Riskfolio-Lib: Quantitative Strategic Asset Allocation, easy for you

Project description

Riskfolio-Lib

Quantitative Strategic Asset Allocation, easy for you.

Description

Riskfolio-Lib is a library for making quantitative strategic asset allocation or portfolio optimization in Python. It is built on top of cvxpy and closely integrated with pandas data structures.

Some of key functionality that Riskfolio-Lib offers:

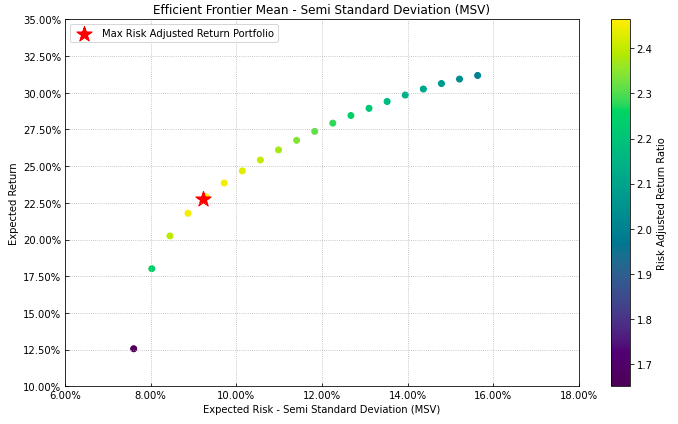

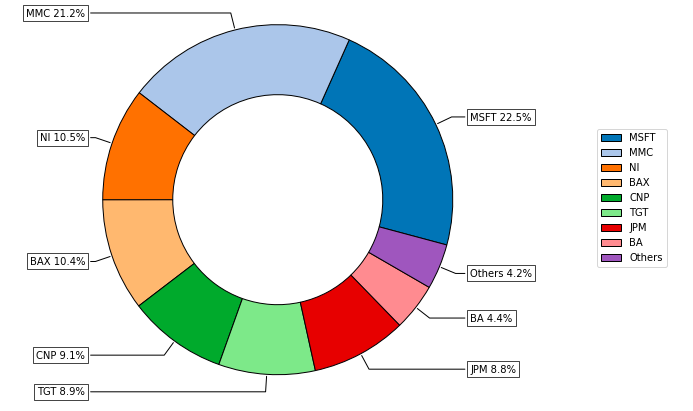

- Portfolio optimization with 4 objective functions (Minimum Risk, Maximum Return, Maximum Risk Adjusted Return Ratio and Maximum Utility Function)

- Portfolio optimization with 10 convex risk measures (Std. Dev., MAD, CVaR, Maximum Drawdown, among others)

- Portfolio optimization with Black Litterman model.

- Portfolio optimization with Risk Factors model.

- Portfolio optimization with constraints on tracking error and turnover.

- Portfolio optimization with short positions and leverage.

- Tools for construct efficient frontier for 10 risk measures.

- Tools for construct linear constraints on assets, asset classes and risk factors.

- Tools for construct views on assets and asset classes.

- Tools for calculate risk measures.

- Tools for visualizing portfolio properties and risk measures.

Documentation

Online documentation is available at Documentation.

The docs include a tutorial with examples that shows the capacities of Riskfolio-Lib.

Dependencies

Riskfolio-Lib supports Python 3.6+.

Installation requires:

- numpy >= 1.17.0

- scipy >= 1.0.1

- pandas >= 1.0.0

- matplotlib >= 3.0.0

- cvxpy >= 1.0.15

- scikit-learn >= 0.22.0

- statsmodels >= 0.10.1

Installation

The latest stable release (and older versions) can be installed from PyPI:

pip install riskfolio-lib

Development

Riskfolio-Lib development takes place on Github: https://github.com/dcajasn/Riskfolio-Lib

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file Riskfolio-Lib-0.0.2.tar.gz.

File metadata

- Download URL: Riskfolio-Lib-0.0.2.tar.gz

- Upload date:

- Size: 2.7 MB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/3.1.1 pkginfo/1.5.0.1 requests/2.22.0 setuptools/42.0.2.post20191203 requests-toolbelt/0.9.1 tqdm/4.40.2 CPython/3.7.5

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

ded371a73127aae9bd062fd91277becbefa45e9ce8402597b1ce7e555fa0cc24

|

|

| MD5 |

92221d2e6b28c03af82fc254f636792a

|

|

| BLAKE2b-256 |

c2aa121459a75fe41c29165260da32f15ce00511dd3e84607a7f00e24f0b4b6c

|

File details

Details for the file Riskfolio_Lib-0.0.2-py3-none-any.whl.

File metadata

- Download URL: Riskfolio_Lib-0.0.2-py3-none-any.whl

- Upload date:

- Size: 29.1 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: twine/3.1.1 pkginfo/1.5.0.1 requests/2.22.0 setuptools/42.0.2.post20191203 requests-toolbelt/0.9.1 tqdm/4.40.2 CPython/3.7.5

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

8e4b08f4430e999b5037052be6afce780ae80a55b245159261cfe610bc2c9bce

|

|

| MD5 |

00405ea61c693739f506acc594ba954c

|

|

| BLAKE2b-256 |

84f2f8dd68228a1ead45dacc1f51fbbe3324fa164c75cd1bf85e0b0992efdfab

|