RiskOptima is a powerful Python toolkit for financial risk analysis, portfolio optimization, and advanced quantitative modeling. It integrates state-of-the-art methodologies, including Monte Carlo simulations, Value at Risk (VaR), Conditional VaR (CVaR), Black-Scholes, Heston, and Merton Jump Diffusion models, to aid investors in making data-driven investment decisions.

Project description

RiskOptima

RiskOptima is a comprehensive Python toolkit for evaluating, managing, and optimizing investment portfolios. This package is designed to empower investors and data scientists by combining financial risk analysis, backtesting, mean-variance optimization, and machine learning capabilities into a single, cohesive package.

Stats

https://pypistats.org/packages/riskoptima

Key Features

- Modular Core:

MarketData,Portfolio, andBacktestConfigtypes for clean workflows. - Backtesting Framework: Strategy interfaces, cost/slippage modeling, and performance tracking.

- Risk Models: Factor risk model with exposures and factor-based covariance estimation.

- Optimization: Mean-variance, efficient frontier, max Sharpe, and constraint handling (bounds, leverage, turnover, factor limits).

- Risk Management: VaR, CVaR, volatility, and drawdown analytics.

- Monte Carlo Simulations: Analyze potential portfolio outcomes. See example here https://github.com/JordiCorbilla/efficient-frontier-monte-carlo-portfolio-optimization

- Market & Allocation Visuals: Correlation matrices, portfolio area charts, and diagnostics.

- Quant Models: Black-Litterman, stochastic volatility models, and options/Greeks analytics.

- Portfolio Projects: algorithmic trading/backtesting, portfolio optimization, market risk dashboard, option pricing engine, and credit risk model workflows.

Quant Portfolio Project Map

| Project | Notebook / Example | Package API | Screenshot |

|---|---|---|---|

| Algorithmic Trading Backtester | 05-portfolio_sma_strategy.ipynb |

riskoptima.backtest |

|

| Portfolio Optimization | 02-portfolio_optimization_riskoptima.ipynb |

riskoptima.optim |

|

| Market Risk Dashboard | examples/example_market_risk_dashboard.py |

riskoptima.reporting |

|

| Option Pricing Engine | examples/example_option_pricing_engine.py |

riskoptima.options |

|

| Credit Risk Model | 08-credit_risk_model_demo.ipynb |

riskoptima.credit |

|

See docs/quant_project_map.md for a recruiter/interviewer-friendly walkthrough of the five projects.

Installation

See the project here: https://pypi.org/project/riskoptima/

pip install riskoptima

Usage

New modular API (backtest + factor risk + constraints)

import pandas as pd

from riskoptima import FactorRiskModel, Constraints, optimize_max_sharpe

from riskoptima import SMACrossStrategy, run_backtest, BacktestConfig, SimpleCostModel

# prices: DataFrame with Date index and asset columns

prices = pd.read_csv("prices.csv", index_col=0, parse_dates=True)

asset_returns = prices.pct_change().dropna()

# factors: Fama-French returns DataFrame (e.g. from RiskOptima.get_fff_returns)

factors = pd.read_csv("fama_french_factors.csv", index_col=0, parse_dates=True)

factor_model = FactorRiskModel(factor_returns=factors).fit(asset_returns)

factor_cov = factor_model.covariance_matrix()

constraints = Constraints(factor_bounds={"MKT": (-0.2, 0.8)})

weights = optimize_max_sharpe(

expected_returns=asset_returns.mean() * 252,

cov=factor_cov,

constraints=constraints,

factor_exposures=factor_model.exposures,

risk_free_rate=0.02,

)

strategy = SMACrossStrategy(short_window=20, long_window=50)

config = BacktestConfig(initial_cash=1_000_000, rebalance_rule="D")

cost_model = SimpleCostModel(spread_bps=2.0, impact_coeff=0.0)

equity_curve, weights_history = run_backtest(prices, strategy, config, cost_model)

See examples/example_factor_backtest.py for a runnable end-to-end example.

Offline sample datasets

RiskOptima includes small synthetic datasets for deterministic examples:

data/synthetic_market_returns.csvdata/synthetic_credit_portfolio.csv

These are intentionally small and have no external data dependency.

