

pl.lit(1_000.0).alias("AAPL"),

pl.lit(500.0).alias("META"),

])

pf = Portfolio.from_position(prices=prices, position=units, aum=1_000_000)

# From risk positions (de-volatized via EWMA, optional vol cap)

risk_units = units

pf = Portfolio.from_risk_position(

prices=prices, risk_position=risk_units, aum=1_000_000,

vol_cap=0.20,

)

# Smooth noisy positions with a rolling mean

pf_smooth = pf.smoothed_holding(n=5)

jQuantStats vs QuantStats

| Feature | jQuantStats | QuantStats |

|---|---|---|

| DataFrame engine | Polars (zero pandas at runtime) | pandas |

| Visualisation | Interactive Plotly charts | Static matplotlib / seaborn |

| Input format | polars.DataFrame |

pandas.Series / pandas.DataFrame |

| Entry point — positions | Portfolio.from_cash_position(prices, cash_position, aum) |

— |

| Entry point — returns | Data.from_returns(returns, benchmark) |

qs.reports.full(returns) |

| Execution-delay analysis | pf.lag(n) + pf.plots.lead_lag_ir_plot() |

— |

| Tilt / timing decomposition | pf.tilt, pf.timing, pf.tilt_timing_decomp |

— |

| Turnover analytics | pf.turnover, pf.turnover_summary() |

— |

| Cost models | Two models: per-unit and turnover-bps | — |

| Cost-impact sweep | pf.trading_cost_impact(max_bps=20) |

— |

| HTML report | pf.report.to_html() |

qs.reports.html(returns) |

| Snapshot chart | pf.plots.snapshot() |

qs.plots.snapshot(returns) |

| Sharpe ratio | pf.stats.sharpe() |

qs.stats.sharpe(returns) |

| Max drawdown | pf.stats.max_drawdown() |

qs.stats.max_drawdown(returns) |

| Python version | 3.11+ | 3.7+ |

| Type annotations | Full (py.typed) |

Partial |

| Test coverage | |

— |

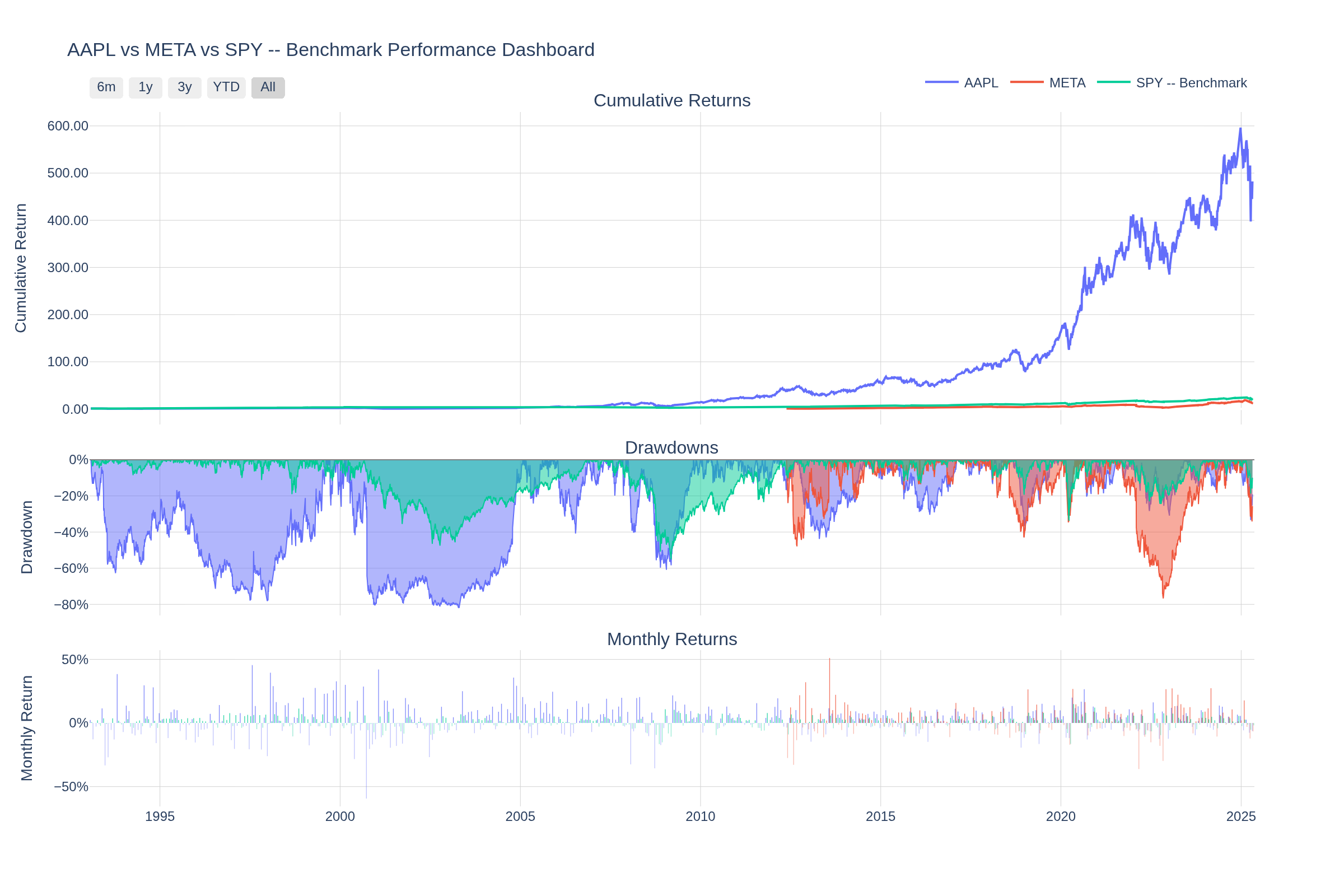

Dashboard Preview

Interactive Plotly dashboard — cumulative returns, drawdowns, and monthly return heatmaps in a single view. Charts are fully interactive (zoom, pan, hover tooltips) when rendered in a browser.

Installation

Using pip:

pip install jquantstats

Using conda (via conda-forge):

conda install -c conda-forge jquantstats

For development:

pip install jquantstats[dev]

Quick Start

Start from prices and positions (recommended)

import polars as pl

from jquantstats import Portfolio

prices = pl.DataFrame({

"date": ["2023-01-01", "2023-01-02", "2023-01-03"],

"AAPL": [150.0, 152.0, 149.5],

"MSFT": [250.0, 253.0, 251.0],

}).with_columns(pl.col("date").str.to_date())

positions = pl.DataFrame({

"date": ["2023-01-01", "2023-01-02", "2023-01-03"],

"AAPL": [500.0, 500.0, 600.0],

"MSFT": [300.0, 300.0, 300.0],

}).with_columns(pl.col("date").str.to_date())

pf = Portfolio.from_cash_position(prices=prices, cash_position=positions, aum=1_000_000)

sharpe = pf.stats.sharpe()

fig = pf.plots.snapshot() # call fig.show() to display

Compare ideal vs. delayed execution

pf_t0 = pf # signal executed immediately

pf_t1 = pf.lag(1) # T+1 execution

pf_t2 = pf.lag(2) # T+2 execution

sharpe_t0 = pf_t0.stats.sharpe()

sharpe_t1 = pf_t1.stats.sharpe()

sharpe_t2 = pf_t2.stats.sharpe()

# Or visualize the full lead/lag Sharpe profile in one chart

fig = pf.plots.lead_lag_ir_plot(start=-5, end=10)

# fig.show()

Start from a return series

import polars as pl

from jquantstats import Data

returns = pl.DataFrame({

"Date": ["2023-01-01", "2023-01-02", "2023-01-03", "2023-01-04", "2023-01-05"],

"Strategy": [0.01, -0.03, 0.02, -0.01, 0.04],

}).with_columns(pl.col("Date").str.to_date())

benchmark = pl.DataFrame({

"Date": ["2023-01-01", "2023-01-02", "2023-01-03", "2023-01-04", "2023-01-05"],

"Benchmark": [0.005, -0.01, 0.008, -0.005, 0.015],

}).with_columns(pl.col("Date").str.to_date())

data = Data.from_returns(returns=returns, benchmark=benchmark)

sharpe = data.stats.sharpe() # {'Strategy': 4.24, 'Benchmark': 4.94}

max_dd = data.stats.max_drawdown() # {'Strategy': 0.03, 'Benchmark': 0.01}

fig = data.plots.snapshot(title="Strategy vs Benchmark") # call fig.show() to display

Risk metrics

sharpe = data.stats.sharpe()

sortino = data.stats.sortino()

max_dd = data.stats.max_drawdown()

vol = data.stats.volatility()

var = data.stats.value_at_risk()

cvar = data.stats.conditional_value_at_risk()

calmar = data.stats.calmar()

win = data.stats.win_rate()

Benchmark comparison

ir = data.stats.information_ratio()

greeks = data.stats.greeks()

alpha = greeks["Strategy"]["alpha"]

beta = greeks["Strategy"]["beta"]

Generate a full HTML report

pf = Portfolio.from_cash_position(prices=prices, cash_position=positions, aum=1_000_000)

html = pf.report.to_html()

with open("report.html", "w") as f:

f.write(html)

Features

Performance Metrics — Sharpe, Sortino, Calmar, Omega, Treynor, Information Ratio, probabilistic Sharpe/Sortino, smart Sharpe/Sortino, CAGR, GHPR, and more.

Risk Analysis — Value at Risk (VaR), Conditional VaR, drawdown details, max drawdown duration, Ulcer Index, Ulcer Performance Index, risk of ruin.

