Dynamic MDF synthetic market data generator

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Project description

market-wave

Fast, lightweight synthetic market data from a Dynamic Market Distribution Function.

English | 한국어

market-wave is a Python library for generating synthetic market paths from

market-wide entry and exit intent. It does not create individual participants.

Instead, it models aggregate buy/sell entry intent, position exits,

order-book depth, cancellations, taker flow, and execution-driven price movement

from probability mass over relative ticks.

It is not a forecasting model. It is a lightweight simulation primitive for experiments, visualization, teaching, and strategy-environment prototyping.

Why market-wave?

- Aggregate intent, not agents: market participants are represented by probability mass over relative ticks, not by individual objects.

- Dynamic MDF: entry and exit intent live in four stateful

MDF(relative_tick)fields that evolve from the previous step. - Pluggable score model: swap the MDF score function with

DynamicMDFModelor a customMDFModel. - Separated shape and size: MDFs decide where intent sits; intensity decides how much order flow appears.

- Execution-driven prices: prices stay flat unless trades execute.

- Batch generation: generate many reproducible synthetic paths without

keeping every path in

market.history. - Inspectable state: every step returns a

StepInfosnapshot with MDFs, volumes, order book state, position mass, VWAP, spread, and imbalance. - Built-in plotting:

matplotlibis included, with a clean light chart style by default.

Install

pip install market-wave

For dataframe export:

pip install "market-wave[dataframe]"

For local development:

git clone https://github.com/smturtle2/market-wave.git

cd market-wave

uv sync --extra dev

Python >=3.10 is supported.

Quickstart

from market_wave import Market

market = Market(

initial_price=10_000,

gap=10,

popularity=1.0,

seed=42,

)

steps = market.step(500)

last = steps[-1]

print(last.price_before, "->", last.price_after)

print("entry:", round(sum(last.entry_volume_by_price.values()), 3))

print("executed:", round(last.total_executed_volume, 3))

print("resting bid/ask:", round(sum(last.orderbook_after.bid_volume_by_price.values()), 3), round(sum(last.orderbook_after.ask_volume_by_price.values()), 3))

print("imbalance:", round(last.order_flow_imbalance, 3))

Market.step(n) always returns list[StepInfo] and appends the same objects to

market.history.

For high-volume generation, skip in-memory history:

steps = market.step(512, keep_history=False)

for step in market.stream(512, keep_history=False):

consume(step)

For simple export workflows, use step.to_dict(), step.to_json(), or

market.history_records().

Example output with seed=42:

10020.0 -> 10010.0

entry: 2.955

executed: 0.976

resting bid/ask: 24.662 25.83

imbalance: 0.484

Smoke Matrix

The simulator is deterministic for a fixed seed, so it is easy to run the same invariants across different market conditions:

from market_wave import Market

cases = [

("baseline", dict(initial_price=10_000, gap=10, popularity=1.0, seed=42), 500),

("busy", dict(initial_price=10_000, gap=10, popularity=2.5, seed=7), 500),

("thin", dict(initial_price=500, gap=5, popularity=0.25, seed=123), 500),

("low_price", dict(initial_price=1, gap=1, popularity=3.0, seed=17), 500),

("trend_up", dict(initial_price=10_000, gap=10, popularity=1.0, seed=42, regime="trend_up"), 500),

("high_vol", dict(initial_price=10_000, gap=10, popularity=1.0, seed=7, regime="high_vol"), 500),

("inactive", dict(initial_price=100, gap=1, popularity=0.0, seed=9), 100),

]

for name, kwargs, steps_count in cases:

market = Market(**kwargs)

steps = market.step(steps_count)

prices = [step.price_after for step in steps]

move_steps = sum(step.price_change != 0 for step in steps)

exec_steps = sum(step.total_executed_volume > 0 for step in steps)

print(name, min(prices), max(prices), move_steps, exec_steps, market.state.price)

Recent verification on the current implementation:

baseline range= 9900.0- 10080.0 unique= 19 moves=369 exec_steps=500 final= 10010.0

busy range= 9890.0- 10030.0 unique= 15 moves=388 exec_steps=500 final= 9910.0

thin range= 455.0- 535.0 unique= 17 moves=318 exec_steps=500 final= 500.0

low_price range= 2.0- 24.0 unique= 23 moves=380 exec_steps=500 final= 19.0

trend_up range= 10000.0- 10320.0 unique= 33 moves=388 exec_steps=500 final= 10320.0

high_vol range= 9960.0- 10040.0 unique= 9 moves=405 exec_steps=500 final= 9970.0

inactive range= 100.0- 100.0 unique= 1 moves= 0 exec_steps= 0 final= 100.0

Those runs also checked that current-state MDF projections stay aligned with

state.price_grid, MDFs remain normalized, prices never fall below one tick,

order book and position mass stay non-negative, and price changes only occur on

steps with executed volume. Dynamic MDF acceptance also runs seeds 10..19 at

mdf_temperature=1.0 and checks that every MDF remains finite, non-negative,

normalized, and broad enough not to collapse to a single price.

Diagnostic note for 0.4.1: the simulator still has no anchor price or stored

target that pulls paths back to the initial price. Seeded mood, trend,

volatility, microstructure activity, cancellation pressure, and event pressure

evolve each step and reshape the MDFs and visible book. Prices remain

execution-driven, with a small flow-implied price-discovery component when

executed flow reveals one-sided pressure. Treat these ranges, move counts, and

execution counts as regression diagnostics, not claims that generated paths

match any specific real market.

Entry MDF prices are treated as incoming order prices. Buy entry orders arrive as bids, sell entry orders arrive as asks, and they execute only when they overlap existing opposite-side quotes. Executions print at the resting quote price. Unfilled volume remains in the book at the sampled MDF price. Exit flow is cohort-conditioned, so exit orders carry the originating cohort id and still route through visible order-book liquidity.

MDF note for 0.4.1: the default entry MDF now uses a side-relative

reservation-price mixture. Buy entry intent is spread across deep value,

passive bid, arrival, and small chase zones; sell entry intent mirrors that on

the ask side. This keeps passive limit interest in the MDF itself instead of

adding synthetic fixed walls, while reducing excessive buy-ask and sell-bid

tail mass.

Microstructure note for 0.4.0: order-book replenishment now includes

regime-specific depth shape, resiliency, wall memory by absolute tick,

event-driven volume bursts, dry-up after cancellation pressure, trend

exhaustion, and squeeze pressure derived from short crowding plus recent

one-sided flow. Live order-book and position totals remain cached by price/side,

lots are coalesced by price/kind, and position inventory is kept in bounded

entry-price cohort buckets.

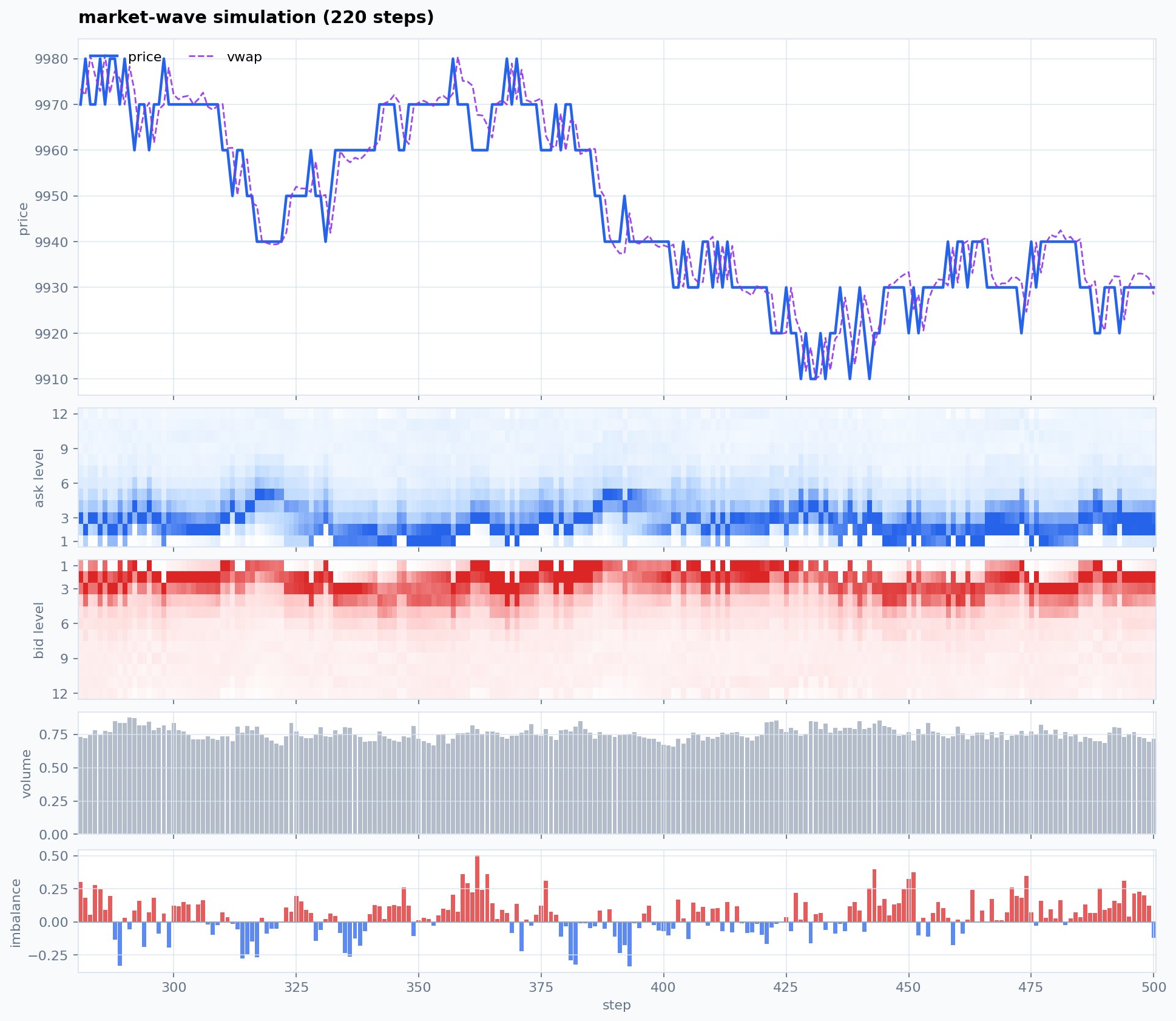

Visualization

from market_wave import Market

market = Market(

initial_price=10_000,

gap=10,

popularity=1.0,

seed=42,

)

market.step(500)

fig, ax = market.plot(last=220, orderbook_depth=12)

The default market_wave style uses a light multi-panel chart: price/VWAP,

bid and ask orderbook depth heatmaps by simple level, executed volume, and

order-flow imbalance. To keep the legacy three-panel view, pass

orderbook=False.

Dark overlay mode is still available:

fig, ax = market.plot(layout="overlay", style="market_wave_dark")

Synthetic Data

from market_wave import compute_metrics, generate_paths

paths = generate_paths(

n_paths=100,

horizon=512,

config_sampler=lambda path_id: {

"initial_price": 10_000,

"gap": 10,

"popularity": 1.0,

"seed": 10_000 + path_id,

},

)

metrics = compute_metrics(paths)

print(metrics.return_std, metrics.volume_mean, metrics.max_drawdown)

print(paths[0].metadata.config_hash)

GeneratedPath.metadata stores seed, config_hash, package version,

regime, and augmentation_strength so synthetic runs can be traced. Pandas is

optional: install market-wave[dataframe] to use to_dataframe().

ValidationMetrics.volatility_clustering_score is computed within each generated

path and aggregated, so independent path boundaries do not affect the diagnostic.

Pluggable MDF

from market_wave import Market

class CenterSeekingMDF:

def scores(self, side, intent, relative_ticks, context, signals=None):

del side, intent, context, signals

return [-abs(tick) for tick in relative_ticks]

market = Market(initial_price=100, gap=1, mdf_model=CenterSeekingMDF(), seed=7)

step = market.step(1)[0]

print(step.relative_ticks)

print(step.buy_entry_mdf)

Custom MDF models return scores, not probabilities. Treat each score as

log-growth evidence: additive score differences become multiplicative changes

to the previous MDF. Market applies those scores through the stabilized MDF

update described below.

Core Concepts

At every step, the market builds relative ticks around the current price:

relative_tick = (price - current_price) / tick_size

relative_ticks = [-grid_radius, ..., 0, ..., +grid_radius]

The simulator maintains four Market Distribution Functions on that relative grid:

buy_entry_mdfsell_entry_mdflong_exit_mdfshort_exit_mdf

Each MDF is normalized. It is not recreated from scratch each step; it evolves from the previous MDF:

logits = persistence * log(MDF_prev(tick) + eps)

+ score(tick) / effective_temperature

proposal = softmax(clamp(logits - max(logits), -50, 0))

MDF_next = Normalize((1 - floor_mix) * Diffuse(proposal) + floor_mix * Uniform)

score(tick) can include placement shape, trend, liquidity attraction, memory,

risk, and order-book imbalance. mdf_temperature controls how sharply scores

reshape the distribution. The effective temperature also includes current volatility, so

high-volatility regimes soften score updates instead of letting one tick absorb

all mass. Persistence, diffusion, and uniform floor mixing prevent repeated

small score advantages from collapsing the MDF into a single tick.

Those relative MDFs are projected onto the pre-trade grid

price_grid = price_before +/- k * gap for order-book formation.

StepInfo.mdf_price_basis records that pre-trade price basis.

low temperature -> sharper, concentrated MDF

high temperature -> wider, smoother MDF

MDFs generate aggregate intent. Intensity controls total size. The order book and execution layer then turn that intent into limit flow, taker flow, cancellations, exits, matched volume, and price changes.

Execution Guarantee

Price movement is execution-driven:

- If a step has no executed volume,

price_after == price_before. - If trades execute,

price_afteris derived from that step's execution statistics. Random quote jitter is bounded and cannot move the price by itself when executions print at the previous price. seedmakes the simulation reproducible for the same version and inputs.

This is a simulator, not a market data replay engine and not financial advice.

API Overview

from market_wave import (

Market,

DynamicMDFModel,

generate_paths,

compute_metrics,

MarketState,

IntensityState,

LatentState,

MDFContext,

MDFSignals,

MDFModel,

RelativeMDFComponent,

MDFState,

OrderBookState,

PositionMassState,

StepInfo,

)

Useful StepInfo fields include:

price_before,price_after,price_changetick_before,tick_after,tick_change,relative_ticksmdf_price_basis,price_gridbuy_entry_mdf,sell_entry_mdf,long_exit_mdf,short_exit_mdfbuy_entry_mdf_by_price,sell_entry_mdf_by_priceentry_volume_by_price,exit_volume_by_pricebuy_volume_by_price,sell_volume_by_priceexecuted_volume_by_price,total_executed_volume,trade_countmarket_buy_volume,market_sell_volumevwap_price,best_bid_before,best_ask_before,spread_afterorderbook_before,orderbook_afterposition_mass_before,position_mass_after

buy_volume_by_price and sell_volume_by_price are submitted side-intent maps

keyed by sampled order price, not executed or resting liquidity. market_*

volume fields report the executed incoming buy/sell volume. Unfilled incoming

volume rests in orderbook_after; legacy residual_market_* and

crossed_market_volume fields remain compatibility zeroes in the current

order-book-first engine.

The *_mdf_by_price fields are pre-trade MDF projections keyed by

mdf_price_basis; current Market.state.mdf.*_by_price is reprojected to the

post-trade state price. Examples and public APIs use MDF names only; stale PMF

examples from earlier prototypes should be considered obsolete.

Public Contract and Snapshot Policy

The public import surface is the package __all__: Market, generate_paths,

compute_metrics, generated-path metadata, MDF model/protocol types, metrics,

and the state dataclasses shown above. The entrypoints are intentionally small,

but the observation contract is broad because StepInfo and MarketState

expose detailed simulator diagnostics.

During the current alpha line, existing public names and existing StepInfo /

state fields are kept compatible where practical. New diagnostic fields may be

added in alpha releases. MDF names are the supported public distribution names;

stale PMF names from earlier prototypes are obsolete.

Snapshot mutability: state dataclasses are frozen=True at the attribute level,

but nested dict and list fields are plain mutable containers so to_dict()

and JSON export remain simple. Treat Market.state, StepInfo, and

GeneratedPath.hidden_states as read-only observations. Use Market.snapshot()

when downstream code needs a mutation-safe deep copy of the current state.

Compatibility note: Market.state remains available as the live current-state

attribute for the alpha line. Future releases may add a more explicit read-model

API or deprecation path for code that mutates state containers in place.

Development

uv sync --extra dev --extra dataframe

uv run ruff check .

uv run pytest

uv build

License

MIT

Project details

Verified details

These details have been verified by PyPIProject links

GitHub Statistics

Maintainers

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file market_wave-0.4.1.tar.gz.

File metadata

- Download URL: market_wave-0.4.1.tar.gz

- Upload date:

- Size: 1.9 MB

- Tags: Source

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.12

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

b5426b6ec7a57c2fec5f7dc55587161809a4809d68df64dfcc6fae02a18760e2

|

|

| MD5 |

41069fdbe59ce4ffdf46035f65a1997e

|

|

| BLAKE2b-256 |

bd78752cb43c4c678d6a6b85d8dcb3a3153bcde03bd006a2ebb5fb4d84bc6ba2

|

Provenance

The following attestation bundles were made for market_wave-0.4.1.tar.gz:

Publisher:

workflow.yml on smturtle2/market-wave

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

market_wave-0.4.1.tar.gz -

Subject digest:

b5426b6ec7a57c2fec5f7dc55587161809a4809d68df64dfcc6fae02a18760e2 - Sigstore transparency entry: 1393055269

- Sigstore integration time:

-

Permalink:

smturtle2/market-wave@b288a595afd4b99efbb735fdc5973fb1adbd5f11 -

Branch / Tag:

refs/tags/v0.4.1 - Owner: https://github.com/smturtle2

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

workflow.yml@b288a595afd4b99efbb735fdc5973fb1adbd5f11 -

Trigger Event:

push

-

Statement type:

File details

Details for the file market_wave-0.4.1-py3-none-any.whl.

File metadata

- Download URL: market_wave-0.4.1-py3-none-any.whl

- Upload date:

- Size: 35.4 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? Yes

- Uploaded via: twine/6.1.0 CPython/3.13.12

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

3bc6dfb9aefc86690f241f5470e80e986f2f5a02fc12861ba7aa3d7733b3f534

|

|

| MD5 |

c8701e2827caf84ee60295448e3f453a

|

|

| BLAKE2b-256 |

dc4d6815f1f0b84d5ab47a1f478da659acddfe6d4906a5f218e577587be543e6

|

Provenance

The following attestation bundles were made for market_wave-0.4.1-py3-none-any.whl:

Publisher:

workflow.yml on smturtle2/market-wave

-

Statement:

-

Statement type:

https://in-toto.io/Statement/v1 -

Predicate type:

https://docs.pypi.org/attestations/publish/v1 -

Subject name:

market_wave-0.4.1-py3-none-any.whl -

Subject digest:

3bc6dfb9aefc86690f241f5470e80e986f2f5a02fc12861ba7aa3d7733b3f534 - Sigstore transparency entry: 1393055275

- Sigstore integration time:

-

Permalink:

smturtle2/market-wave@b288a595afd4b99efbb735fdc5973fb1adbd5f11 -

Branch / Tag:

refs/tags/v0.4.1 - Owner: https://github.com/smturtle2

-

Access:

public

-

Token Issuer:

https://token.actions.githubusercontent.com -

Runner Environment:

github-hosted -

Publication workflow:

workflow.yml@b288a595afd4b99efbb735fdc5973fb1adbd5f11 -

Trigger Event:

push

-

Statement type: