Compute technical indicators and build trade strategies in a simple way

Project description

simple-trade

A Python library that allows you to compute technical indicators and build trade strategies in a simple way.

Features

- Data Fetching: Easily download historical stock data using

yfinance. - Technical Indicators: Compute a variety of technical indicators:

- Trend (e.g., Moving Averages, MACD, ADX)

- Momentum (e.g., RSI, Stochastics)

- Volatility (e.g., Bollinger Bands, ATR)

- Volume (e.g., On-Balance Volume)

- Trading Strategies: Implement and backtest common trading strategies:

- Cross Trade Strategies (

cross_trade) - Band Trading Strategies (

band_trade)

- Cross Trade Strategies (

- Backtesting: Evaluate the performance of your trading strategies on historical data.

- Optimization: Optimize strategy parameters using techniques like grid search.

- Plotting: Visualize data, indicators, and backtest results using

matplotlib.

Installation

- Clone the repository:

git clone <repository_url> # Replace with your repo URL cd simple-trade

- Create and activate a virtual environment (recommended):

python -m venv myenv # On Windows myenv\Scripts\activate # On macOS/Linux source myenv/bin/activate

- Install the package and dependencies:

pip install .

Alternatively, installed with PyPI:pip install simple-trade

Dependencies

- Python >= 3.10

- yfinance

- pandas

- numpy

- joblib

- matplotlib

These will be installed automatically when you install simple-trade using pip.

Basic Usage

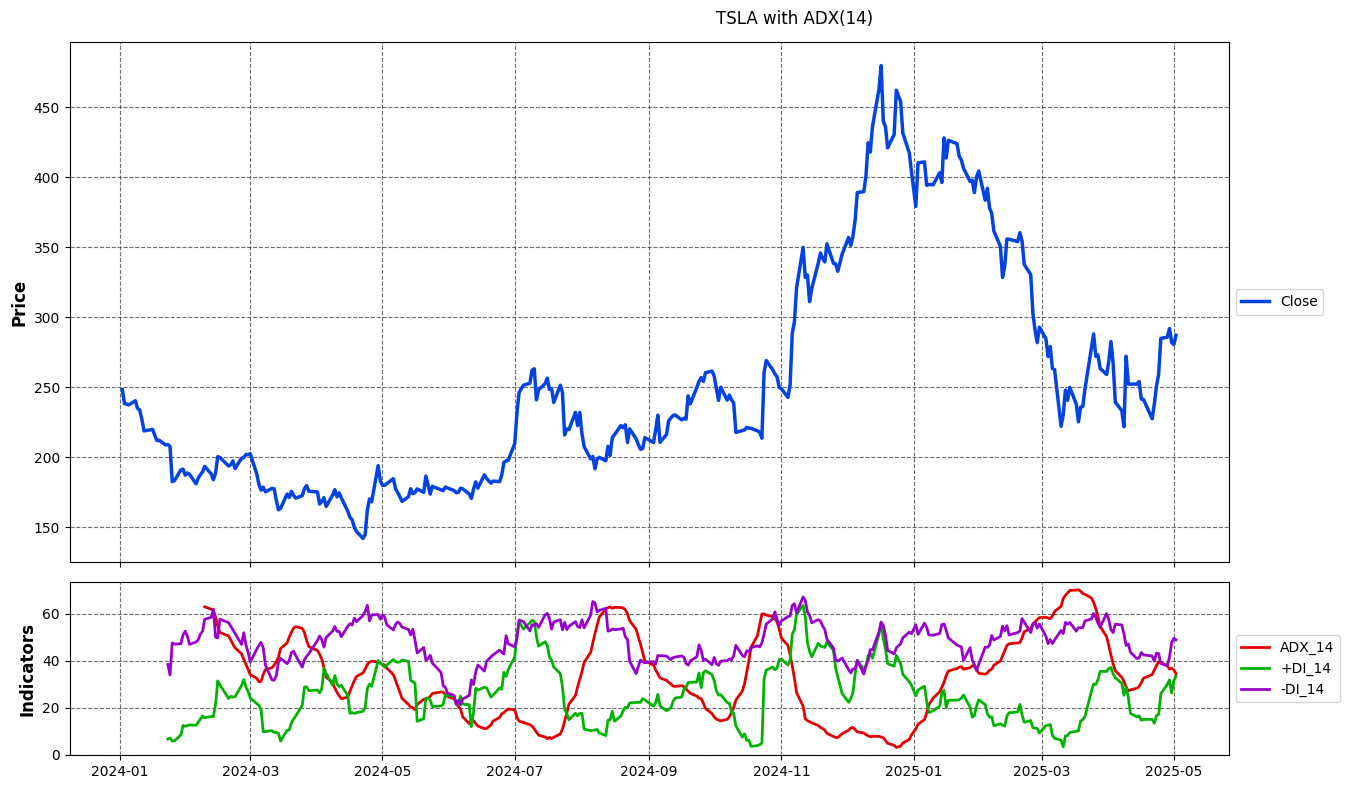

Here's a quick example of how to download data and compute a technical indicator:

# Load Packages and Functions

import pandas as pd

from simple_trade import compute_indicator, download_data

from simple_trade import IndicatorPlotter

# Step 1: Download data

symbol = 'TSLA'

start = '2024-01-01'

end = '2025-01-01'

interval = '1d'

print(f"\nDownloading data for {symbol}...")

data = download_data(symbol, start, end, interval=interval)

# Step 2: Calculate indicator

parameters = dict()

columns = dict()

parameters["window"] = 14

columns["high_col"] = 'High'

columns["low_col"] = 'Low'

columns["close_col"] = 'Close'

data = compute_indicator(

data=data,

indicator='adx',

parameters=parameters,

columns=columns

)

# Step 3: Plot the indicator

plotter = IndicatorPlotter()

window = parameters["window"]

columns = [f'ADX_{window}', f'+DI_{window}', f'-DI_{window}']

fig = plotter.plot_results(

data,

price_col='Close',

column_names=columns,

plot_on_subplot=True,

title=f"{symbol} with ADX({window})"

)

# Step 4: Display the plot

fig.show()

Plot of Results

Advanced Usage

Backtesting Strategies

Use the backtesting module to simulate strategies like moving average crossovers (cross_trade) or Bollinger Band breakouts (band_trade).

# Load Packages and Functions

import pandas as pd

from simple_trade import download_data, compute_indicator

from simple_trade import CrossTradeBacktester

from simple_trade import BacktestPlotter

# Step 1: Download data

symbol = 'AAPL'

start_date = '2020-01-01'

end_date = '2022-12-31'

interval = '1d'

data = download_data(symbol, start_date, end_date, interval=interval)

# Step 2: Download indicators

short_window = 25

long_window = 75

data = compute_indicator(data, indicator='sma', window=short_window)

data = compute_indicator(data, indicator='sma', window=long_window)

# Step 3: Initialize strategy

initial_cash = 10000.0

commission = 0.01

backtester = CrossTradeBacktester(initial_cash=initial_cash, commission_long=commission)

results, portfolio = backtester.run_cross_trade(

data=data,

short_window_indicator="SMA_25",

long_window_indicator="SMA_75",

price_col='Close',

)

# Step 4: Produce results

backtester.print_results(results)

# Step 5: Plot results

plotter = BacktestPlotter()

indicator_cols_to_plot = [f'SMA_{short_window}', f'SMA_{long_window}']

fig = plotter.plot_results(

data_df=data,

history_df=portfolio,

price_col='Close',

indicator_cols=indicator_cols_to_plot,

title=f"Cross Trade (Long Only) (SMA-{short_window} vs SMA-{long_window})"

)

# Step 6: Display the plot

plt.show()

Output of Results

============================================================

✨ Cross Trade (SMA_25/SMA_75) ✨

============================================================

🗓️ BACKTEST PERIOD:

• Period: 2020-04-20 to 2022-12-30

• Duration: 984 days

• Trading Days: 682

📊 BASIC METRICS:

• Initial Investment: $10,000.00

• Final Portfolio Value: $11,400.77

• Total Return: 14.01%

• Annualized Return: 4.96%

• Number of Trades: 16

• Total Commissions: $1,936.74

📈 BENCHMARK COMPARISON:

• Benchmark Return: 71.32%

• Benchmark Final Value: $17,132.49

• Strategy vs Benchmark: -57.31%

📉 RISK METRICS:

• Sharpe Ratio: 0.320

• Sortino Ratio: 0.260

• Maximum Drawdown: -33.59%

• Average Drawdown: -15.36%

• Max Drawdown Duration: 849 days

• Avg Drawdown Duration: 61.33 days

• Annualized Volatility: 23.75%

Plot of Results

Optimizing Strategies

The optimizer module allows you to find the best parameters for your strategy (e.g., optimal moving average windows).

# Load Packages and Functions

from simple_trade import download_data, compute_indicator

from simple_trade import CrossTradeBacktester

from simple_trade import Optimizer

# Step 1: Load Data

ticker = "AAPL"

start_date = "2020-01-01"

end_date = "2023-12-31"

data = download_data(ticker, start_date, end_date)

# Step 2: Load Optimization Parameters

# Define the parameter grid to search

param_grid = {

'short_window': [10, 20, 30],

'long_window': [50, 100, 150],

}

# Define constant parameters for the backtester

initial_capital = 100000

commission_fee = 0.001 # 0.1%

constant_params = {

'initial_cash': initial_capital,

'commission_long': commission_fee,

'price_col': 'Close'

}

# Define the metric to optimize and whether to maximize or minimize

metric_to_optimize = 'total_return_pct'

maximize_metric = True

# Step 3: Define the wrapper function

def run_cross_trade_with_windows(data, short_window, long_window, **kwargs):

# Work on a copy of the data

df = data.copy()

# Compute the SMA indicators

df = compute_indicator(df, indicator='sma', parameters={'window': short_window}, columns={'close_col': 'Close'})

df = compute_indicator(df, indicator='sma', parameters={'window': long_window}, columns={'close_col': 'Close'})

# Get the indicator column names

short_window_indicator = f"SMA_{short_window}"

long_window_indicator = f"SMA_{long_window}"

# Create a backtester instance

backtester = CrossTradeBacktester(

initial_cash=kwargs.pop('initial_cash', 10000),

commission_long=kwargs.pop('commission_long', 0.001),

)

# Run the backtest

return backtester.run_cross_trade(

data=df,

short_window_indicator=short_window_indicator,

long_window_indicator=long_window_indicator,

**kwargs

)

# Step 4: Instantiate and Run Optimizer

print("Initializing Optimizer...")

optimizer = Optimizer(

data=data,

backtest_func=run_cross_trade_with_windows, # Use our wrapper function

param_grid=param_grid,

metric_to_optimize=metric_to_optimize,

maximize_metric=maximize_metric,

constant_params=constant_params

)

print("\nRunning Optimization (Parallel)...")

# Run optimization with parallel processing (adjust n_jobs as needed)

results = optimizer.optimize(parallel=True, n_jobs=-1) # n_jobs=-1 uses all available cores

# --- Display Results ---

print("\n--- Optimization Results ---")

# Unpack results

best_params, best_metric_value, all_results = results

print("\n--- Top 5 Parameter Combinations ---")

# Sort results for display

sorted_results = sorted(all_results, key=lambda x: x[1], reverse=maximize_metric)

for i, (params, metric_val) in enumerate(sorted_results[:5]):

print(f"{i+1}. Params: {params}, Metric: {metric_val:.4f}")

Output of Results

print("\nRunning Optimization (Parallel)...")

# Run optimization with parallel processing (adjust n_jobs as needed)

results = optimizer.optimize(parallel=True, n_jobs=-1) # n_jobs=-1 uses all available cores

# --- Display Results ---

print("\n--- Optimization Results ---")

# Unpack results

best_params, best_metric_value, all_results = results

print("\n--- Top 5 Parameter Combinations ---")

# Sort results for display

sorted_results = sorted(all_results, key=lambda x: x[1], reverse=maximize_metric)

for i, (params, metric_val) in enumerate(sorted_results[:5]):

print(f"{i+1}. Params: {params}, Metric: {metric_val:.4f}")

Initializing Optimizer...

Generated 9 parameter combinations.

Running Optimization (Parallel)...

Starting optimization for 9 combinations...

Metric: total_return_pct (Maximize) | Parallel: True (n_jobs=-1)

Using 16 parallel jobs.

[Parallel(n_jobs=16)]: Using backend LokyBackend with 16 concurrent workers.

[Parallel(n_jobs=16)]: Done 2 out of 9 | elapsed: 9.0s remaining: 31.6s

[Parallel(n_jobs=16)]: Done 4 out of 9 | elapsed: 9.4s remaining: 11.7s

[Parallel(n_jobs=16)]: Done 6 out of 9 | elapsed: 9.5s remaining: 4.7s

Optimization finished in 9.86 seconds.

Best Parameters found: {'short_window': 10, 'long_window': 50}

Best Metric Value (total_return_pct): 89.0500

--- Optimization Results ---

--- Top 5 Parameter Combinations ---

1. Params: {'short_window': 10, 'long_window': 50}, Metric: 89.0500

2. Params: {'short_window': 20, 'long_window': 50}, Metric: 76.6100

3. Params: {'short_window': 30, 'long_window': 50}, Metric: 60.6400

4. Params: {'short_window': 10, 'long_window': 150}, Metric: 19.4100

5. Params: {'short_window': 20, 'long_window': 100}, Metric: 10.9600

[Parallel(n_jobs=16)]: Done 9 out of 9 | elapsed: 9.7s finished

Examples

For more detailed examples, please refer to the Jupyter notebooks in the /examples directory:

/examples/indicators: Demonstrations of various technical indicators./examples/backtest: Examples of backtesting different strategies./examples/optimize: Examples of optimizing strategy parameters.

Contributing

Contributions are welcome! Please feel free to submit a pull request or open an issue. (Further details can be added here if needed).

License

This project is licensed under the AGPL-3.0 License - see the LICENSE file for details.

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file simple_trade-0.1.2.tar.gz.

File metadata

- Download URL: simple_trade-0.1.2.tar.gz

- Upload date:

- Size: 5.3 MB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.11.4

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

68f972265d194cf038cb7853cae6fb9871be9e3b51b4179a4d16f295313cc88c

|

|

| MD5 |

13b8b0c5c3e7cbaed25b040f9d97ab6f

|

|

| BLAKE2b-256 |

49028fa477cbf87943c38f88412e88e0669fe52fa5750a767e18373cf9ed2f5e

|

File details

Details for the file simple_trade-0.1.2-py3-none-any.whl.

File metadata

- Download URL: simple_trade-0.1.2-py3-none-any.whl

- Upload date:

- Size: 84.0 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/6.1.0 CPython/3.11.4

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

eda09ebfcf1e8254162aea5d8167da228b6296b2c8359cbdabc61af349f1c519

|

|

| MD5 |

866e9f096e88404ac43b139e4e510d1c

|

|

| BLAKE2b-256 |

20d3f7c4cfab1952e1b916c73824f029d75428dbc1d9d1f244cea1ccb5c20ff6

|