Credit Risk Model

RiskOptima includes a production-ready credit risk layer for PD/LGD/EAD portfolios, expected loss, unexpected loss, rating migration, Merton structural default probability, and Credit VaR/CVaR Monte Carlo.

import pandas as pd

from riskoptima.credit import (

expected_loss,

portfolio_expected_loss,

simulate_credit_losses,

credit_var,

credit_cvar,

merton_pd,

)

portfolio = pd.DataFrame({

"obligor": ["A", "B", "C"],

"PD": [0.01, 0.025, 0.04],

"LGD": [0.40, 0.45, 0.55],

"EAD": [1_000_000, 750_000, 500_000],

})

print(expected_loss(0.02, 0.45, 1_000_000))

print(portfolio_expected_loss(portfolio))

losses = simulate_credit_losses(portfolio, n_sims=20_000, random_state=42)

print(credit_var(losses, confidence=0.99))

print(credit_cvar(losses, confidence=0.99))

print(merton_pd(asset_value=150, debt_face_value=100, asset_vol=0.25, risk_free_rate=0.03, maturity=1.0))

See 08-credit_risk_model_demo.ipynb for an end-to-end notebook.

Market Risk Dashboard

RiskOptima can build a dashboard-ready market risk report with annualized return, volatility, Sharpe, Sortino, drawdown, historical VaR, Gaussian VaR, CVaR/expected shortfall, beta, tracking error, information ratio, rolling volatility, and rolling drawdown.

Screenshot placeholder: plots/market_risk_dashboard.png

import pandas as pd

from riskoptima.reporting import build_market_risk_report

returns = pd.DataFrame({

"AssetA": [0.01, -0.005, 0.004, 0.002],

"AssetB": [0.002, 0.003, -0.006, 0.005],

})

weights = pd.Series({"AssetA": 0.6, "AssetB": 0.4})

report = build_market_risk_report(returns, weights=weights, confidence_levels=(0.95, 0.99))

print(report.metrics["annualized_volatility"])

print(report.metrics["historical_var"][0.99])

Run examples/example_market_risk_dashboard.py to generate a multi-panel dashboard.

Optional Streamlit dashboard:

pip install streamlit

streamlit run examples/streamlit_market_risk_dashboard.py

Option Pricing Engine

The clean options API covers Black-Scholes call/put pricing, Greeks, implied volatility, binomial trees, and Monte Carlo European option pricing while preserving the legacy RiskOptima class methods.

import pandas as pd

from riskoptima.options import (

black_scholes_price,

black_scholes_greeks,

implied_volatility,

monte_carlo_european_option,

)

S, K, T, r, sigma = 100, 100, 1.0, 0.05, 0.20

call = black_scholes_price(S, K, T, r, sigma, option_type="call")

put = black_scholes_price(S, K, T, r, sigma, option_type="put")

greeks = pd.Series(black_scholes_greeks(S, K, T, r, sigma, option_type="call"))

iv = implied_volatility(call, S, K, T, r, option_type="call")

mc = monte_carlo_european_option(S, K, T, r, sigma, option_type="call", random_state=42)

print(call, put)

print(greeks)

print(iv, mc)

Run examples/example_option_pricing_engine.py for a full pricing comparison.

Example 1: Setting up your portfolio

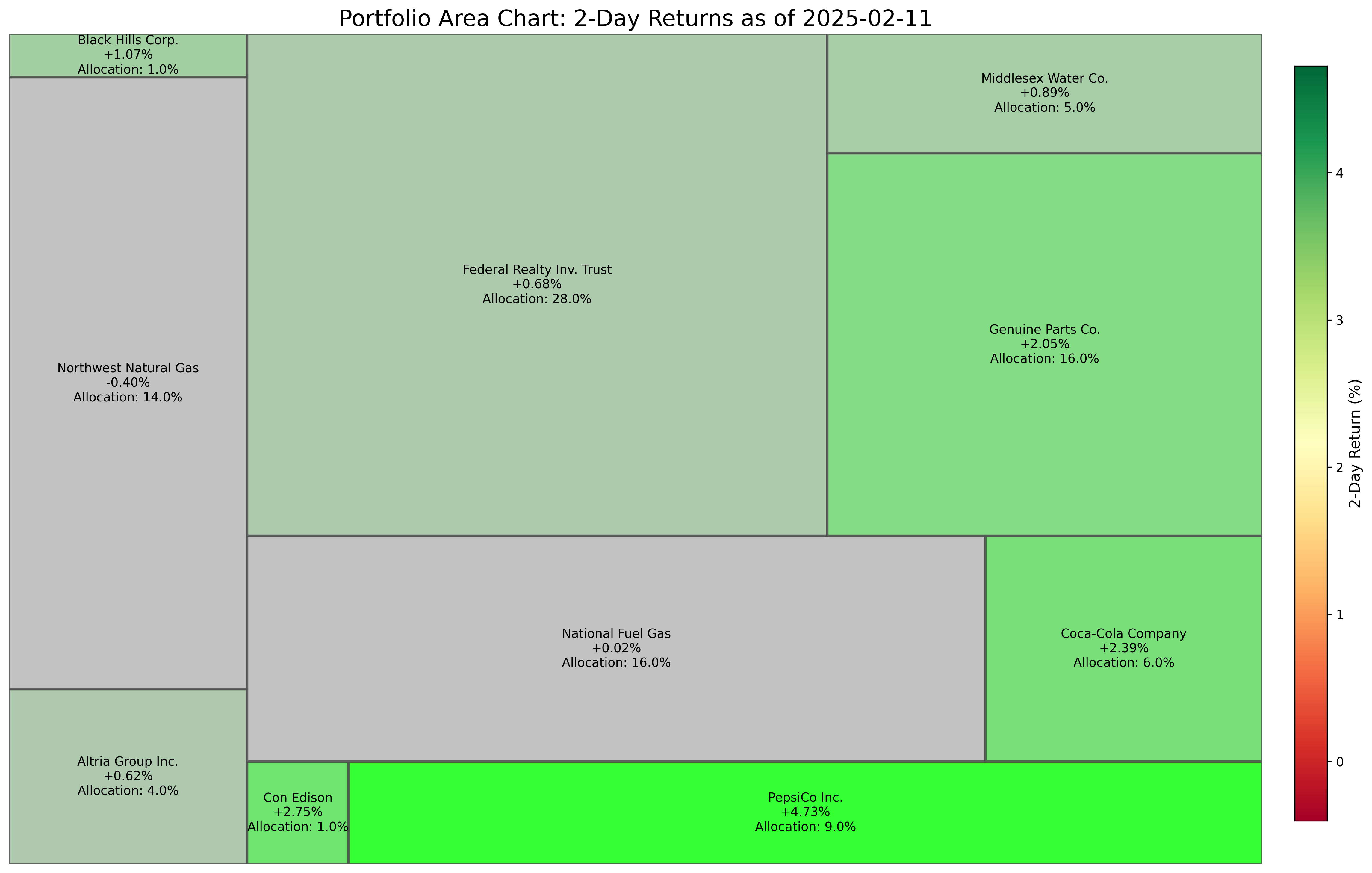

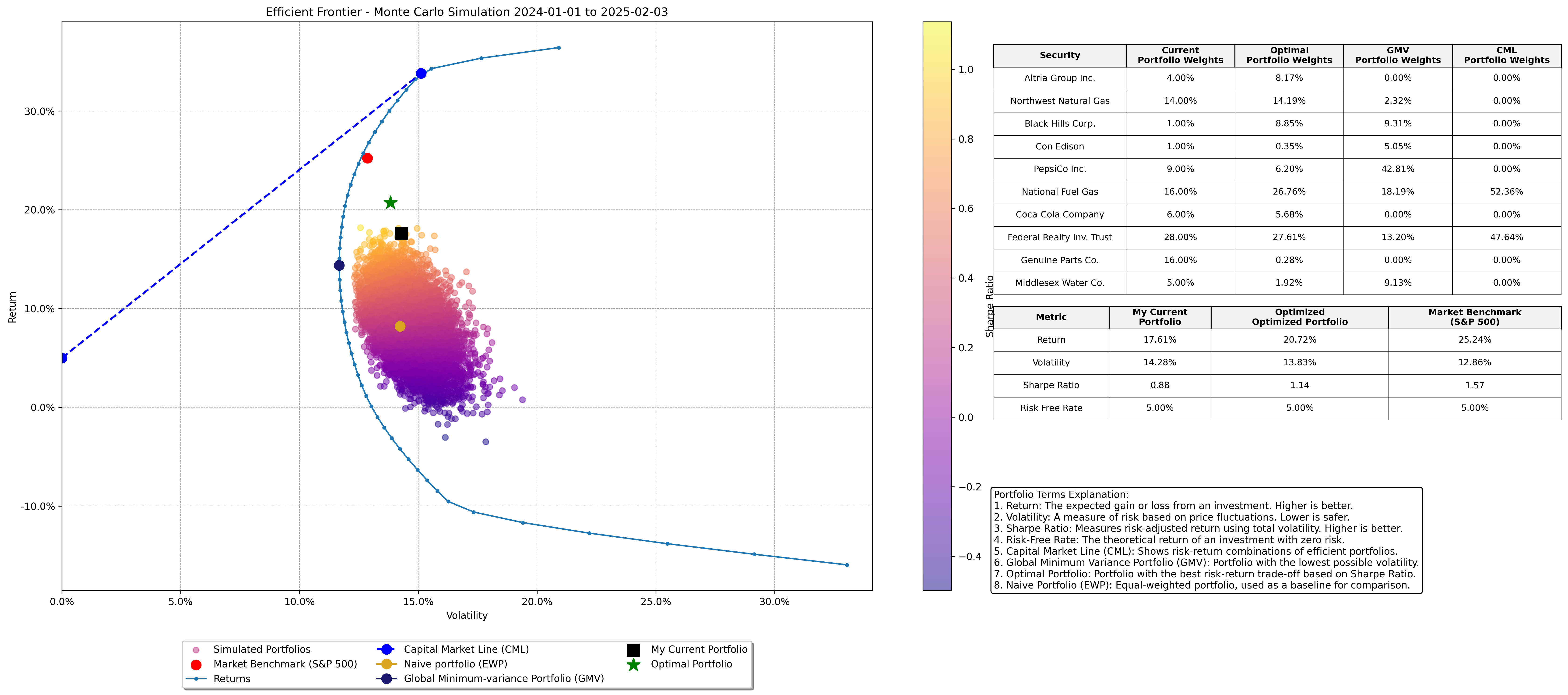

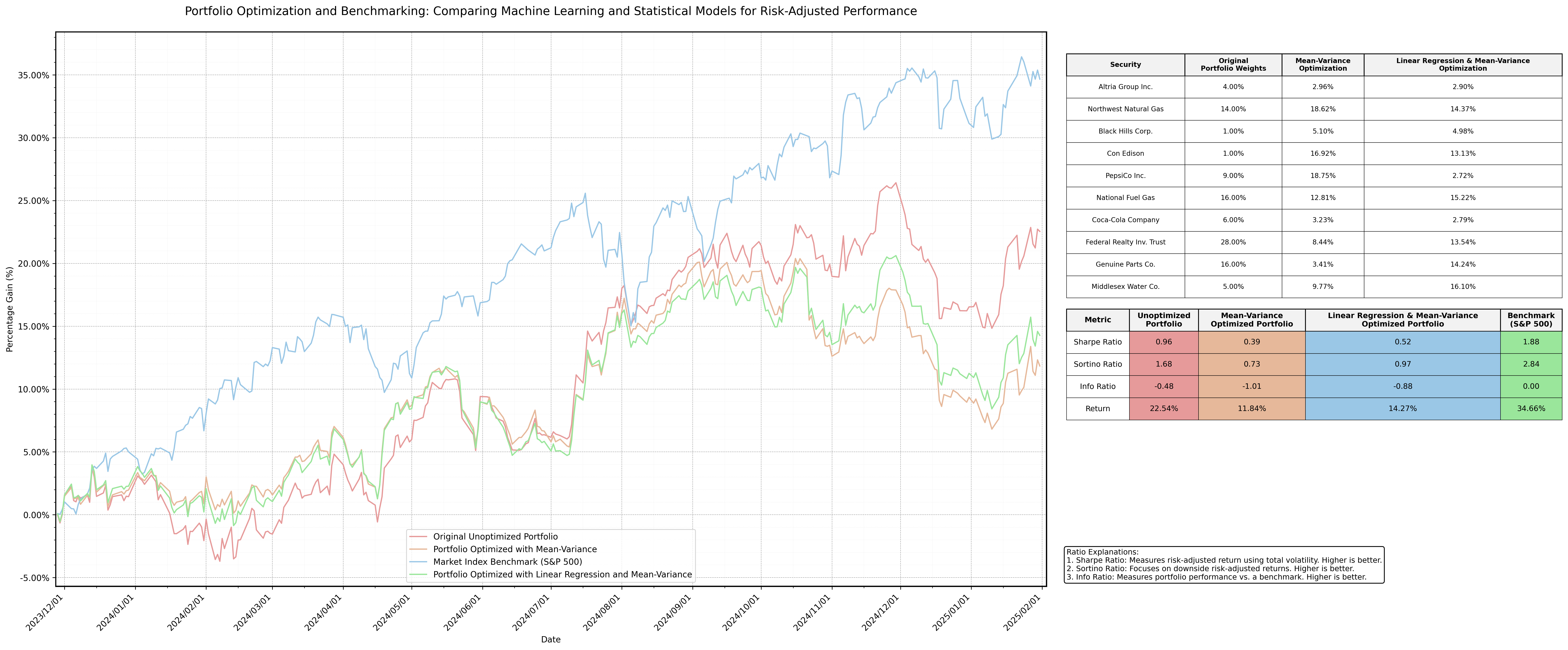

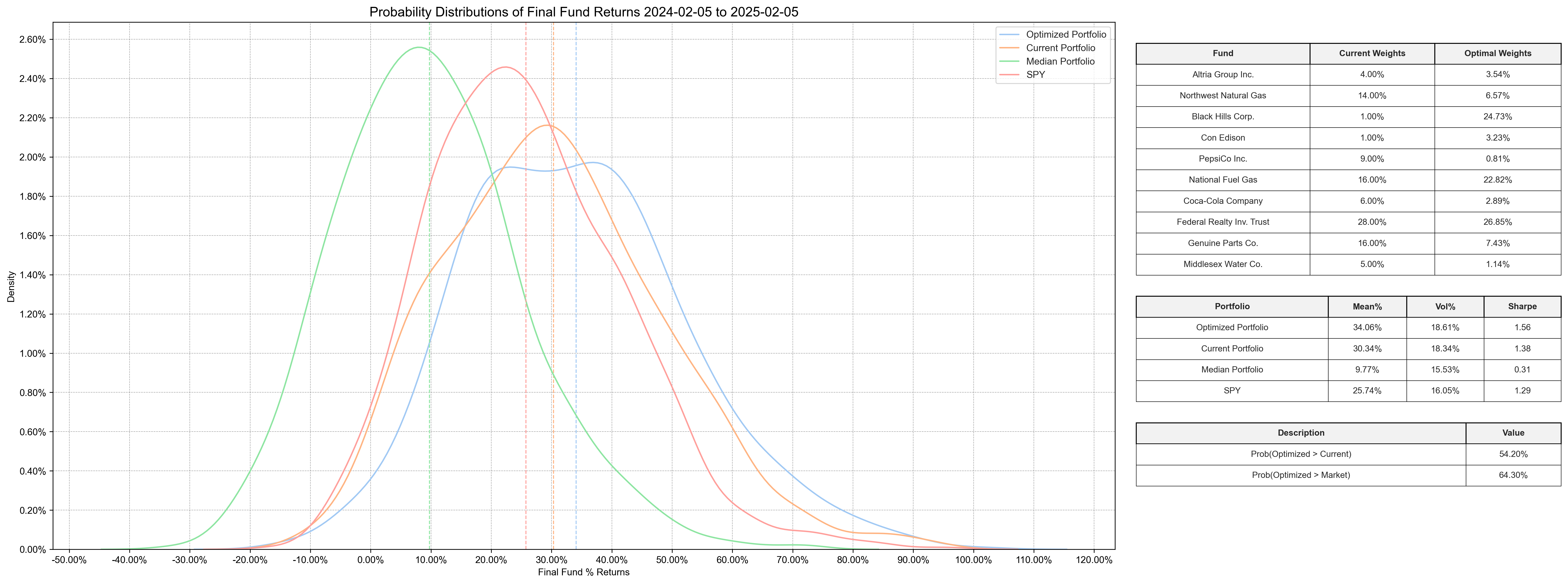

Create your portfolio table similar to the below:

| Asset | Weight | Label | MarketCap |

|---|---|---|---|

| MO | 0.04 | Altria Group Inc. | 110.0e9 |

| NWN | 0.14 | Northwest Natural Gas | 1.8e9 |

| BKH | 0.01 | Black Hills Corp. | 4.5e9 |

| ED | 0.01 | Con Edison | 30.0e9 |

| PEP | 0.09 | PepsiCo Inc. | 255.0e9 |

| NFG | 0.16 | National Fuel Gas | 5.6e9 |

| KO | 0.06 | Coca-Cola Company | 275.0e9 |

| FRT | 0.28 | Federal Realty Inv. Trust | 9.8e9 |

| GPC | 0.16 | Genuine Parts Co. | 25.3e9 |

| MSEX | 0.05 | Middlesex Water Co. | 2.4e9 |

import pandas as pd

from riskoptima import RiskOptima

import warnings

warnings.filterwarnings(

"ignore",

category=FutureWarning,

message=".*DataFrame.std with axis=None is deprecated.*"

)

# Define your current porfolio with your weights and company names

asset_data = [

{"Asset": "MO", "Weight": 0.04, "Label": "Altria Group Inc.", "MarketCap": 110.0e9},

{"Asset": "NWN", "Weight": 0.14, "Label": "Northwest Natural Gas", "MarketCap": 1.8e9},

{"Asset": "BKH", "Weight": 0.01, "Label": "Black Hills Corp.", "MarketCap": 4.5e9},

{"Asset": "ED", "Weight": 0.01, "Label": "Con Edison", "MarketCap": 30.0e9},

{"Asset": "PEP", "Weight": 0.09, "Label": "PepsiCo Inc.", "MarketCap": 255.0e9},

{"Asset": "NFG", "Weight": 0.16, "Label": "National Fuel Gas", "MarketCap": 5.6e9},

{"Asset": "KO", "Weight": 0.06, "Label": "Coca-Cola Company", "MarketCap": 275.0e9},

{"Asset": "FRT", "Weight": 0.28, "Label": "Federal Realty Inv. Trust", "MarketCap": 9.8e9},

{"Asset": "GPC", "Weight": 0.16, "Label": "Genuine Parts Co.", "MarketCap": 25.3e9},

{"Asset": "MSEX", "Weight": 0.05, "Label": "Middlesex Water Co.", "MarketCap": 2.4e9}

]

asset_table = pd.DataFrame(asset_data)

capital = 100_000

asset_table['Portfolio'] = asset_table['Weight'] * capital

ANALYSIS_START_DATE = RiskOptima.get_previous_year_date(RiskOptima.get_previous_working_day(), 1)

ANALYSIS_END_DATE = RiskOptima.get_previous_working_day()

BENCHMARK_INDEX = 'SPY'

RISK_FREE_RATE = 0.05

NUMBER_OF_WEIGHTS = 10_000

NUMBER_OF_MC_RUNS = 1_000

Example 1: Creating a Portfolio Area Chart

If you want to know visually how's your portfolio doing right now

RiskOptima.create_portfolio_area_chart(

asset_table,

end_date=ANALYSIS_END_DATE,

lookback_days=2,

title="Portfolio Area Chart"

)

Example 2: Efficient Frontier - Monte Carlo Portfolio Optimization

RiskOptima.plot_efficient_frontier_monte_carlo(

asset_table,

start_date=ANALYSIS_START_DATE,

end_date=ANALYSIS_END_DATE,

risk_free_rate=RISK_FREE_RATE,

num_portfolios=NUMBER_OF_WEIGHTS,

market_benchmark=BENCHMARK_INDEX,

set_ticks=False,

x_pos_table=1.15, # Position for the weight table on the plot

y_pos_table=0.52, # Position for the weight table on the plot

title=f'Efficient Frontier - Monte Carlo Simulation {ANALYSIS_START_DATE} to {ANALYSIS_END_DATE}'

)

Example 3: Portfolio Optimization using Mean Variance and Machine Learning

RiskOptima.run_portfolio_optimization_mv_ml(

asset_table=asset_table,

training_start_date='2022-01-01',

training_end_date='2023-11-27',

model_type='Linear Regression',

risk_free_rate=RISK_FREE_RATE,

num_portfolios=100000,

market_benchmark=[BENCHMARK_INDEX],

max_volatility=0.25,

min_weight=0.03,

max_weight=0.2

)

Example 4: Portfolio Optimization using Probability Analysis

RiskOptima.run_portfolio_probability_analysis(

asset_table=asset_table,

analysis_start_date=ANALYSIS_START_DATE,

analysis_end_date=ANALYSIS_END_DATE,

benchmark_index=BENCHMARK_INDEX,

risk_free_rate=RISK_FREE_RATE,

number_of_portfolio_weights=NUMBER_OF_WEIGHTS,

trading_days_per_year=RiskOptima.get_trading_days(),

number_of_monte_carlo_runs=NUMBER_OF_MC_RUNS

)

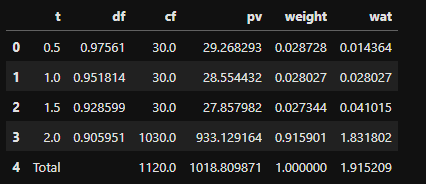

Example 5: Macaulay Duration

from riskoptima import RiskOptima

cf = RiskOptima.bond_cash_flows_v2(4, 1000, 0.06, 2) # 2 years, semi-annual, hence 4 periods

md_2 = RiskOptima.macaulay_duration_v3(cf, 0.05, 2)

md_2

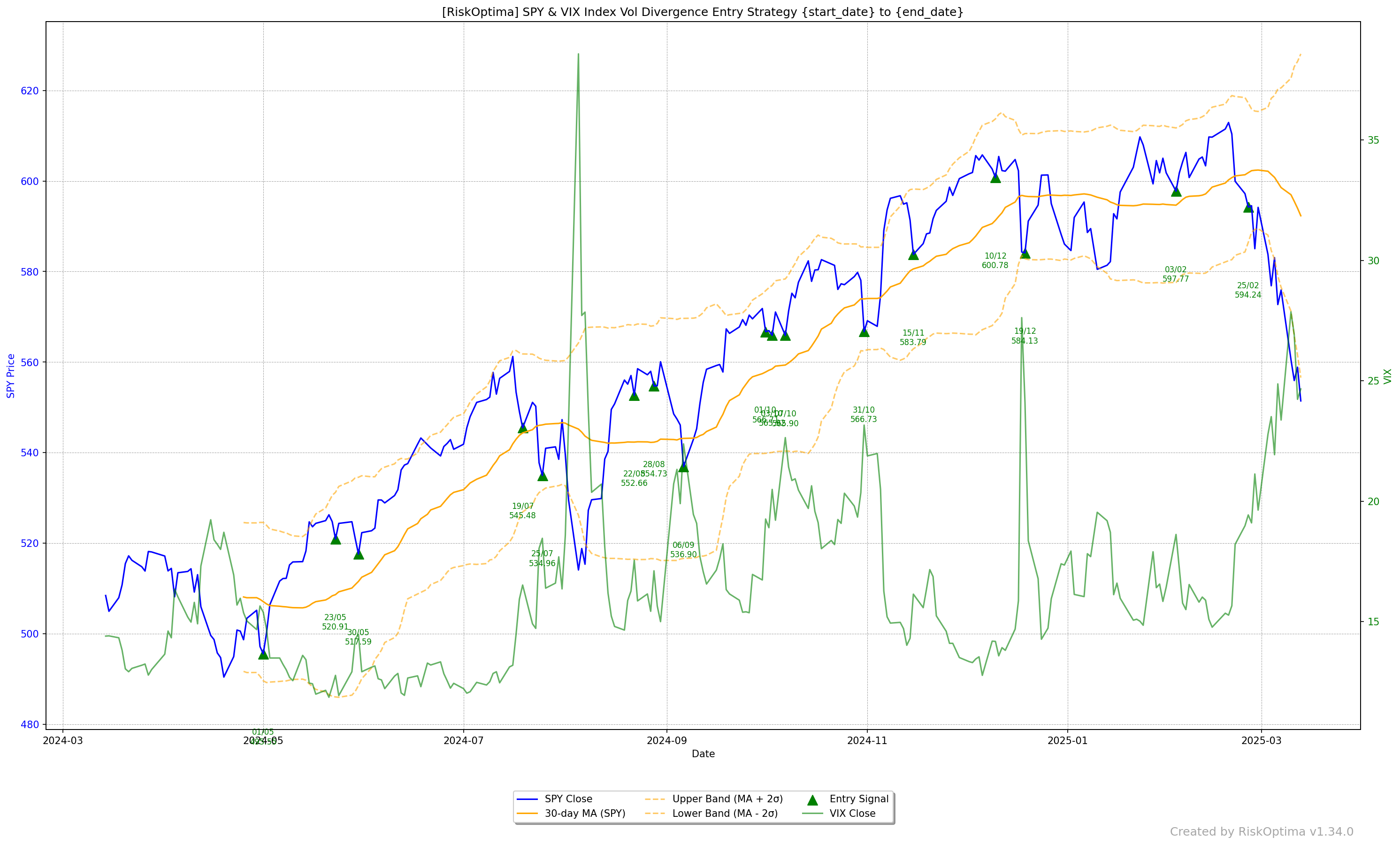

Example 6: Market Turns with SPY & VIX Divergence

ANALYSIS_START_DATE = RiskOptima.get_previous_year_date(RiskOptima.get_previous_working_day(), 1)

ANALYSIS_END_DATE = RiskOptima.get_previous_working_day()

df_signals, df_exits, returns = RiskOptima.run_index_vol_divergence_signals(start_date=ANALYSIS_START_DATE,

end_date=ANALYSIS_END_DATE)

Documentation

For complete documentation and usage examples, visit the GitHub repository:

Contributing

We welcome contributions! If you'd like to improve the package or report issues, please visit the GitHub repository.

License

RiskOptima is licensed under the MIT License.

Support me

Release history Release notifications | RSS feed

Download files

Download the file for your platform. If you're not sure which to choose, learn more about installing packages.

Source Distribution

Built Distribution

Filter files by name, interpreter, ABI, and platform.

If you're not sure about the file name format, learn more about wheel file names.

Copy a direct link to the current filters

File details

Details for the file riskoptima-2.3.1.tar.gz.

File metadata

- Download URL: riskoptima-2.3.1.tar.gz

- Upload date:

- Size: 60.0 kB

- Tags: Source

- Uploaded using Trusted Publishing? No

- Uploaded via: poetry/1.8.5 CPython/3.12.7 Windows/11

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

12a370ddb0df4c0b613ce7062b58630395d0b03f91c285971335959223075e6a

|

|

| MD5 |

7ccb81be5deeeaf97368958c2295de62

|

|

| BLAKE2b-256 |

e4115a24ba87a79939a8d8b9418554b268c3dae366e0147c0eab5c14ad81f5ff

|

File details

Details for the file riskoptima-2.3.1-py3-none-any.whl.

File metadata

- Download URL: riskoptima-2.3.1-py3-none-any.whl

- Upload date:

- Size: 65.1 kB

- Tags: Python 3

- Uploaded using Trusted Publishing? No

- Uploaded via: poetry/1.8.5 CPython/3.12.7 Windows/11

File hashes

| Algorithm | Hash digest | |

|---|---|---|

| SHA256 |

d499636aba0046861be947c58abd61ccdced8f5519adc5266427c1c1753b1235

|

|

| MD5 |

c8dfa9034f8744953d18e7b71e5ad66c

|

|

| BLAKE2b-256 |

292951dd351ddf631dc7062629566cded52b01d0062517ff5c6106e7634e15bb

|