Win/Loss Statistics — win rate, monthly win rate, profit factor, payoff ratio, consecutive wins/losses, tail ratio, gain-to-pain ratio, outlier win/loss ratios.

Benchmark Analysis — alpha, beta, correlation, tracking error, information ratio, up/down capture ratios, R².

Rolling Analytics — rolling Sharpe, Sortino, volatility, and Greeks with configurable windows.

Portfolio-native (not available in QuantStats):

- Execution-delay analysis via

lag(n)andlead_lag_ir_plot() - Tilt / timing attribution via

tilt,timing,tilt_timing_decomp - Turnover analytics via

turnover,turnover_weekly,turnover_summary() - Cost modeling via

CostModel.per_unit()/CostModel.turnover_bps() - Cost-impact sweep via

trading_cost_impact(max_bps) - Position smoothing via

smoothed_holding(window) - Risk-position entry via

from_risk_position()with EWMA de-volatization

Interactive Visualizations — all charts are Plotly (zoom, pan, hover tooltips, range selectors). Includes portfolio snapshot, lead/lag IR, correlation heatmap, drawdown, rolling returns, rolling volatility, return distribution, monthly heatmap.

HTML Reports — self-contained reports with embedded interactive charts and categorized metric tables, rendered via Jinja2 templates.

Requirements

- Python 3.11+

- numpy

- polars

- plotly

- scipy

Documentation

For detailed documentation, visit jQuantStats Documentation.

Contributing

Contributions are welcome! Please feel free to submit a Pull Request.

- Fork the repository

- Create your feature branch (

git checkout -b feature/amazing-feature) - Commit your changes (

git commit -m 'Add some amazing feature') - Push to the branch (

git push origin feature/amazing-feature) - Open a Pull Request

Citing

If you use jQuantStats in academic work or research reports, please cite it using the CITATIONS.bib file provided in this repository:

@software{jquantstats,

author = {Schmelzer, Thomas},

title = {jQuantStats: Portfolio Analytics for Quants},

url = {https://github.com/jebel-quant/jquantstats},

version = {0.4.0},

year = {2026},

license = {MIT}

}

License

This project is licensed under the MIT License - see the LICENSE file for details.

Project details

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file jquantstats-0.6.4.tar.gz.

File metadata

- Download URL: jquantstats-0.6.4.tar.gz

- Upload date:

- Size: 92.2 kB

- Tags: Source

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.12

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

c383f1e6dfdb66398a13cba3f718932068b16ee624717b2d1c1a20cd9129738c

|

|

| MD5 |

08aae5799a28eeb36960296448c00764

|

|

| BLAKE2b-256 |

89c1ca904d149294f83116fecaf4864847e0a4d3577203f0c39102a72e5e6d47

|

Provenance

The following attestation bundles were made for jquantstats-0.6.4.tar.gz:

Publisher:

rhiza_release.yml on Jebel-Quant/jquantstats

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

jquantstats-0.6.4.tar.gz -

Subject digest:

c383f1e6dfdb66398a13cba3f718932068b16ee624717b2d1c1a20cd9129738c - Sigstore transparency entry: 1280659367

- Sigstore integration time:

-

Permalink:

Jebel-Quant/jquantstats@5d509f3ef68aca063fa97cc0a6a5b158dc2886ac -

Branch / Tag:

refs/tags/v0.6.4 - Owner: https://github.com/Jebel-Quant

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

rhiza_release.yml@5d509f3ef68aca063fa97cc0a6a5b158dc2886ac -

Trigger Event:

push

-

Statement type:

File details

Details for the file jquantstats-0.6.4-py3-none-any.whl.

File metadata

- Download URL: jquantstats-0.6.4-py3-none-any.whl

- Upload date:

- Size: 104.4 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.12

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

ae6d04948ce8ab5320683678ff0bc3b896a373a76704d46d294c6bcf8bed8917

|

|

| MD5 |

2d9fd2ddbb0c06dd9fd0771e8c23a4d4

|

|

| BLAKE2b-256 |

3d86bc17f0188dc8f8907a1df3b22e6ffcf20069689e22eb9f8137d3b82a2939

|

Provenance

The following attestation bundles were made for jquantstats-0.6.4-py3-none-any.whl:

Publisher:

rhiza_release.yml on Jebel-Quant/jquantstats

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

jquantstats-0.6.4-py3-none-any.whl -

Subject digest:

ae6d04948ce8ab5320683678ff0bc3b896a373a76704d46d294c6bcf8bed8917 - Sigstore transparency entry: 1280659371

- Sigstore integration time:

-

Permalink:

Jebel-Quant/jquantstats@5d509f3ef68aca063fa97cc0a6a5b158dc2886ac -

Branch / Tag:

refs/tags/v0.6.4 - Owner: https://github.com/Jebel-Quant

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

rhiza_release.yml@5d509f3ef68aca063fa97cc0a6a5b158dc2886ac -

Trigger Event:

push

-

Statement type: